BREAKING: General Catalyst's First-Ever Quarterly Review

CEO Hemant Taneja

Is GC Going Public??

Hemant Taneja, CEO of General Catalyst, joins Sourcery to unpack GC’s first-ever quarterly review.

→ Listen on X, Spotify, YouTube, Apple

We cover why he wrote it, the state of GC’s $43B ecosystem, why the software buyout model is broken, Anthropic’s Series G at $380B, the $5B India commitment, buying Summa Health in Akron, the Anthropic–DoW controversy, Mythos & Project Glasswing, Nikesh Arora joining the GC board, and his take on “Tech Lash 2.0.”

Plus: Is GC going public??

HUGE thank you to Deel Co-Founder & CRO Shuo Wang for the introduction to Reggie & the GC team, I am SO happy we were able to make this happen so quickly! What a treat.

Read the Q1 2026 Review (overview below)

𝐓𝐈𝐌𝐄𝐒𝐓𝐀𝐌𝐏𝐒

(00:00) Hemant Taneja, CEO at General Catalyst

(01:21) Present state of General Catalyst

(05:08) Seed, Creation & the Customer Value Fund

(06:54) The purpose behind GC’s quarterly review

(12:26) The biggest AI themes right now

(15:06) How AI is changing investing decisions

(19:25) Why seed and Series G require the same conviction

(22:55) Why does he holds two titles at once?

(25:17) Why Silicon Valley glorifies the wrong founders

(27:52) Building an AI-native hospital

(30:20) Managing funds through bubbles and hype cycles

(33:13) How funds sell ownership stakes

(34:59) Why the software buyout model is broken

(38:44) Vista's new software buyout debt fund

(39:20) Global Resilience vs. American Dynamism

(41:49) GC’s $5B bet on India

(45:48) What global investing teaches you

(47:09) The four forces of tech lash

(50:12) Anthropic and the Pentagon

(54:06) Is GC going public?

(55:26) The Puka shell necklace era

Brought to you by:

Brex—The intelligent finance platform: cards, expenses, travel, bill pay, banking—wrapped into a high-performance stack. Built for scale. Trusted by teams that move fast. visit → brex.com/sourcery

Turing—Turing accelerates superintelligence by helping frontier AI labs improve model capabilities and enabling enterprises to deploy end-to-end AI systems inside mission-critical workflows. Visit: turing.com/sourcery

VCX—VCX is the public ticker for private tech, allowing investors of all sizes to invest in venture capital. View The Portfolio at GetVCX.com

Deel—Deel is the global people platform that helps startups hire, manage, pay, and equip anyone, anywhere. Trusted by more than 35,000 fast-growing companies, Deel is the people platform that just works, so teams can scale without the chaos. Visit: deel.com/sourcery

Public-–Investing platform Public just launched Generated Assets, which lets you turn any idea into an investable index with AI. With Generated Assets, you can build, backtest, refine, and invest in any thesis with AI. Gone are the days of one-size-fits-all ETFs. Try it today: public.com/sourcery

Merge—The leading provider of customer-facing integrations and agentic tools for frontier LLMs, Fortune 500 organizations, and B2B SaaS companies. Visit: https://merge.dev

GC’s First-Ever Quarterly Review

CEO Hemant Taneja on AI’s Dominance, Broken Buyouts, & the Gray Areas of Silicon Valley

I just sat down with Hemant Taneja, CEO of General Catalyst, at the top of GC’s San Francisco tower to walk through the firm’s first-ever quarterly review.

It’s a deliberate break from the X-thread, fireside-soundbite, click-bait rhythm that dominates venture commentary, a slower, more honest attempt to make sense of a quarter where, as Hemant puts it, “a lot of large things happened simultaneously, none of them finished.”

Below, I’ve pulled out the most data-oriented sections of the review and our conversation, the software buyout math, the Anthropic trajectory, the India commitment, the CVF credit rating milestone, and tied them back to the broader argument Hemant is making about where durable value lives in the AI era.

→ Listen on X, Spotify, YouTube, Apple

Why the First Quarterly Review, & Why Now?

Hemant’s explanation for the review’s existence is itself a thesis about the industry. The formats venture has defaulted to, X, LinkedIn, conference stages, reward certainty & controversy. None of them, in his view, help anyone actually make sense of the world.

When I asked him why he started writing it now, he told me, “A lot of that generally skews us towards taking very polarized views, because the stuff that amplifies in the world tends to be very black or white, & the progress gets made in the gray.”

