EXCLUSIVE: Coatue's Public Investments CIO on Anthropic, Semis, & AI's Biggest Market Shifts

Jaimin Rangwalla | Spring 2026 Public Markets Update

Follow the Gigawatts

Coatue’s Chief Investment Officer of Public Investments, Jaimin Rangwalla, joins Sourcery for an exclusive interview unpacking their latest Spring 2026 Public Markets Update amid one of the most unpredictable technology cycles of his 20-year career.

→ Listen on X, Spotify, YouTube, Apple

In our conversation, Jaimin breaks down how Coatue is thinking about the AI economy, including compute demand, hyperscaler spending, semiconductors, agents, and trillion-dollar private companies.

We cover:

OpenAI, Anthropic, & SpaceX are breaking into the world’s top 25 companies before going public

Anthropic adding $2.5 billion in ARR every single week

The tokenmaxxing economy

The rise of agents launching agents, creating what he calls a “digital population explosion” that will multiply everyone’s semiconductor & energy footprint by 1,000x

Why Coatue is "following the gigawatts"

The $12T funding engine behind the AI buildout

Sellers of shortage vs. buyers of shortage

The CPU/GPU flip reshaping compute demand

Coatue's $6T+ AI market estimate

Plus: the bottlenecks no one is solving, trillion-dollar IPOs coming, & what keeps him up at night.

Shoutout to Caryn, Joanna, Michael & the amazing team at Coatue!

Coatue’s Spring Public Markets Update Replay + Slides: https://www.coatue.com/blog/perspective/public-markets-update-2026-05-06

Chapters & breakdown below. Subscribe for more conversations with the investors and operators building the AI era.

𝐓𝐈𝐌𝐄𝐒𝐓𝐀𝐌𝐏𝐒

(00:00) Jaimin Rangwalla, CIO of Public Investments at Coatue

(00:56) Inside Coatue HQ

(02:48) Investor Update Kickoff

(04:36) Mapping the AI Stack

(06:02) Why Supply Stays Tight

(07:03) How Jaimin's Became CIO

(10:43) Private Giants vs Mag 7

(12:40) Market Breadth and Reordering

(15:24) Where AI Revenue Comes From

(17:04) Tokens and Economy

(19:43) Agents Change Everything

(21:58) OpenClaw Explained

(24:49) Memory Demand Explosion

(27:12) Architecture Shifts Ahead

(27:24) Agents Gain Memory

(27:58) CPU Demand Surge

(28:38) CPU GPU Ratio Flip

(30:21) Key Chip Players

(30:45) Intel Comeback Thesis

(31:41) Semis Go Mainstream

(33:24) Nvidia Mania and GTC

(33:59) Tracking Data Center Buildouts

(35:21) Jobs Lost and Created

(37:30) Sellers Versus Buyers

(40:54) Optical Breakouts

(41:27) Bottlenecks Everywhere

(44:48) Sentiment Versus Fundamentals

(47:10) Handling Volatility

(49:17) Finding New Leaders

(51:18) Trillion Dollar IPOs

(52:48) Risks and Disruptions

(55:00) Coatue Growth Story

(55:58) Staying Curious to Win

Brought to you by:

Brex—The intelligent finance platform: cards, expenses, travel, bill pay, banking—wrapped into a high-performance stack. Built for scale. Trusted by teams that move fast. visit → brex.com/sourcery

Turing—Turing accelerates superintelligence by helping frontier AI labs improve model capabilities and enabling enterprises to deploy end-to-end AI systems inside mission-critical workflows. Visit: turing.com/sourcery

VCX—VCX is the public ticker for private tech, allowing investors of all sizes to invest in venture capital. View The Portfolio at GetVCX.com

Deel—Deel is the global people platform that helps startups hire, manage, pay, and equip anyone, anywhere. Trusted by more than 35,000 fast-growing companies, Deel is the people platform that just works, so teams can scale without the chaos. Visit: deel.com/sourcery

Public-–Investing platform Public just launched Generated Assets, which lets you turn any idea into an investable index with AI. With Generated Assets, you can build, backtest, refine, and invest in any thesis with AI. Gone are the days of one-size-fits-all ETFs. Try it today: public.com/sourcery

Merge—The leading provider of customer-facing integrations and agentic tools for frontier LLMs, Fortune 500 organizations, and B2B SaaS companies. Visit: https://merge.dev

Coatue’s Spring 2026 Public Markets Update: Inside the AI Supercycle

In this conversation, Coatue CIO Jaimin Rangwalla walks through the firm's May 2026 investor update and the rate-of-change framework shaping how Coatue invests across AI, from gigawatts to agents to the trillion-dollar private companies reshaping public markets. Slides from the presentation added below.

