BREAKING: Inside Accel - Cursor, Nebius, Cyera, Facebook..

Exclusive Interview w/ Late Stage Team

The ‘Quiet’ Silicon Valley Legend

Accel Late-Stage Partners Arun Mathew, Miles Clements, & Matt Weigand join Sourcery to go deep into the lore of the quiet, yet legendary, Silicon Valley firm.

→ Listen on X, Spotify, YouTube, Apple

We go back through Accel's 40 years of history, starting with the 10% Facebook stake and the secondary they modeled at 5X, which under-shot the outcome by an order of magnitude, and how the firm now runs a global AI portfolio spanning chips, neoclouds, labs, and applications, with exposure across Cursor, Anthropic, and Nebius.

The three have invested together for 15 years, and they break down how a generalist team wins competitive deals against flashier names, why late-stage returns are starting to match early-stage top quartile, and how check sizes moved from a $480M first growth fund to single investments north of $500M and, at times, over $1B.

Topics include Matt's $150M Nebius PIPE, now up 10-13X, and its $26B Meta deal; the "agentic influence" thesis behind the Lovable investment; Supabase growing 350% on nearly all inbound at 9M developers; Cyera's path from Series A to the highest-valued private security company; tokenmaxxing; and 3x trillion dollar IPOs.

We also get into the hot topics moving tech, AI, and investing right now: the agent economy and real enterprise adoption, the inference buildout and whether infrastructure is the rate limiter, AI optimization replacing SEO as the new distribution channel, the concentration of capital into a handful of late-stage rounds, security as an AI tailwind rather than a casualty after Mythos, the race toward $10 trillion companies, and what it means for retail when SpaceX, and others, finally hit the public markets.

𝐓𝐈𝐌𝐄𝐒𝐓𝐀𝐌𝐏𝐒

(00:00) Arun Mathew, Miles Clements, Matt Weigand, Partners at Accel

(00:49) Meet the Accel growth team

(01:48) The Facebook deal almost no one believed in

(06:19) The Thesis behind every Accel bet

(09:06) The silent strategy behind Accel's biggest wins

(09:51) The real reason Cursor picked Accel

(14:02) $200B into three companies in one quarter

(16:05) Early-stage vs. Late-stage returns

(17:18) Why trillion dollar companies are coming next

(20:13) The $26B Nebius deal, explained

(23:15) Building the AI infrastructure everyone will need

(26:22) The $150M bet that's up 13X today

(27:44) How agents are quietly rewriting enterprise software

(35:16) The three categories getting the biggest tailwinds

(36:35) From data security to AI security: the Cyera story

(39:48) How AI agents are creating infinite breach risk

(41:51) Is "token maxing" actually a real problem?

(44:22) Betting big on AI's exploding token economy

(47:53) Bracing for three Trillion Dollar IPOs

(51:05) What Accel is betting on next

(52:45) The unexpected place AI is already changing lives

Brought to you by:

Brex—The intelligent finance platform: cards, expenses, travel, bill pay, banking—wrapped into a high-performance stack. Built for scale. Trusted by OpenAI, Anthropic, Vercel, Granola, Deepgram, & Sourcery.. teams that move fast AF. visit → brex.com/sourcery

Turing—Turing partners with frontier AI labs to improve model capabilities in coding, reasoning, tool use, & multimodality, as well as with Fortune 500 enterprises to build & deploy end-to-end agentic AI systems in mission-critical workflows Visit: turing.com/sourcery

VCX—VCX is the public ticker for private tech, allowing investors of all sizes to invest in venture capital. View The Portfolio at GetVCX.com

Deel—Deel is the global people platform that helps startups hire, manage, pay, and equip anyone, anywhere. Trusted by more than 35,000 fast-growing companies, Deel is the people platform that just works, so teams can scale without the chaos. Visit: deel.com/sourcery

Public-–Investing platform Public just launched Generated Assets, which lets you turn any idea into an investable index with AI. With Generated Assets, you can build, backtest, refine, and invest in any thesis with AI. Gone are the days of one-size-fits-all ETFs. Try it today: public.com/sourcery

Inside Accel’s Growth Machine:

40 Years, 10% Facebook Stake, AI Supercycle

From a 10% Facebook Stake to Three Tech Cycles

Accel late-stage Partners, Arun Mathew, Miles Clements, & Matt Weigand, have worked together for 15 years at one of the most quietly dominant firms in Silicon Valley. The firm’s identity traces back to stakes that now read as inevitable but were anything but at the time. Accel led Facebook’s Series A in 2005 out of its early-stage fund and later held a stake reported at around 10%.