The review itself opens on the same note, the volume of happenings, the heat of the discourse, and the open question mark of what the very near future will look like can leave one feeling confused. Hemant’s answer is to slow down, once a quarter, take stock, and be willing to sit with complexity rather than reach for a clean narrative.

The format also forces GC to be honest about the arc it's actually on. In our conversation, Hemant described three core investment strategies:

Seed (the firm's venture capital fund, which he calls the largest seed fund of its kind)

Creation (the build-and-transform strategy run by Marc Bhargava that includes AI-native rollups like Long Lake, Crescendo, Udia, and company hatches like Hippocratic AI)

Customer Value Fund (the investment-grade-rated product for scaling proven businesses)

But those three sit inside a larger ecosystem. Percepta is GC's in-house AI engineering and research company, bringing applied AI into GC's portfolio and partner institutions. HATCo is the healthcare transformation arm behind the acquisition of Summa Health in Akron, Ohio, where the firm is trying to build the first AI-native community hospital. GC Institute is the policy arm operating out of DC, Brussels, and Delhi. And GC Wealth, launched publicly in early 2025 under former First Republic executive Dave Breslin, is the firm's full-service wealth management business for founders and entrepreneurs in GC's Famiglia.

The Anthropic Trajectory & What “Beneficent Singularity” Actually Means

The review leads with AI because, as Hemant writes, “I can’t start anywhere else.” The central data point: Anthropic went from $1B to over $20B (now allegedly at $30B ARR) in annualized revenue run rate in fifteen months. GC first invested in March 2025 at a $61.5B valuation. The March 2026 Series G valued the company at $380B, one of the largest venture rounds in history.

Hemant frames this through the Collisons’ 2026 Stripe letter, which reported over 700 AI agent companies launching on the platform in a single year. Their conclusion: the world may be at the advent of a different and “hopefully much more beneficent singularity.” Hemant lingers on those word choices, hopefully, beneficent, because they frame the singularity as an aspiration, not a foregone conclusion.

His point is that capability is no longer the binding constraint. Trust is. The companies that will matter in thirty years, he argues in the review, are not necessarily the most technically capable ones. The actual transformation happens inside regulated, high-stakes environments, healthcare, education, defense, financial systems.. he makes it clear, those environments don’t reward or value raw capability. They reward embedded trust.

That reframing is what drives GC’s full-arc positioning: 20 seed investments this quarter alongside the Anthropic Series G, Percepta building AI engineering capacity in-house, and Creation doing AI-native rollups of incumbent businesses.

Why the Software Buyout Model Is Broken

The most data-dense section of the review is Hemant’s breakdown of software buyout economics, and it’s worth walking through carefully. The setup: a high-quality B2B software business bought a few years ago with sticky enterprise contracts, 90% gross margins, and 25% annual growth. Entry price: 25× EBITDA (roughly 40–50× FCF), partially financed through private credit, underwritten to a five-year hold. Over that hold, EBITDA grows 50%. The debt comes down. By every operational measure, the deal worked.

And yet the equity doesn’t. EBITDA growth added $625M in enterprise value. Multiple compression from 25× to 12× destroyed $975M. The deal returned 0.68× MOIC, roughly a third of LP capital lost on a deal where the underlying business succeeded. Annualized over 5 years, that’s a deeply negative IRR of approximately -7%.

When I asked Hemant to walk me through this live, he put it simply: the assumption of terminal value is gone.

“In the world of AI today where code is self-writing, to say that a piece of software in a company that has been existing, let’s say five years, the free cash flow, that is worth 30 times, means you’re gonna have 30 years of generating that free cash flow is what you’re paying for. How can you ever make that assumption when technology is changing so fast to say these things are that durable?”

His path forward: structure software buyouts the way mature-category buyouts have always been structured, on cash flows, not exit multiples.

In the review, he runs the counterfactual. Same $50M EBITDA business, 25% growth, but entered at 10× instead of 25×. $500M enterprise value, 3× EBITDA leverage, $350M equity check. Over five years, EBITDA grows to $75M through genuine AI-driven operational improvement. Exit clears at 14×. Enterprise value: $1.05B. Equity recovered: $950M. That’s a 2.7× MOIC and an IRR of approximately 22%.