→ Listen on X, Spotify, YouTube, Apple

A New Tech Cycle, Defined by Rate of Change

Every era of technology eventually finds its defining metric. For the internet it was page views; for mobile it was app downloads. For AI, according to Coatue’s Chief Investment Officer of Public Investments, Jaimin Rangwalla, it’s rate of change, and the rate is unlike anything he’s seen in nearly two decades on Wall Street.

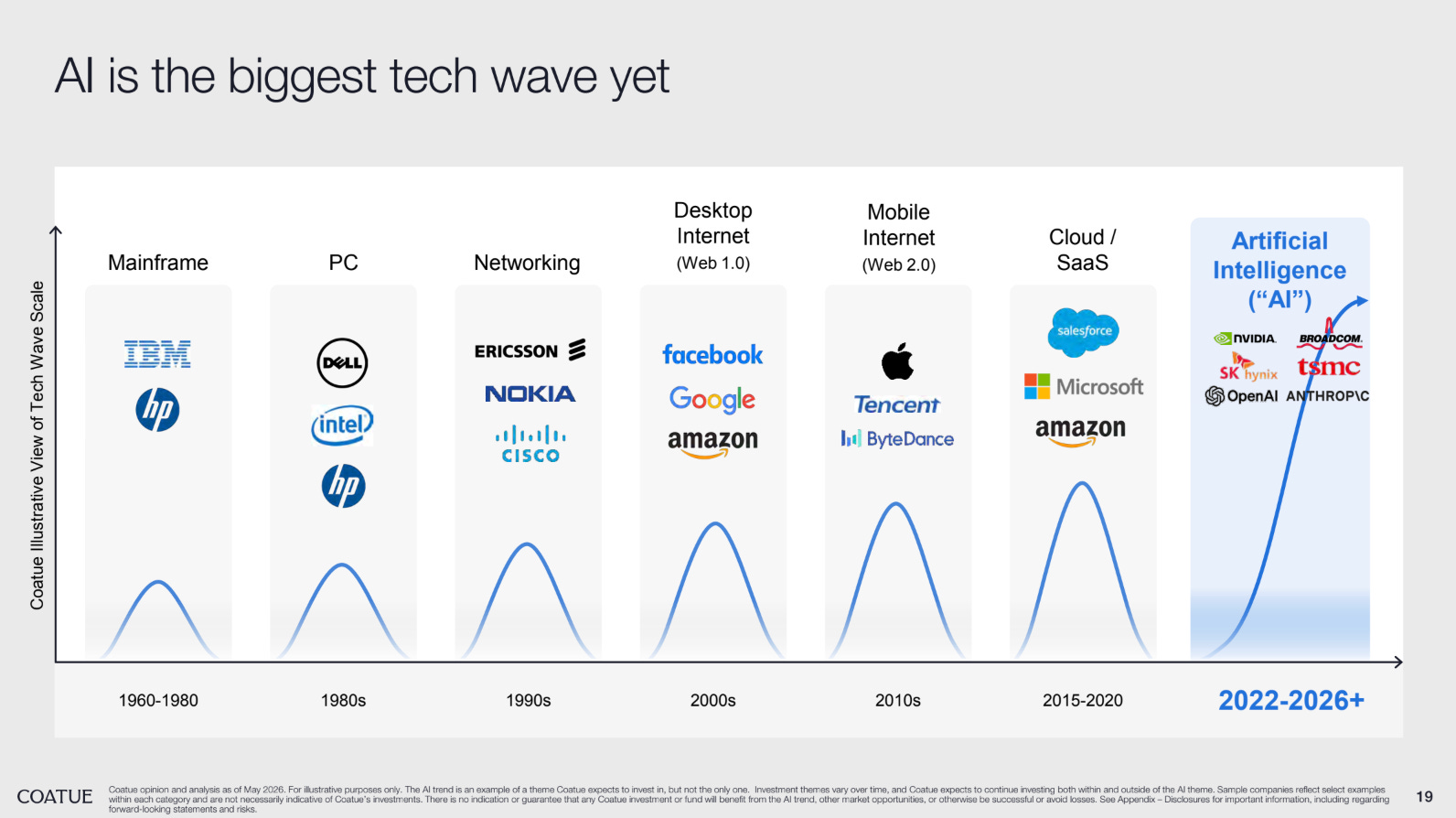

Coatue frames AI as the seventh and largest of the major tech waves, following Mainframe (1960 to 1980), PC (1980s), Networking (1990s), Desktop Internet (2000s), Mobile Internet (2010s), and Cloud/SaaS (2015 to 2020). The 2022 to 2026+ AI wave, in Coatue’s illustrative scaling (slide 19), towers over every prior one.

“AI is big and everyone can make these grand statements about how big it is.. but the most exciting part is the pace of the innovation, and you can look at that across, you know, how quickly companies have reached, you know, $10 billion, 30 billion, $50 billion of ARR.”

