BREAKING: Inside VCX — The Public Venture Capital Fund

How VCX Put Anthropic & OpenAI Into Public Markets

The Rise of Public Venture Capital

Fundrise CEO Ben Miller breaks down the launch of Fundrise Growth Tech Fund (NYSE: $VCX) — one of the first publicly traded venture capital funds.

→ Listen on X, Spotify, YouTube, Apple

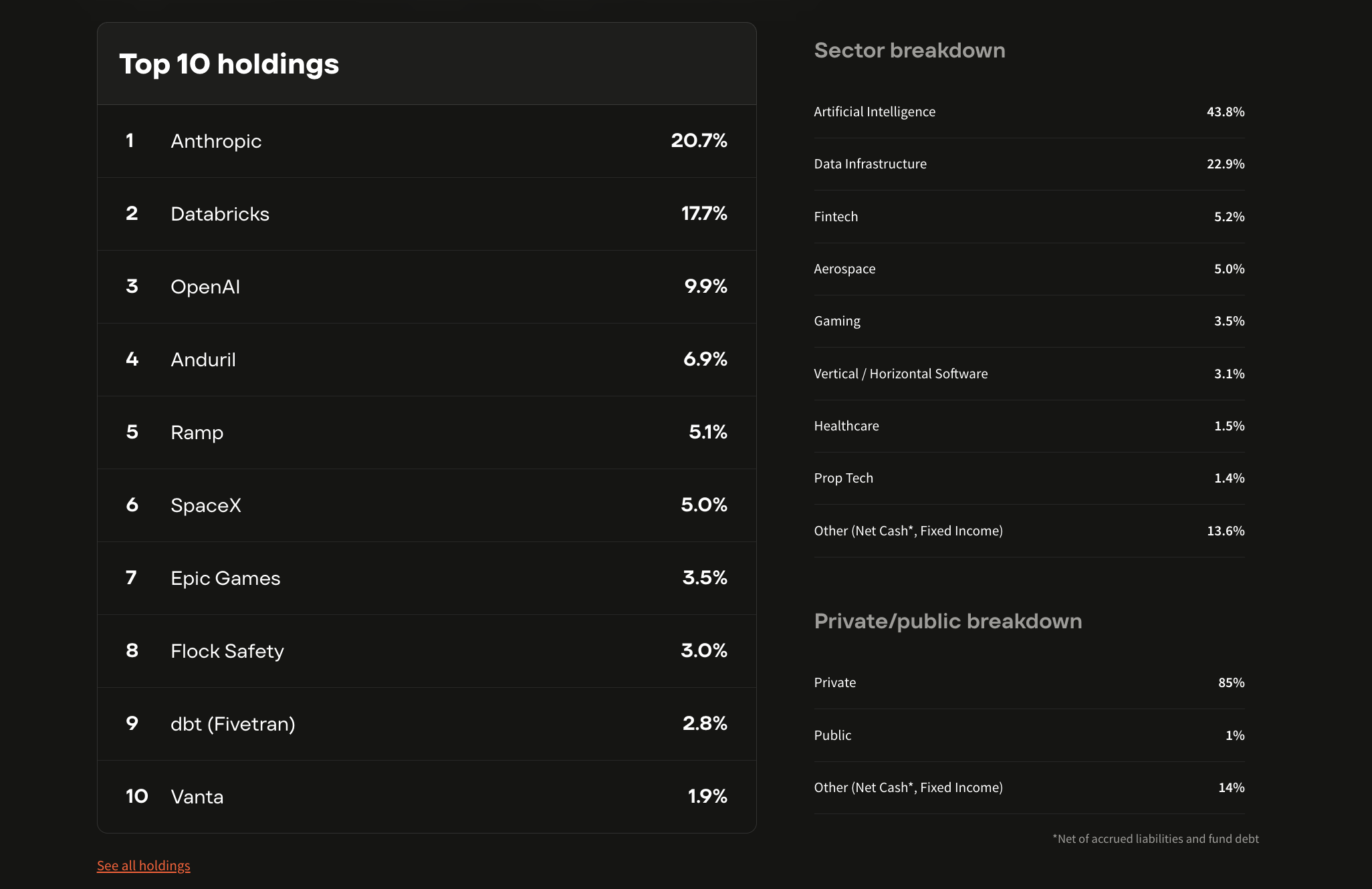

VCX debuted at roughly $700M valuation, then surged to ~$6.5B within 3 days, then hit +18x, with shares spiking to $575, way above the estimated net asset value (NAV) per share of $18.97, giving over 100,000 investors access to a portfolio of top private companies including Anthropic (~20%), Databricks (~17%), OpenAI (~10%), Anduril, Ramp, and SpaceX.

The timing reflects a broader shift: private markets are now where most value is created. VCX portfolio companies grew ~193% vs ~25% for public tech benchmarks, highlighting the gap between private and public market growth. Meanwhile, IPO timelines have stretched from ~3–5 years to 10–15+ years, meaning public investors are increasingly missing the highest-growth phase.

We discuss how VCX works as a closed-end fund, why it has traded at a premium (despite most closed-end funds trading at discounts), & how Fundrise accessed top-tier companies during the 2022–2023 venture downturn — including buying from distressed sellers and stepping into competitive rounds.

Finally, we explore what comes next: whether public venture capital becomes a standard allocation, how cycles and volatility impact the model, and what happens if public markets begin directly funding private tech at scale.

Topics Covered:

• VCX launch & NYSE debut dynamics

• Portfolio composition (Anthropic, OpenAI, Databricks, SpaceX)

• Private vs public market growth gap (193% vs 25%)

• Macro shift: value creation moving to private markets

• IPO window + why companies stay private longer

