BREAKING: Commure Hits $7B Backed by GC, Sequoia, Morgan Stanley

CEO Tanay Tandon | $70M Round, $750M Total Funding

Saving Doctors 75 Million Hours

Tanay Tandon, Co-Founder & CEO of Commure, joins Sourcery to break down the company’s new $70M round at a $7B post-money valuation, led by General Catalyst with participation from Sequoia Capital, Morgan Stanley, and Kirkland & Ellis.

→ Listen on X, Spotify, YouTube, Apple

With $750M raised to date, Commure now runs inside 500+ healthcare organizations, 3,000+ sites of care, and processes tens of billions of dollars in annual claims — with 85%+ of revenue cycle work completed without a human in the loop.

Tanay started the company at 18 out of his Stanford dorm room. Today, Commure has 1,200 employees across seven offices, supports 200M+ patient encounters a year, and has doubled ARR three years in a row.

We get into the round, the use of General Catalyst’s Customer Value Fund (CVF) for non-dilutive growth capital, why he believes point solutions will be wiped out, the Augmedix acquisition, the Summa Health partnership in Akron, the JPM flip-flops story, and his IPO plans.

Topics covered:

The $70M / $7B round and why they didn’t need the capital

CVF and non-dilutive financing for go-to-market

Building an AI-native OS for healthcare • HCA, Tenet, Epic, and Meditech partnerships

Why platforms beat point solutions

Lessons from acquiring Augmedix

What Alfred Lin, Hemant Taneja, and Teresa Carlson taught him

The path to IPO

𝐓𝐈𝐌𝐄𝐒𝐓𝐀𝐌𝐏𝐒

(00:00) Tanay Tandon, Co-Founder and CEO at Commure

(01:03) The $70M R&D Sprint

(03:45) Rockefeller's funding playbook beats dilutive VC

(05:42) Tokens killing SaaS margins

(07:14) Going public is the plan

(07:40) Automating healthcare’s back office

(11:02) Scaling Commure’s engine

(11:49) Partnering with Epic

(13:06) Why healthcare point solutions will be dead in 3 years?

(16:42) Learnings from the AWS-CIA deal

(19:13) Going to zero rollouts overnight

(22:23) Nuking malpractice premiums with AI

(23:52) Winning HCA’s trust

(26:27) Saving burned out doctors

(28:24) Buying a bankrupt hospital

(32:30) Ending healthcare interop

(35:41) The viral hiring email

(38:23) Acquiring for distribution

(45:13) Free blood samples?

(47:19) The Stanford hacker who became an enterprise sales rep

(48:21) The cargo shorts fiasco

(53:57) American healthcare isn't broken

(55:28) The agentic healthcare takeover

Brought to you by:

Brex—The intelligent finance platform: cards, expenses, travel, bill pay, banking—wrapped into a high-performance stack. Built for scale. Trusted by teams that move fast. visit → brex.com/sourcery

Turing—Turing partners with frontier AI labs to improve model capabilities in coding, reasoning, tool use, & multimodality, as well as with Fortune 500 enterprises to build & deploy end-to-end agentic AI systems in mission-critical workflows Visit: turing.com/sourcery

VCX—VCX is the public ticker for private tech, allowing investors of all sizes to invest in venture capital. View The Portfolio at GetVCX.com

Deel—Deel is the global people platform that helps startups hire, manage, pay, and equip anyone, anywhere. Trusted by more than 35,000 fast-growing companies, Deel is the people platform that just works, so teams can scale without the chaos. Visit: deel.com/sourcery

Public-–Investing platform Public just launched Generated Assets, which lets you turn any idea into an investable index with AI. With Generated Assets, you can build, backtest, refine, and invest in any thesis with AI. Gone are the days of one-size-fits-all ETFs. Try it today: public.com/sourcery

Merge—The leading provider of customer-facing integrations and agentic tools for frontier LLMs, Fortune 500 organizations, and B2B SaaS companies. Visit: https://merge.dev

Commure’s $7B Bet on AI Healthcare

Commure CEO and Co-Founder Tanay Tandon joined Sourcery to discuss the round, the company’s trajectory, and his vision for rebuilding American healthcare on top of LLMs and agents. Below, a seven part breakdown of the conversation.