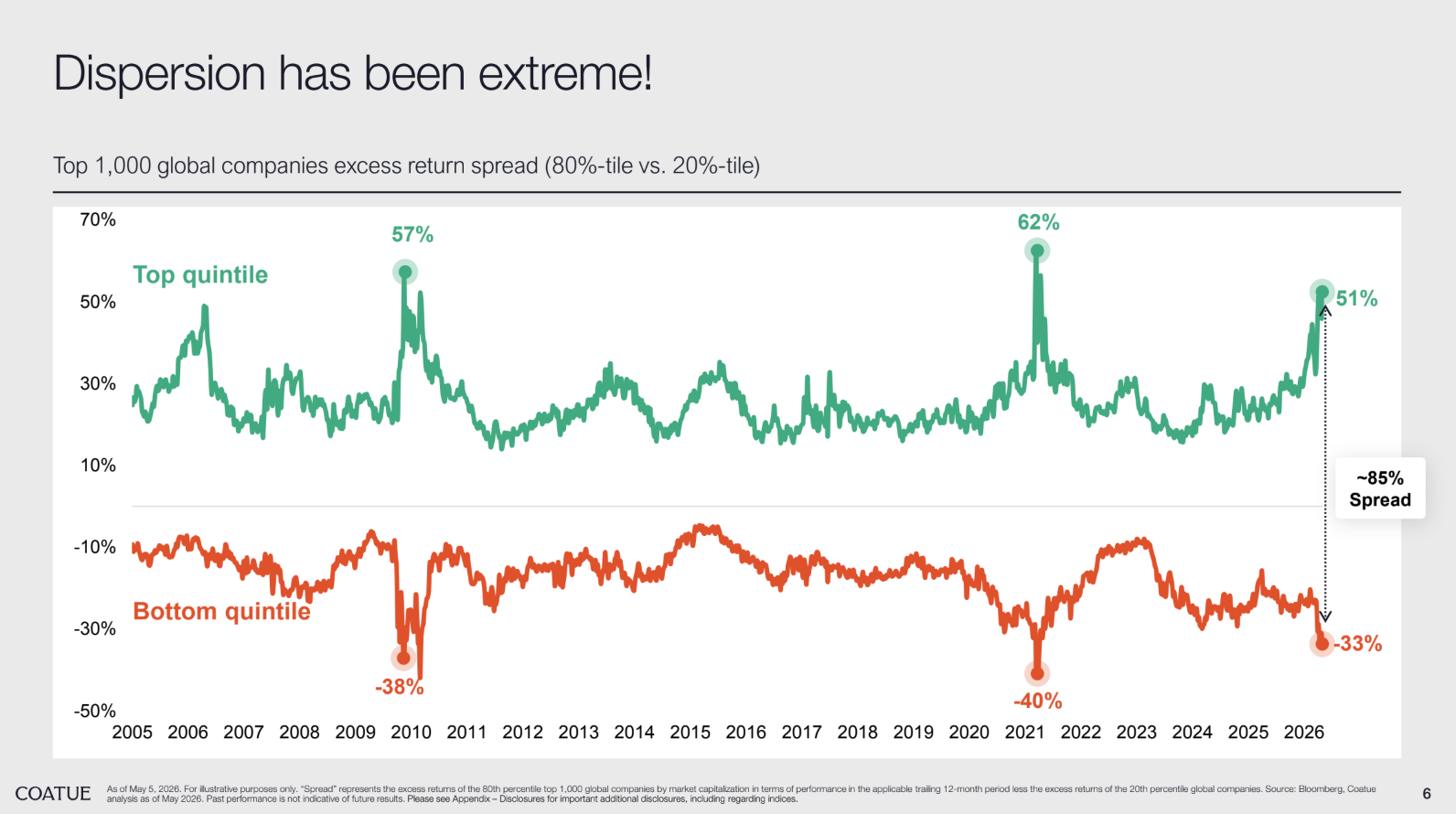

That pace is also visible in market dispersion. Coatue’s analysis of the top 1,000 global companies (slide 6) shows the spread between the 80th percentile and 20th percentile excess returns has reached roughly 85%, with the top quintile at +51% and the bottom at –33%, rivaling the 2009 and 2021 peaks of 57% and 62%.