• How Fundrise sources and wins allocation

• Closed-end fund structure, NAV, premiums/discounts

• Risks: volatility, cycles, and downside scenarios

• Future of venture: rise of public VC funds

Subscribe to Sourcery for more conversations with the founders, investors, and operators shaping the future of tech, markets, and capital.

𝐓𝐈𝐌𝐄𝐒𝐓𝐀𝐌𝐏𝐒

(00:00) Benjamin Miller, Co-Founder & CEO at Fundrise

(01:12) The idea that almost got rejected

(04:27) How the 2023 crash created big opportunities

(05:54) From $700M to $6.5B in days

(07:38) How a closed-end fund works

(11:09) Inside the VCX portfolio (OpenAI, SpaceX, Databricks)

(14:50) What Robinhood and Destiny are doing

(17:02) Why private markets are pulling ahead

(21:38) IPO environment right now

(22:17) The SaaS apocalypse & market volatility

(25:55) What happens if VCX trades down

(27:39) How VCX moves through cycles

(31:25) How they decide where to invest

(35:45) Investment size and scale

(36:59) Most underrated portfolio company

(40:37) Biggest lesson: pain = success

(43:30) Origin story: why Fundrise exists

(47:12) Will big VC firms go public?

(50:52) Future of venture capital

(54:05) Biggest risks ahead

(57:18) Democratizing venture capital

(01:00:56) What’s next for VCX

(01:03:05) Dealing with skeptics

Brought to you by:

Brex—The intelligent finance platform: cards, expenses, travel, bill pay, banking—wrapped into a high-performance stack. Built for scale. Trusted by teams that move fast. visit → brex.com/sourcery

Turing—Turing delivers top-tier talent, data, and tools to help AI labs improve model performance, and enable enterprises to turn those models into powerful, production-ready systems. Visit: turing.com/sourcery

VCX—VCX is the public ticker for private tech, allowing investors of all sizes to invest in venture capital. View The Portfolio at GetVCX.com