The story the partners keep returning to is the secondary. Accel created its growth vehicle in 2008, and one of its first opportunities was buying Facebook secondary shares shortly after Microsoft invested at a $15 billion valuation. Accel had the chance to buy in a little south of $20 billion. As Arun recalls the partner debate “We actually think this could be $100 billion business or more, that we could generate north of a 5X.” Both numbers proved far too conservative.

That miss is now cultural shorthand at the firm. “Lo & behold, that was way under-shooting what the opportunity and the potential of Facebook was,” Arun said. The lesson was not just about scale but about structural humility. Matt describes early partner Ryan Sweeney, who helped build the growth practice and drilled a specific discipline into the team, he “would remind us every day to be humble and to hustle.”

The through-line to today is the platform pattern. Miles points to Facebook as the first platform company the team watched founders build on top of, a dynamic he sees repeating now with the labs. The partners frame the current AI cycle as the same distribution shift they lived through once already, which shapes how aggressively they move on it.

→ Listen on X, Spotify, YouTube, Apple

Meet Arun Mathew, Miles Clements, & Matt Weigand

The growth team’s edge is overlapping coverage, not just tenure. All three partners joined Accel within a four-year window and have compounded relationships and pattern recognition across enterprise, infrastructure, & application software through multiple cycles.

Arun Mathew joined Accel in 2009 after starting as an associate at Insight Venture Partners, and holds degrees from the University of Pennsylvania (Wharton) and Stanford’s Graduate School of Business. He leads growth investments across enterprise, security, and infrastructure, and runs the firm’s Tech Council. His portfolio spans 1Password, Tenable, PagerDuty, Webflow, G2, Squarespace, and Qualtrics (acquired by SAP), alongside a deep India book that includes Flipkart, Freshworks, BookMyShow, and Ola. He also sourced Accel’s early investment in Groupon.

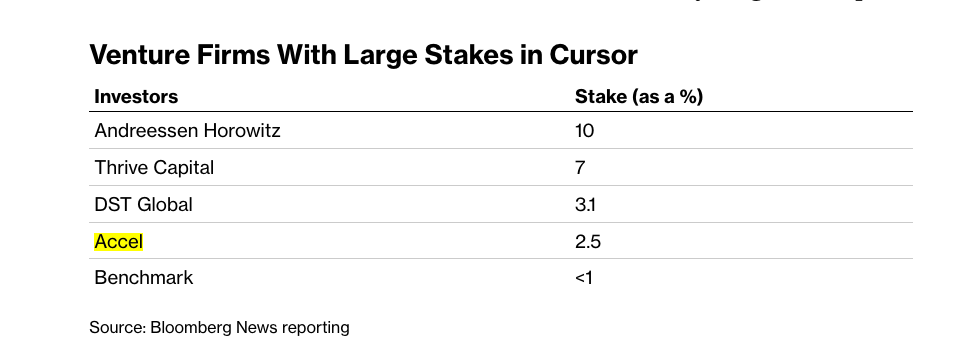

Miles Clements joined in 2009 as Accel’s first associate, coming from a product role at lynda.com (later acquired by LinkedIn), with degrees from the University of Virginia and Harvard. He helps lead the growth fund across AI, cloud, and enterprise software, and oversees Accel’s Ignite program for revenue leaders. He has led the firm’s investments in Linear (an $82 million round in March 2026 valued the company at $1.25 billion), Cursor ($60B SpaceX acquisition), Podium, and Laravel (a $57 million Series A), and worked on landmark deals in Atlassian and UiPath earlier in his career.

Matt Weigand joined in 2013 from William Blair’s technology investment banking group, & earlier Deloitte, with a degree from Miami University. He focuses on growth-stage enterprise software, security, fintech, and infrastructure. He led Accel’s $150 million Nebius PIPE and sits on the boards of Snyk, Cognite, Veriff, & DriveWealth, with active involvement across Scale AI, Axonius, G2, Xero, GoFundMe.

The Generalist Model & Why Late-Stage Now Rivals Early-Stage Returns

Accel’s growth team runs a generalist book with individual areas of depth. Arun concentrates on infrastructure and cybersecurity, Matt on infrastructure, and Miles on application software and developer tooling. Miles frames the requirement bluntly, in a market where categories appear & scale in months, an investor needs “some mental plasticity to wrap your head around these new categories as they evolve.”