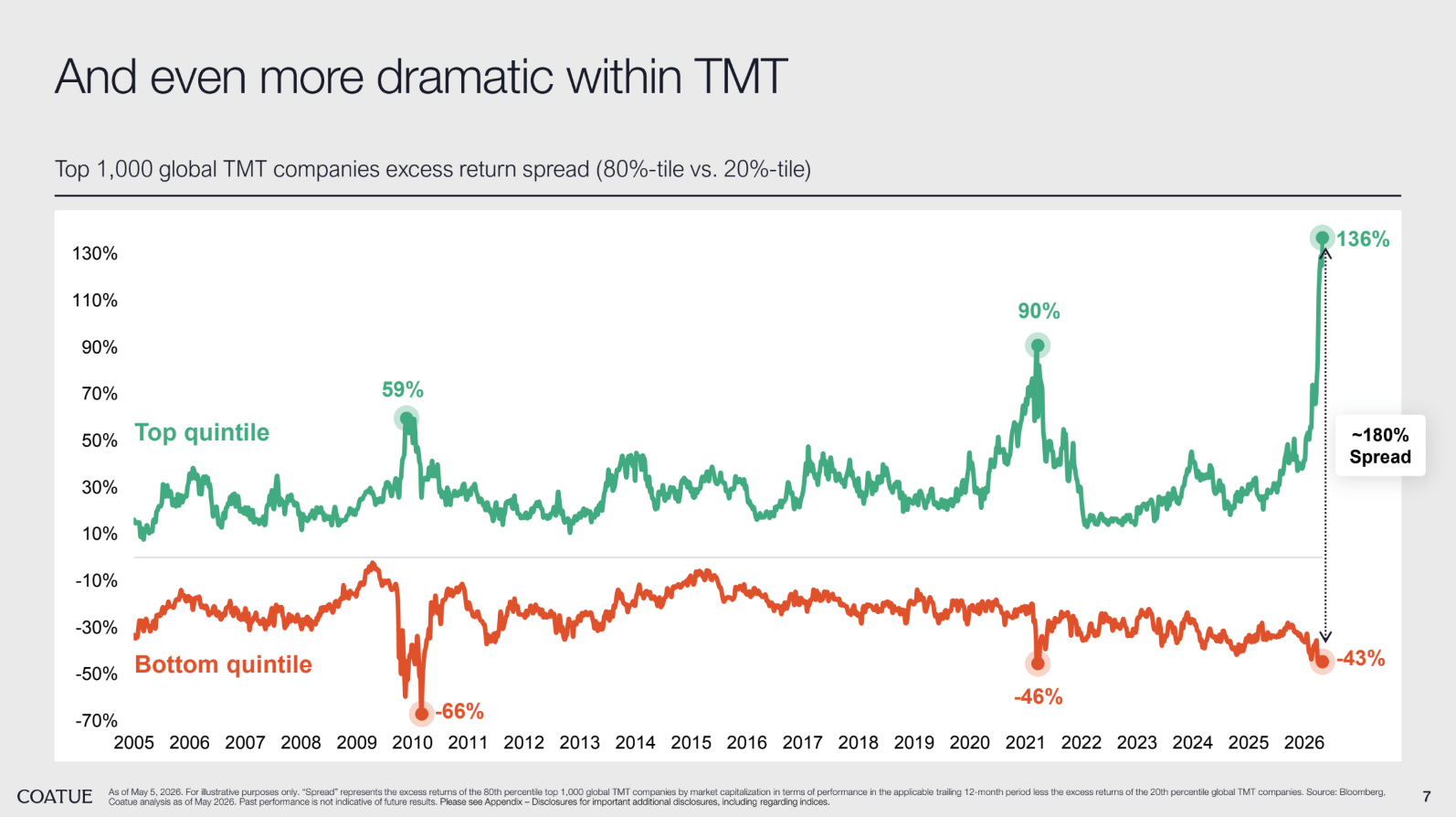

Inside TMT, the dispersion is even more extreme. The same spread analysis applied only to the top 1,000 global TMT companies (slide 7) shows a ~180% gap, with the top quintile delivering +136% while the bottom delivers –43%. That’s nearly triple the dispersion of the 2009 financial-crisis recovery and almost double the 2021 spike. The market is not rewarding “tech” broadly; it is rewarding a very specific slice of tech and punishing the rest.

What makes this cycle unusual is the absence of the typical flattening pattern. Adoption curves at the consumer, enterprise, and revenue levels are still bending upward rather than rolling over. “Even the biggest bulls I think aren’t capturing the size of the markets,” Jaimin said. Coatue is no longer organizing coverage by traditional sector buckets. Instead, analysts are sliced across the AI supply chain itself: “We’re almost thinking what slice of the AI supply chain, and then who are the people we’re gonna have covering those slices.”

Pictured: Michael Barton, Sector Head at Coatue, Coatue’s Tech Museum

Follow the Gigawatts

Two or three years ago, Coatue’s internal mantra was follow the GPU. Betting on NVIDIA early was right, but the team knew one stock was never the whole story.

“We bet on Nvidia early, but that’s usually not enough. Like what we really characterize a big theme being that there’s many ideas across a theme because there’s so many companies that are gonna be benefiting and impacting the, the forward kind of future of a theme.”

The framework has since evolved. The new shorthand is follow the gigawatts.

“The gigawatt is almost the, the atomic unit of where the growth in AI is coming from, and it’s one of the biggest shortages as well that’s out there.”