Deel—Deel is the global people platform that helps startups hire, manage, pay, and equip anyone, anywhere. Trusted by more than 35,000 fast-growing companies, Deel is the people platform that just works, so teams can scale without the chaos. Visit: deel.com/sourcery

Public-–Investing platform Public just launched Generated Assets, which lets you turn any idea into an investable index with AI. With Generated Assets, you can build, backtest, refine, and invest in any thesis with AI. Gone are the days of one-size-fits-all ETFs. Try it today: public.com/sourcery

Inside $VCX: A New Structure for Accessing Private Technology Markets

NYSE Public Debut & Early Trading Dynamics

On March 19, 2026, the Fundrise Growth Tech Fund (VCX) began trading publicly, marking one of the first instances of a venture-style portfolio being made accessible through a listed vehicle.

The fund debuted at an approximate $700 million valuation and subsequently experienced significant upward trading activity, with shares in the last week reaching as high as $575, representing a substantial premium to its estimated net asset value (NAV) of $18.97 per share. This divergence reflects strong early demand for exposure to private technology assets, as well as the structural characteristics of closed-end funds, where market price is determined independently from underlying asset value.

At the time of listing, the fund had over 100,000 investors, indicating broad participation relative to traditional venture vehicles.

Portfolio Composition & Exposure

VCX provides investors with exposure to a concentrated portfolio of private technology companies, with a notable emphasis on artificial intelligence and data infrastructure.

As disclosed, key holdings include:

Anthropic (~20%)

Databricks (~18%)

OpenAI (~10%)

Anduril (~7%)

SpaceX (~5%)

This composition reflects a strategy focused on high-growth, category-defining companies, many of which remain private for extended periods. The ability to access these companies through a public market instrument is central to the fund’s value proposition.

Structure Details: How VCX Trades & Prices

A key aspect of VCX is how its closed-end fund structure differs from more familiar public market vehicles. While it provides exposure to private companies, investors are not directly buying shares in those companies. Instead, they are purchasing shares in a listed fund that holds those positions.

“The fund is listed, not the companies.”

VCX operates as a closed-end fund, meaning trading occurs at the fund level rather than through continuous creation and redemption of underlying assets. This distinction has important implications for pricing, liquidity, & how closely the fund reflects its underlying portfolio.

“The people are buying & selling the actual fund itself in the public markets.”

Because of this structure, the market price of VCX is determined by supply & demand for the fund’s shares. This can result in meaningful divergence from the fund’s net asset value (NAV), especially given that the underlying holdings are private and marked based on periodic funding rounds rather than continuous market pricing.

“You invest in private companies… typically mark at their last round valuation.”

This creates a dual-layer dynamic: a publicly traded price driven by investor demand, and a privately marked portfolio value that updates more gradually.

Summary of Structure

Investors buy shares of the fund, not the underlying private companies

The fund is a closed-end structure, not an ETF

Shares trade between investors on the public market

The fund does not continuously issue or redeem shares based on demand

Market price is driven by public supply and demand, not directly by NAV

Shares can trade at a premium or discount to NAV

Underlying holdings are private & typically marked to last funding rounds

The structure separates public market liquidity from private company operations

Massive Growth in Private Value Creation

The emergence of VCX is closely tied to broader structural changes in capital markets. Over the past decade, a growing share of value creation has shifted to private markets.

As discussed in the conversation, portfolio companies within VCX have demonstrated significantly higher growth rates relative to public benchmarks:

“The weighted average growth rate for our portfolio for VCX was 193%… the weighted average growth rate of public tech companies last year was 25%.”

At the same time, the timeline to public listing has extended materially. Companies that historically may have gone public within 3–5 years are now remaining private for 10–15 years or longer, concentrating the highest-growth phase outside public markets.

Structure: Closed-End Fund Mechanics

VCX is structured as a closed-end fund, which differs meaningfully from more familiar public market vehicles such as ETFs.