The firm’s competitive edge, as the partners describe it, is reputation rather than marketing. Miles recounts asking Cursor CEO Michael Truell why he picked Accel in a crowded round. The answer “I asked around, & people said really nice things about Accel.” Matt adds that for most of the firm’s history, being first mattered above all “it was almost a religion here to be the first institutional investor into a company.”

The structural shift the team is underwriting is that late-stage returns are converging with early-stage. Matt notes that when he joined, Accel had roughly 90% coverage of every seed and Series A, a level no longer possible given how many companies now start. But a small cohort of outliers runs into the late stage, and Matt argues top-quartile late-stage funds will roughly match top-quartile early-stage this cycle. Brian Singerman, formerly of Founders Fund, made a similar point in a prior Sourcery interview.

The check sizes reflect the change. Accel’s first growth fund was $480 million. Single investments of $500 million, and at times over $1 billion, are now routine. Arun frames it as rational given the prize “if we believe that these companies can be trillion, multi-trillion dollar companies within a very short hold period, we should reflect that in check size.”

Six Investors: How Accel’s Partnership Is Built

For a firm operating across the full stack & three geographies, the late-stage engine is small. Matt notes about 6 investors deploy most of that capital, working in concert with the wider team. The continuity is the point “the three of us have worked together for 15 years, and a lot of it has grown from within.”

The firm’s investing philosophy rewards moving outside a lane. Arun cites Andrew Braccia, whom he calls “one of the best enterprise software investors in the last two decades,” despite a decade at Yahoo as a consumer internet operator. Braccia “led our seed investment into Slack early on.” Sameer Gandhi, a prolific consumer investor, became one of the firm’s leading cybersecurity investors. The instruction Arun draws from this is to hold focus and domain depth while staying open “it’s also really important to repot yourself and to look out.”

That model depends on a bench maturing into lead roles. Asked what he is most looking forward to, Miles pointed not to a company but to his younger colleagues, naming Ben Quazzo, Christine Esserman, Gonzalo Mocorrea, Josh Fang, & Rohan Kamat. Several have led investments that are not yet public knowledge, and Miles expects some to become known names in the coming months “I think we have some rising stars that are gonna really, really hit their stride.”

The takeaway for founders and LPs is that Accel’s edge is built on generational continuity rather than star individuals. A tight core, a wide bench, & a culture that pushes investors to keep repotting is how the firm sustains coverage as the market fragments.

Nebius, Neocloud Bet, & Inference Buildout

One of the most recent killer deals: $150 million PIPE into Nebius, led by Matt, roughly 16 months before the company became a consensus name. Miles, bragging on Matt’s behalf because “he’s not gonna brag on himself,” pegged the position as up 13X (as of June 2, 2026). The context around Nebius has since caught up to the thesis in the public data.

Nebius, the AI-infrastructure company built from the team that followed founder Arkady Volozh out of the former Yandex, reported Q1 2026 revenue of $399 million, up roughly 684% year over year, with AI cloud making up the vast majority of it. The company has guided to exit-2026 annualized run-rate revenue of $7 billion to $9 billion. It has signed roughly $46 billion in multi-year capacity contracts, headlined by a five-year deal with Meta reported near $27 billion and a Microsoft agreement around $17 billion, and Nvidia has committed to invest $2 billion. The stock has climbed well over 150% in 2026, putting the market cap in the high-$50-billion to high-$60-billion range.

Matt’s framing on Arkady captures why Accel structured a public-market investment at all “he is the most quietly humble killer I’ve ever met.” Nebius’ vision, in Matt’s telling, was a vertically integrated hyperscaler owning everything from the data center and server racks through the software layer, built for a world where inference demand compounds as agents proliferate.

That inference wave is the core of the bull case. Estimates vary widely across research shops, but multiple 2025 baselines put the AI inference market near $106 billion, growing to roughly $255 billion by 2030 at high-teens annual rates. Matt’s own read is that the buildout has barely started “I still view it as we’re inning one, and we’re just getting going.” Accel is pushing deeper into the stack alongside Nebius, including inference software from the ex-xAI team at RadixArk.

Agent Economy, Supabase, & “Agentic Influence”

The team’s clearest signal that agent adoption has moved from demo to production comes from its own portfolio telemetry. Arun points to Supabase, the Postgres-based backend for a large share of agent workflows “That’s growing 350% at hundreds of million dollars of scale, & they have virtually no salespeople. It’s all inbound.” Supabase has crossed 9 million developers, up from under 1 million when Accel first invested, with most of the growth in the last three or four months.