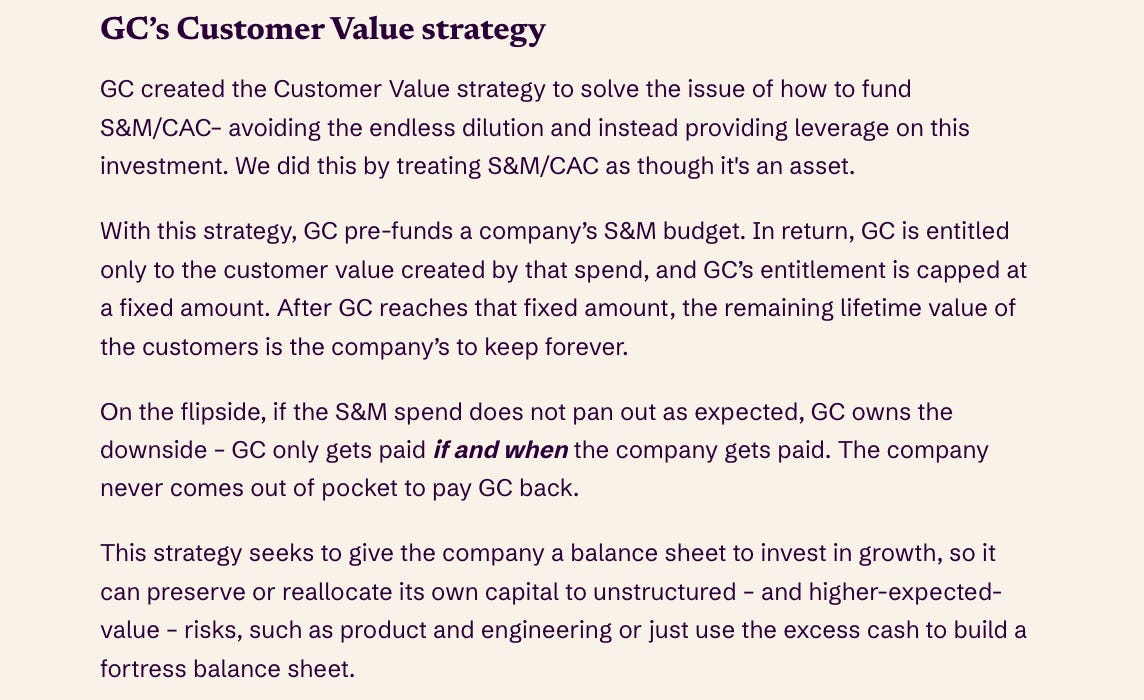

The CVF Credit Rating & What It Unlocks

The other major financial milestone Hemant discloses in the review is that GC’s Customer Value Fund reached an investment-grade credit rating this quarter, BBB or higher on roughly two-thirds of the capital. To the best of GC’s knowledge, no venture product has ever reached that threshold before.

The unlock is scale. Apollo Global Management runs close to a trillion dollars in AUM, roughly 80% of it in investment-grade credit strategies. That’s nearly $800 billion in capital at a single asset manager that venture has historically been unable to access, because venture investments carry no defined duration or structure. CVF, which launched in 2021, can now bring that kind of capital to bear for GC’s companies, and it did so in under five years.

Fast-growing companies like Fivetran, Kandji, Ro, Travelperk, Superplay, & Upside are already using CVF to fund customer acquisition costs, with CFOs describing it as a dedicated growth balance sheet that scales with unit economics rather than market conditions.

In our conversation, Hemant tied this back to the software buyout argument. CVF gives GC the ability to drive returns in software on a cash flow basis, without the terminal-value dependency that’s impaired so much of the current vintage. Paired with Creation (for transforming established assets) and Percepta (for the AI orchestration layer), it’s the financial infrastructure behind GC’s thesis that the next era of private markets returns comes from AI-driven top-line growth, not cost-cut exits.

GC’s direct exposure to pure SaaS, for context, is approximately $4 billion out of $43 billion in AUM, much of which sits across strong pre-2022 companies in fintech, healthcare, and defense that have embraced AI and are scaling faster than ever.

The $5B India Commitment & Global Resilience

In February, Hemant flew to New Delhi for the India AI Impact Summit and announced a $5B GC commitment to India over the next five years, one of the largest single-country investment commitments in venture history. When I asked him why India, he broke it into three forces playing out at once.

The first is systems. India has a pattern of solving for constraint: generic pharmaceuticals, UPI (which now processes more transactions than Visa and Mastercard combined), and Aadhaar (the largest biometric database on earth).