In this structure:

Shares of the fund trade on an exchange

The fund does not continuously issue or redeem shares based on demand

Market pricing is determined by investor sentiment rather than strictly by NAV

“A closed-end fund… the shares in the fund are trading rather than shares in the underlying asset portfolio.”

This structure allows the fund to hold illiquid private assets while still offering liquidity to investors. However, it also introduces the possibility of sustained premiums or discounts relative to NAV, as seen in early trading.

Sourcing & Access to Private Companies

A key question for any vehicle of this type is how it gains access to highly competitive private investments.

Fundrise’s entry into several portfolio companies occurred during the 2022–2023 market downturn, when venture capital sentiment was negative and liquidity pressures forced some investors to sell positions. This created opportunities to acquire stakes through secondary transactions and participate in rounds where capital availability was constrained.

“In 2023… people were selling their best assets… we bought from distressed funds who were having to sell.”

This combination of timing, opportunistic capital deployment, and positioning as a long-term partner enabled Fundrise to build exposure to companies that are typically difficult to access.

Implications for Venture Capital & Public Markets

VCX reflects a broader evolution in how capital may flow between private & public markets. As private markets expand, and companies delay or avoid IPOs, new structures may emerge to provide access to earlier stages of company growth.

Miller frames this as a longer-term shift:

“I think that like 10 years from now, every single person… will have 5% of their portfolio in public venture capital.”

At the same time, the model introduces new considerations, including pricing volatility, NAV transparency, and the cyclical behavior of premiums and discounts. The early trading of VCX (at a significant premium) highlights both the demand for private market exposure and the complexity of integrating illiquid assets into a public framework.

What Happens Next?

The Fundrise Growth Tech Fund (VCX) represents a notable experiment/innovation/development in market structure: a publicly traded vehicle providing access to private, high-growth technology companies.

Its early performance reflects strong demand for this exposure, while its structure raises important questions about pricing, liquidity, and long-term sustainability. More broadly, VCX sits at the intersection of two ongoing shifts, the expansion of private markets and the search for new ways to access them.

Whether this model becomes widely adopted will depend on how it performs across market cycles, but it clearly signals a growing interest in bridging the gap between private value creation and public market participation.

Questions to consider:

If private markets continue to capture the majority of value creation, can a public structure like VCX sustainably bridge that gap?

Can venture capital truly be made public without changing the characteristics that drive its returns?

Does this mark the beginning of venture capital becoming a public asset class, or the limits of trying to make it one?

Can liquidity & venture returns coexist, or are they fundamentally at odds?

If this model works, does it redefine how investors access innovation over the next decade?

→ Listen on X, Spotify, YouTube, Apple

The material presented on Molly O’Shea’s website are my opinions only and are provided for informational purposes and should not be construed as investment advice. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular security, strategy, or investment product. Any analysis or discussion of investments, sectors or the market generally are based on current information, including from public sources, that I consider reliable, but I do not represent that any research or the information provided is accurate or complete, and it should not be relied on as such. My views and opinions expressed in any website content are current at the time of publication and are subject to change. Past performance is not indicative of future results.

Paid Endorsement. Brokerage services by Open to the Public Investing Inc, member FINRA & SIPC. Advisory services by Public Advisors LLC, SEC-registered adviser. Crypto trading provided by Zero Hash LLC, licensed by the NYSDFS. Generated Assets is an interactive analysis tool by Public Advisors. Output is for informational purposes only and is not an investment recommendation or advice. See disclosures at public.com/disclosures/ga. Matched funds must remain in your account for at least 5 years. Match rate and other terms are subject to change at any time.

What becomes of the vcx fund as the holdings in private companies becomes holdings in public companies, post ipo?

Do the now publicly traded stocks remain in the vcx fund?

What do holders of vcx get as companies go public?

bought from distressed funds selling their best assets in 2023 - that's how you get anthropic at 20% of a public vehicle. the timing was the whole thesis and they executed it well