The mechanism, Arun argues, is a distribution shift from search engine optimization to what he calls AI optimization: coding tools like Claude and Codex now recommend backend products, and they favor the ones with the best developer experience. He notes roughly 60% of YC companies now choose Supabase, and that a framework easy for humans to use turns out to be easy for AI to use.

The pattern crystallized into a thesis Miles and Arun call “agentic influence.” After seeing simultaneous spikes across a Supabase board meeting and a Linear board meeting, the team recognized that “all of a sudden these agents are making decisions about downstream workflows and downstream tool creation.” The conclusion was to invest in every company sitting in that flow, especially the choke points metering the decisions.

That gave the team, working with partners Ben Fletcher & Zhenya Loginov, the conviction to back Lovable, and it reinforced existing positions in Vercel & Cursor. Arun’s broader point is that enterprise usage, not just vibe-coding hobbyists, is driving the curve, which he says gives him confidence the adoption is still in early innings.

Cursor & the $60 Billion SpaceX Acquisition

Cursor recurs throughout the interview as a portfolio company and as a canonical “choke point” in the agent economy. Miles describes a competitive early process and a second, conviction-led follow-on. Importantly, the episode was recorded before the deal below was finalized, so the partners discuss Cursor purely as a private holding and do not address an acquisition. The following is context added after taping.

Since recording, SpaceX agreed to acquire Cursor parent Anysphere in an all-stock deal valuing it at $60 billion, announced June 16, 2026 and expected to close in Q3 2026 pending regulatory approval. The transaction traces to an option SpaceX secured in April, which it exercised days after its Nasdaq IPO. Reporting describes it as one of the largest venture-backed startup acquisitions on record.

The financing mechanics underscore the “IPO as currency” theme the partners raise elsewhere. SpaceX debuted on Nasdaq on June 12, 2026, raising in the range of $75 billion to $86 billion and reaching a valuation above $2 trillion, then used its new public equity to move on Cursor within days. Cursor had reached roughly $4 billion in annualized revenue in under four years.

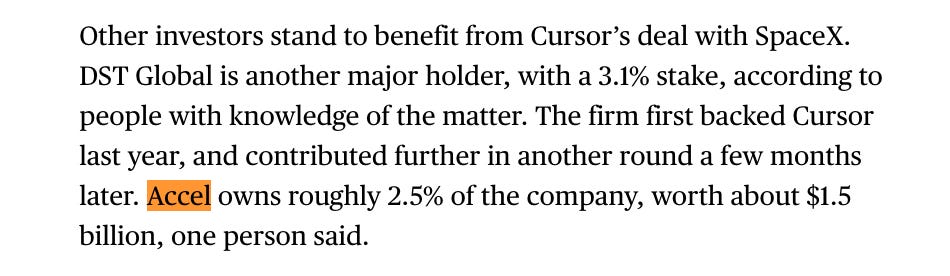

Bloomberg has solid coverage, complete with an estimated stake cap table.

Cyera & Why Security Became an AI Tailwind

Cybersecurity is one of three categories Arun flags as seeing dramatic tailwinds, alongside developer-first companies and AI infrastructure. The counterintuitive part is timing. After the release of the Mythos model, the market initially expected AI to kill incumbent security names. The opposite happened “The last six weeks for our security companies have been tremendous,” Arun said, pointing to CrowdStrike’s move over the same window.

Accel’s flagship position in the category is Cyera. Arun traces the firm’s data-security lineage back to Varonis in Israel, and credits London partner Philippe Botteri, who intersected Cyera CEO Yotam Segev on a biannual Israel trip, with sourcing the deal. Accel co-led the Series A with Sequoia, then leaned in through a difficult 2022 quarter to lead the Series B, and later led a subsequent round.

The public data confirms Arun’s claim that Cyera is among the most valuable private security companies. In June 2026 Cyera raised $600 million at a $12 billion valuation, led by Evolution Equity Partners with Accel participating, bringing total funding above $2 billion. That marked a roughly fourfold increase in about 18 months, following a $9 billion valuation in January 2026 and $6 billion in mid-2025. The company reports annual recurring revenue tripling for three consecutive years and roughly one-fifth of the Fortune 500 as customers.

Arun’s structural view is that value will concentrate, not fragment, he expects a few trusted platforms, Cyera, CrowdStrike, & Palo Alto Networks among them, to accrue most of the value as the attack surface expands. The driver is scale of creation: with hundreds of millions of people now building on AI, the surface area needing protection is growing at an exponential pace.