The second is scale, India will be the third-largest economy within the decade, with one million young people entering the workforce every month.

The third is resilience: India is actively diversifying away from Russian defense procurement, with 75% of modernization spend now going domestic (up from roughly 60% five years ago) and defense exports up 34x over 11 years.

The India commitment sits inside a broader global resilience thesis. Hemant told me in the interview that the geopolitics will force supply chains to shift, Europe won’t buy American defense products at scale, India won’t rely on Russia and America, so defense primes will emerge everywhere.

GC is already invested in Anduril & Saronic in the U.S., Helsing in Europe (Jeannette zu Fürstenberg, Daniel Ek, & Paul Kwan), and Raphe in India.

In Hemant’s framing, this isn’t just TAM expansion. It’s a values statement about inclusive prosperity: if AI concentrates opportunity in a handful of companies in a handful of countries, society will reject it, and the whole transformation stalls.

Anthropic–DoW Controversy & Mythos

The part of the review I most wanted to push him on was the Anthropic–Department of War situation from February. The public discourse simplified fast into “morally superior AI vs. unbridled acceleration.” Hemant’s position is that neither side captures what actually happened.

“I cannot say the perspectives on either side were wrong,” he told me. “It’s just like from where you sit and how you think about the world and what’s important is really what led to those issues. But what it shows you is just the complexity of what we have to go through.”

His concern in the review is less about the specifics of that deal and more about what it revealed.. how quickly the public reached for the exit in the face of genuine complexity. The same questions, where should AI have no role, who decides, will show up in healthcare, education, workforce, and online safety, and the industry needs governance architecture, not leadership preference.

Mythos is the other side of that coin. Anthropic could have released it broadly; instead they rolled it out through Project Glasswing to a tight group focused on eliminating vulnerability debt in critical infrastructure. Hemant calls the restraint admirable, “the opposite of move fast and break things,” and adds news that Nikesh Arora, who’s joining GC’s board, is part of the “Glasswing 40.” His broader point is that the individual moral frameworks from leaders like Dario aren’t a governance system. The industry needs the architecture to make responsible deployment practice rather than preference.

The thread running through all of this, Anthropic, Mythos, Iran, the DoW, is Hemant’s argument that the world is irreducibly gray, and the leaders worth following are the ones who can stay in the gray long enough to design something durable.

Nikesh Arora Joins the GC Board

One of the more consequential governance moves Hemant discloses in the review is that Nikesh Arora, CEO of Palo Alto Networks and one of the “Glasswing 40” working with Anthropic on Mythos, is joining GC’s Board. In the review, Hemant writes:

“I’m very glad that Nikesh Arora, who is joining GC’s Board, is part of the ‘Glasswing 40’. Nikesh has led some of the most consequential technology organizations in the world, and I’ve long admired the clarity and ambition he brings to everything he does. His presence reflects the caliber of judgment being brought to bear on a model that could either do serious damage to or rigorously armor the world’s critical systems.”

Ken Chenault remains Chairman, and Nikesh is joining as lead independent director. When I asked Hemant about the appointment in our interview, he laid out the reasoning:

“He’s been, first of all, incredibly brilliant. He’s an entrepreneurial soul running a Fortune 500 company, & he’s done an incredible job building that. He’s also a great investor mind. So as I think about our GC ecosystem, which is a collection of investors & builders, I just think he’d be a great mentor for all of us.”

The framing mattered. Hemant isn’t treating this as a prestige appointment. He’s treating it as another node in the leadership structure he’s built around himself, Ken Chenault as Chairman, former industry CEOs like Ken Frazier, Kate Walsh, Steve Klasko, and Daryl Tol helping run the company, and now Nikesh as a sounding board on where AI and enterprise security are actually headed.

“I’ve had many conversations with him about where this is going, and every one of those conversations is extremely provocative,” Hemant told me, “and so it made sense to lean on him. Just like we lean on Ken.”

Tech Lash 2.0 & The 4 Forces Driving It

The review’s most pointed section is Hemant’s argument that “Tech Lash 2.0” is already building around AI, and that it’s largely self-inflicted. He cites a Wall Street Journal piece calling this “The Most Joyless Tech Revolution Ever” and agrees with the framing. The anxiety spreading across society about displacement, erosion of human connection, and what intelligent machines mean for ordinary lives is, in his view, fully rational, and largely a response to who Silicon Valley has become in public. He identifies four forces that have brought us here.