→ Listen on X, Spotify, YouTube, Apple

The Funding: A $7B Valuation Without the Cash Pressure

Commure’s latest round is notable less for the dollar amount than for the posture behind it. Tandon was direct about why the company raised:

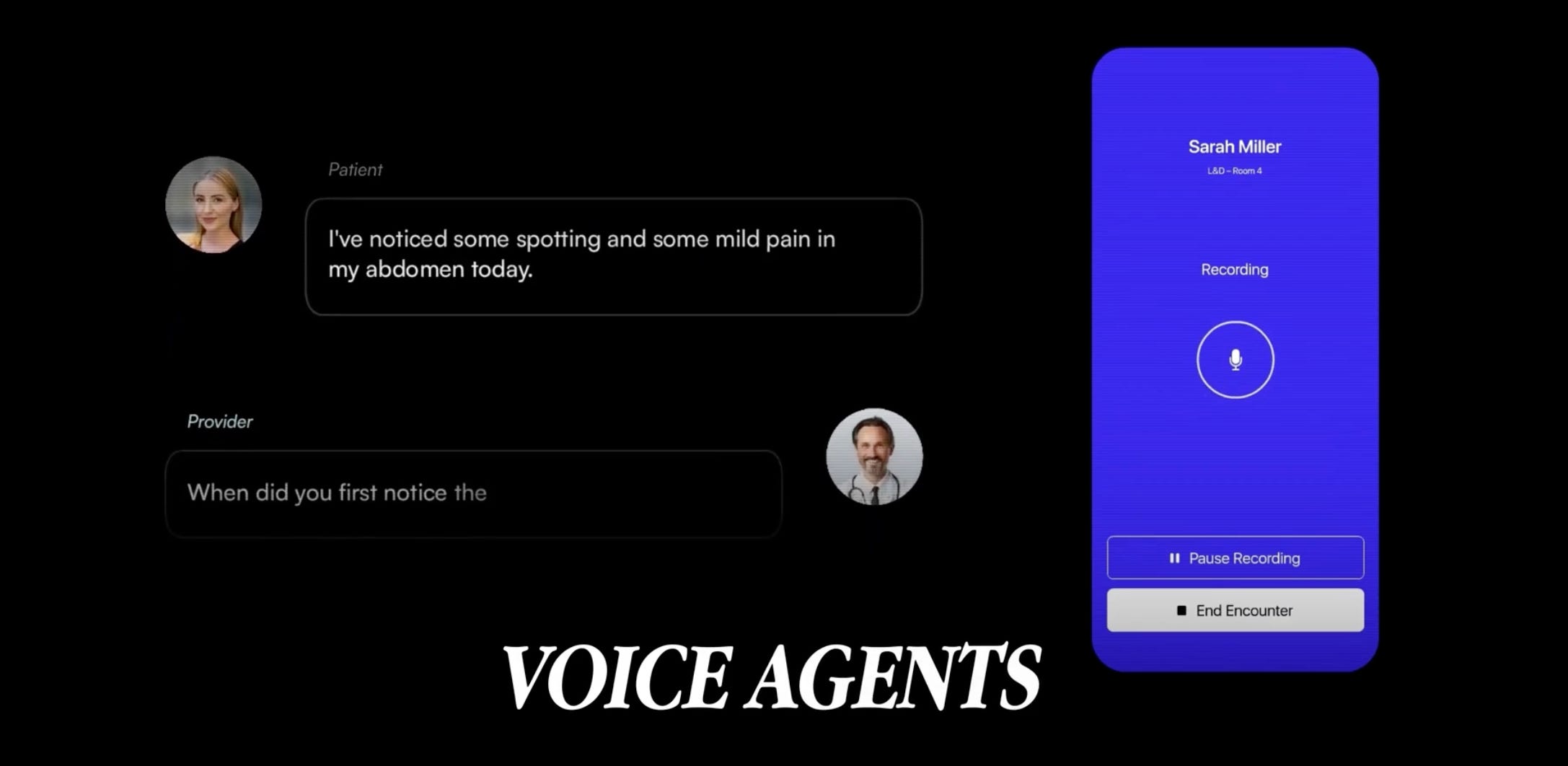

“This round.. we really didn’t need the capital. We raised it for pricing purposes, and we saw a couple interesting opportunities to accelerate R&D, particularly around AIR, which is our LLM native EMR platform… and our voice agent platform.”

The company has now raised roughly $750 million in total across its life, and the new round was structured to set a new mark without meaningfully diluting shareholders.

A central part of that strategy is General Catalyst’s Customer Value Fund (CVF), a non-dilutive credit facility underwritten against forward-looking SaaS cohorts rather than the company’s balance sheet.

Tandon framed it as a return to first principles: “Credit is not a unique concept… The reason startups shy away from it is it often puts this massive liability on your balance sheet, and if the worst case Armageddon happens, your whole company could implode.” CVF, he argued, sidesteps that risk by tying repayment to customer performance. His operating philosophy follows from there: “You actually don’t wanna use balance sheet for go-to-market. You wanna use balance sheet for R&D & these more durable long-term investments.”