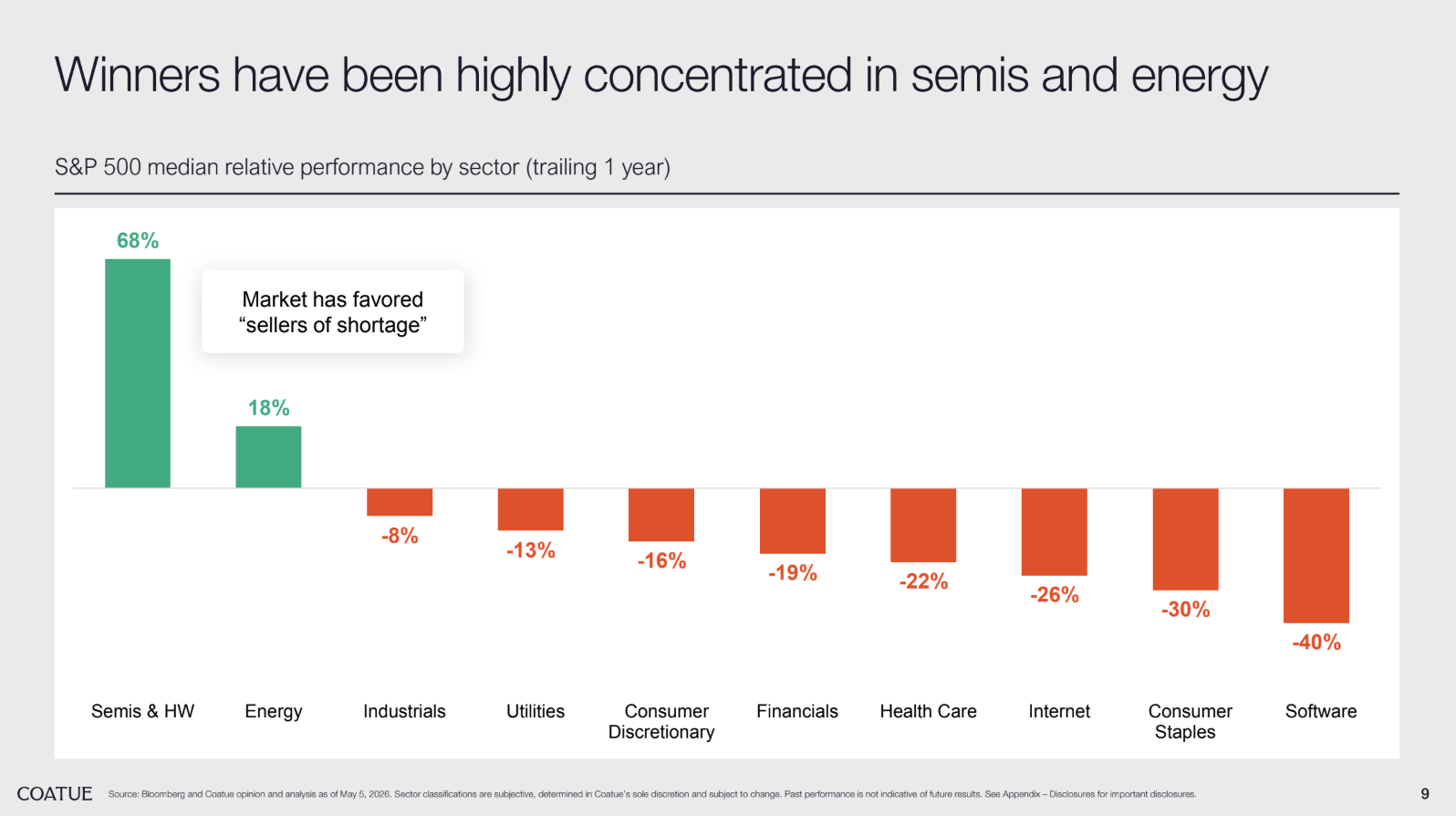

That shift is visible in trailing one-year S&P 500 sector performance (slide 9): Semis & Hardware lead at +68% and Energy comes in at +18%, while every other sector posts negative relative returns. Industrials are at –8%, Utilities –13%, Consumer Discretionary –16%, Financials –19%, Health Care –22%, Internet –26%, Consumer Staples –30%, and Software at –40%. Coatue captions the chart simply: “Market has favored ‘sellers of shortage.’”

From the gigawatt as the atomic unit, Coatue maps outward in every direction. What are the inputs to a gigawatt? What reduces its lead time? Who are the buyers? Who consumes the tokens produced by the gigawatt’s output? Each question opens a new investable surface area.

The biggest surprise, Jaimin said, has been how long the tightness has lasted. Memory suppliers are now signing guaranteed commitments through 2029 and 2030. “The fact that it is tight, and it almost seems like it’s getting tighter every week that goes by.” The buyers, he notes, are the largest companies in the world: “They are not investing hundreds and hundreds of billions of dollars growing at these high rates into something that they think is just gonna kinda peak and trough.”