The first is the social-media optimization of our minds. Hemant argues the industry has given itself false permission to decouple its social presence from its real-life presence. “Moderation does not get engagement,” he writes. “Nuance does not go viral. And so we have collectively abandoned both.” When I asked him about it directly, he was blunt: saying ridiculous things for attention is “a entirely unproductive exercise if you’re focused on the long term. It is a very short term mindset.”

The second is politics contamination. When Silicon Valley entered the political arena in recent years, Hemant argues it had the opportunity to export its best qualities, bias for action, intellectual honesty, genuine meritocracy. Instead, it imported the worst qualities of politics: tribal sorting, ideological litmus tests, zero-sum conflict performed for audiences rather than resolved for outcomes. GC’s response was to decline political engagement and instead launch the GC Institute, investing in policy education across DC, Brussels, and Delhi. “We had the institutional credibility to elevate public discourse,” Hemant writes. “We degraded it, and our own industry, instead.”

The third is the genius asshole myth. Hemant’s argument here is empirical: organizational behavior research consistently shows that one genuinely toxic person costs an organization hundreds of thousands annually in lost productivity, turnover, and diminished performance. When someone succeeds and happens to be cruel, we assume causation when the evidence shows coincidence. “They succeed despite it,” he writes. “They would succeed more without it.” The theory that brilliance licenses cruelty, in his view, is both statistically wrong and a license most people invoking it don’t qualify for.

The fourth, and the one Hemant has made personal mission to counteract, is contempt for legacy. In Silicon Valley’s culture, “legacy” has become a synonym for irrelevance. He considers this precisely backward. “Legacy is a beautiful word and a beautiful thing to have built. The word itself tells you what matters: you endured. You were trusted long enough, by enough people, to leave a mark.” The industries tech most wants to transform are governed and trusted by people with decades of institutional knowledge the industry doesn’t have. Treating them as obstacles rather than partners is, in his view, how the transformation stalls.

The Case for Kindness (Not Niceness)

When I asked Hemant about the kindness argument in our interview, he was careful to draw a distinction that matters. Kind is not the same as nice. “Kindness and ambition are not at odds with each other,” he told me. “I think in Silicon Valley, we try to glorify the asshole symptom of founders thinking that’s almost a necessary ingredient to succeed. And I don’t think it has to be that way.”

Niceness, in his framing, is often its own form of contempt, conflict-avoidant, performative, unwilling to engage seriously with ideas that challenge. Kindness is different. Patrick Collison delivers difficult feedback and disagrees directly. Satya Nadella inherited a Microsoft defined by stack-ranking and internal warfare and disbanded the toxic culture while raising expectations. Paul Graham described his purpose at YC as “trying hard to prevent assholes from getting funded.” Roger Federer was the most ferociously competitive player of his generation and never once diminished an opponent.

Hemant ties this directly back to GC’s investment thesis. Transforming healthcare, defense, energy, and education at the scale the firm envisions requires trust from governments, regulators, legacy institutions, and communities who have no obligation to extend it. Burning that trust for engagement metrics and personal brand isn’t just a cultural issue, it’s a business risk that compounds across every deal GC wants to do. His closing line captures the argument cleanly: “AI can’t cure cancer if we’ve convinced everyone it is a cancer.”

The quarterly review, in that sense, is itself part of the answer: slower, more honest, more willing to sit in the gray. It’s a bet that the industry’s most durable competitive advantage over the next decade won’t be capability. It will be whether we were worth rooting for.

Read the Q1 2026 Review

→ Listen on X, Spotify, YouTube, Apple

The material presented on Molly O’Shea’s website are my opinions only and are provided for informational purposes and should not be construed as investment advice. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular security, strategy, or investment product. Any analysis or discussion of investments, sectors or the market generally are based on current information, including from public sources, that I consider reliable, but I do not represent that any research or the information provided is accurate or complete, and it should not be relied on as such. My views and opinions expressed in any website content are current at the time of publication and are subject to change. Past performance is not indicative of future results.

Paid Endorsement. Brokerage services by Open to the Public Investing Inc, member FINRA & SIPC. Advisory services by Public Advisors LLC, SEC-registered adviser. Crypto trading provided by Zero Hash LLC, licensed by the NYSDFS. Generated Assets is an interactive analysis tool by Public Advisors. Output is for informational purposes only and is not an investment recommendation or advice. See disclosures at public.com/disclosures/ga. Matched funds must remain in your account for at least 5 years. Match rate and other terms are subject to change at any time.