Careful about the financing of the business & its structure, Tandon was straightforward abou his long-term financing goals: IPO.

“I think the best American businesses go public and become long, durable parts of retail and allow the public to invest in them,” he said, adding that given the company’s scale, with hundreds of millions in revenue, an IPO would “be fueled by going public as opposed to being hampered by it.”

The Product: An AI Operating System for Healthcare

Commure’s pitch is that healthcare doesn’t need another point solution. It needs an operating system.

“For Commure at its core is a software company that builds tools for providers & for healthcare administrators. This is a multi-trillion dollar problem, and even when you cohort it down, there’s a trillion dollars spent on healthcare admin every year.”

The platform spans clinical and financial workflows: ambient documentation, autonomous coding, patient intake and engagement, revenue cycle management, and back office automation, all orchestrated through what he calls Commure OS.

“We’ve built a series of fine-tuned language models & agents that automate all of those tasks and truly take a health system that might operate at 2-3% operating margin today because of all the labor it needs, and turn it into something that can operate at 20-30% operating margin, the top percentile healthcare practices & systems.”

He’s betting that consolidation is inevitable: “that’s not going to be a hundred different point solutions. That’s actually, actually gonna be one revenue engine and a series of agents that are orchestrated on a single platform.”

That conviction extends to how he sees competitors. Tandon drew a historical parallel to Grammatik, the early grammar checker eventually wiped out when Microsoft Word shipped autocorrect natively.

“There’s a lot of nonsense GPT wrapper businesses out there right now… they grew fast. They got a lot of VC interest. But they’re gonna be gone in three years, because companies like ourselves will completely disintermediate them.”

Scale Measured in Hours, Encounters, & Margins

The metrics Commure now operates at make the platform thesis concrete. The company supports 500+ healthcare organizations across thousands of sites of care, integrates with dozens of EHRs, and processes tens of billions of dollars in annual claims, with the vast majority of revenue cycle work completed without a human in the loop. Over 50 of the largest health systems in the country, including HCA and Tenet, are customers. ARR has doubled three years in a row.

Tandon translated the scale into human terms: “We support, I wanna say, 200 million patient encounters every year now.” On ambient documentation alone, the product that listens to a clinical encounter and generates the note and superbill, he said the company runs “about 50 million annualized appointments every year, saving at least 75 million hours a year for physicians… and that’s just productivity straight back into the American economy.”

The most affecting story he told was a quote from a physician using the product, surfaced publicly by General Catalyst’s Hemant Taneja: “I was about to quit. I was looking for another job because these long shifts were just ridiculous… And then I used the tool, the Premier Ambient tool paired with Revenue Cycle, and it literally finished fourteen charts instantly.” Tandon’s framing: “We have a massive labor shortage in healthcare. We cannot have trained people leave the system.”

Tokens, Margins, & Why SaaS Math Is Breaking

One of the more candid threads of the conversation was on unit economics in the LLM era, specifically how token costs are reshaping software margins.

“VCs have a good sense of what a SaaS business looks and feels like in terms of its margin structure, its payback, its CAC, its LTV,” Tandon said. “And one of the challenges is that these token businesses have essentially turned a lot of software businesses to service level margin. And if you play the game the same way you did two years ago, you can blow up, and you can burn a lot of cash in the process.”

Commure’s response has been to operate the business as a portfolio of distinct margin profiles. “We have, you know, we have parts of our business that run at pure SaaS margins in the high 80-90s. And you have other parts of the business, like full-cycle RCM, that have a labor component and a heavy token component, and those run at everywhere… anywhere from the high 60s in their implementation stage to the mid 70s in their steady state.”

That mixed structure is precisely what makes non-dilutive financing rational. If payback periods are well understood, Tandon argued, equity is the wrong instrument: “If you fundamentally understand the payback periods, then you should use CVF. You should use non-dilutive mechanisms to fund that expansion.”

AI in Practice: Accuracy, Evals, & the Cost of Hallucination

In healthcare, AI failure modes are not abstract. They’re regulatory, reputational, and clinical. Tandon was explicit about where the bar sits:

“Where you see rollouts get completely stopped or companies go to zero overnight is in cases where a model or a tool hallucinates or performs incorrectly and ends up impacting patient care, and so it ends up being maybe the most important thing.”

His operating answer is infrastructure heavy.

“The only way to truly ensure that is great evals. You need to have a massive data set of historical documentation or whatever the task might be, coding, voice calls, to then measure your model iterations on. Because, you know, when you release a new version of a model or a new version of an agent, it does some things amazing, but then it does a couple of things that are kinda weird, and there might be regression and performance deterioration on the fringes.”