What Happens After Tokenmaxxing

“Tokenmaxxing,” the episodic overconsumption of model tokens, has grabbed headlines, but the team’s read is that the dominant trend runs the other way. Miles cites an Accel blind developer survey asking whether CFOs were pushing teams to spend less or more on consumption. The result “seven times more companies are being told to let it rip and spend more.”

Arun ties consumption directly to the pace of capability gains. Because what is possible on AI expands week to week, he argues the priority for most companies is deeper adoption rather than edge optimization, and that cost-cutting behavior will arrive only when the capability frontier plateaus. Matt frames the same point around forecasting history “I think you’re gonna see revisions up on tokens, for sure,” comparing it to every underestimated infrastructure forecast.

Matt does acknowledge a governor. Consumption scales only as far as the value returned, and if models asymptote in capability, the indigestion around token spend becomes real. For scale context, the broader AI market was estimated near $390.9 billion in 2025 and around $539.5 billion in 2026, a base against which even large token-spend figures represent early penetration.

The practical takeaway for operators is that current overconsumption examples are outliers that will be curtailed, while aggregate consumption keeps climbing. The team’s confidence rests on the absence of evidence that capability improvement is slowing.

3x Trillion-Dollar IPOs & the Race to $10 Trillion

The partners are constructive on the wave of mega-cap IPOs approaching the public markets, against a backdrop Miles describes as “an unmistakable concentration of capital around a handful of late-stage private companies,” with nearly $200 billion flowing into just two or three names in Q1 alone. Matt’s priority is durability over near-term volatility, the question that matters to him is “do I think those three companies have generational runs ahead of them, and I think they do.” He expects the debuts could be rocky early but favors being a long-term holder of the basket.

Arun frames the IPOs as a positive for market access, not just returns. He highlights the retail dimension of the SpaceX offering: “Elon reserving 30% of the SpaceX IPO for retail investors I think is a really great thing,” tying it to a broader cultural argument that ordinary investors have been shut out of this part of the cycle until now. He also connects that exclusion to the backlash against AI data centers.

The scale of the prize keeps expanding. Miles notes that 10 years ago no publicly traded company was worth $1 trillion, 5 years ago there were 5, and today there are 14, with several private pre-IPO candidates. His forward view “it’s fair to expect there will be $10 trillion companies and beyond over the next cycle.”

The closing note is applied rather than financial. Arun describes his wife, an ER doctor implementing an AI triage tool where “the early results from implementing this is that it made them 100% more effective.”

Matt’s most-anticipated development over the next 12 months is the same shift, AI value dispersing well beyond the small frontier of power users and outside Silicon Valley entirely.

→ Listen on X, Spotify, YouTube, Apple

The views expressed here are those of the individual personnel quoted and are not the views of Accel Management Co. L.L.C. or its affiliates (collectively, “Accel”). This content may include third-party advertisements; Accel has not reviewed such advertisements and does not endorse any advertising content contained therein. This content is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. You should consult your own advisers as to those matters. References to any securities or digital assets are for illustrative purposes only, and do not constitute an investment recommendation or offer to provide investment advisory services. Furthermore, this content is not directed at nor intended for use by any investors or prospective investors, and may not under any circumstances be relied upon when making a decision to invest in any fund managed by Accel. An offering to invest in an Accel fund will be made only by the relevant offering documentation of any such fund, which should be read in its entirety. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Accel, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Accel is available at https://www.accel.com/relationships.

The material presented on Molly O’Shea’s website are my opinions only and are provided for informational purposes and should not be construed as investment advice. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular security, strategy, or investment product. Any analysis or discussion of investments, sectors or the market generally are based on current information, including from public sources, that I consider reliable, but I do not represent that any research or the information provided is accurate or complete, and it should not be relied on as such. My views and opinions expressed in any website content are current at the time of publication and are subject to change. Past performance is not indicative of future results.

Paid Endorsement. Brokerage services by Open to the Public Investing Inc, member FINRA & SIPC. Advisory services by Public Advisors LLC, SEC-registered adviser. Crypto trading provided by Zero Hash LLC, licensed by the NYSDFS. Generated Assets is an interactive analysis tool by Public Advisors. Output is for informational purposes only and is not an investment recommendation or advice. See disclosures at public.com/disclosures/ga. Matched funds must remain in your account for at least 5 years. Match rate and other terms are subject to change at any time.