He sees this as a structural advantage for larger, well-capitalized teams: smaller competitors can ship quickly but lack the engineering depth to catch silent regressions.

How do they get these AI systems into an industry with limited AI knowledge? An implementation playbook borrowed openly from Palantir.

“We have this forward deployed team of engineers that, you know, obviously stolen from Palantir, but I mean, the model works so well.

You take smart, hungry people that are early in their careers, and you throw them into the face of the problem within the hospital.”

Example: Commure’s first HCA deployment, he said, was “literally a couple engineers on the ground in a hospital with three physicians, and it was like two months of back and forth, how do we make this model work really well in a hospital setting or an ED setting, which are really hard settings to perfect documentation in.”

Healthcare Dynamics: Politicians, Operators, & the Regulatory Window

Asked about the state of American healthcare, Tandon gave one of his sharpest takes: “I would actually say that healthcare’s biggest problem today is it is run by politicians. It is not run by ruthless, pragmatic business operators.” The for-profit systems that are compounding fastest, he argued, share a common trait, aggressive CEOs at the top, while academic & nonprofit systems remain stuck in “design by committee & decide by committee.”

He was unusually positive on the current administration’s posture toward healthcare innovation, particularly on interoperability. “One of the biggest problems in healthcare over the last thirty years was an EMR could guzzle up all your data and then sit there, and then when you ask for it back, quote you some crazy fee to move one piece of data from one system to another.” He praised the administration for “funding the Department of Justice to come after folks that are engaging in information blocking or violating the Cures Act.”

His hottest take pushed back on the conventional narrative that American healthcare is broken. “The American healthcare system is the engine of innovation for the whole, whole world. The vaccines that are made are the best in the world. The drugs that are made are the best in the world.” The opportunity, in his framing, isn’t to import another country’s system. It’s to remove the work tax with software:

“LLMs are this gift that we’ve received to go nuke all of that work tax, and that in some ways is gonna be my life’s work, eliminating the work tax and making the system a trillion dollars more efficient.”

Hiring “Heat-Seeking Missiles”

With over a thousand employees across offices in Mountain View, New York, Boston, Nashville, Salt Lake City, and Bangladesh, hiring has become one of Tandon’s primary jobs. His framework went viral after Sequoia’s Alfred Lin tweeted an internal memo: Commure looks for “heat-seeking missile[s] for pain,” people who, in Tandon’s words,

“actively seek out the hairiest, gnarliest problems that customers have or exists generally in the business… and then surgically works to eliminate said problem. They have almost an addiction to seeking out sources of pain and blowing them up.”

The philosophy is rooted in a specific worldview about value creation. “Pain is the genesis of all capitalism. Like, there is problem, and then someone comes up with solution, and then there’s value creation and value capture in that process. Without pain, there is no capitalism. And as a result, I think we should all pray at the altar of pain.”

Without that disposition, he argued, fast-growth companies don’t survive: “Your go to market will never be as fast as the next guy over. Your products will never evolve as quickly because every product has pain.”

M&A Strategy

The same lens shapes Commure’s M&A strategy, which has included the Athelas merger and the acquisition of Augmedix, a public company purchased primarily for distribution.

Biggest M&A Lessons:

Pristine assets rarely offer price advantages, so good acquirers buy companies with fixable flaws

Culture is non-negotiable.

“There’s always a winning acquiring culture that becomes the culture of the combined business. And there are people in the company you’re acquiring that heavily opt into that. There’s also people that opt out, and that’s totally fine.”

The window for that reset, in his experience, is short, roughly the first month and a half post close.

The material presented on Molly O’Shea’s website are my opinions only and are provided for informational purposes and should not be construed as investment advice. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular security, strategy, or investment product. Any analysis or discussion of investments, sectors or the market generally are based on current information, including from public sources, that I consider reliable, but I do not represent that any research or the information provided is accurate or complete, and it should not be relied on as such. My views and opinions expressed in any website content are current at the time of publication and are subject to change. Past performance is not indicative of future results.

Paid Endorsement. Brokerage services by Open to the Public Investing Inc, member FINRA & SIPC. Advisory services by Public Advisors LLC, SEC-registered adviser. Crypto trading provided by Zero Hash LLC, licensed by the NYSDFS. Generated Assets is an interactive analysis tool by Public Advisors. Output is for informational purposes only and is not an investment recommendation or advice. See disclosures at public.com/disclosures/ga. Matched funds must remain in your account for at least 5 years. Match rate and other terms are subject to change at any time.

Very good.

running the business as a portfolio of distinct margin profiles (some SaaS-pure, some labor-heavy RCM) is going to be the playbook for vertical AI founders. great interview molly 🎙️