Trillion-Dollar Private Club & a $6T+ TAM

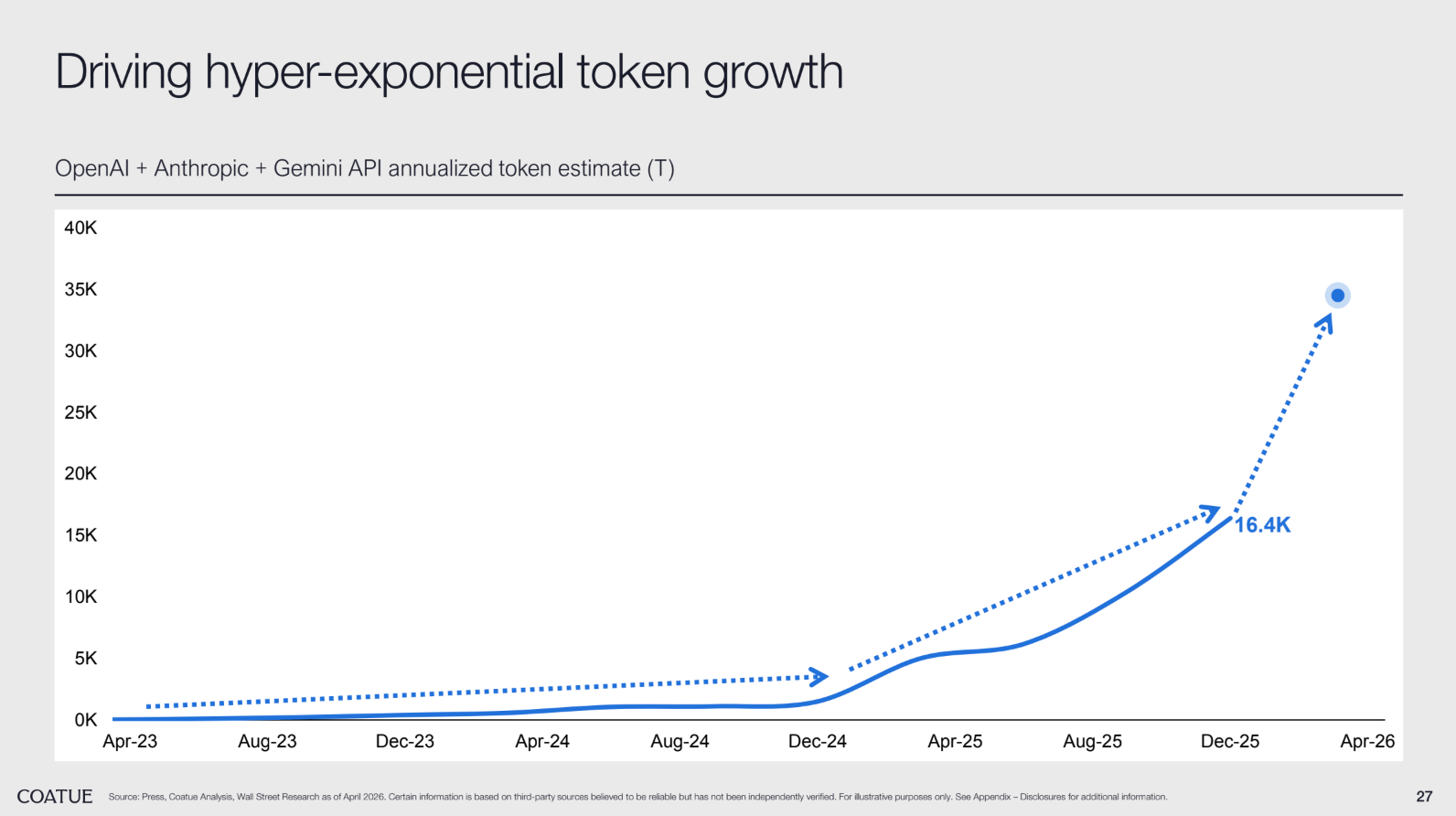

For most of modern market history, the largest technology companies became large after going public. Meta, the biggest of the Mag 7 at IPO, listed in 2012 at roughly $100 billion. That pattern has now broken. “Today you look, OpenAI’s most recent round was 800 plus billion dollars. SpaceX is most recent, when they did the transaction with xAI was $1.25 trillion. Anthropic’s last round was high $300 billions.” Three private companies have lodged themselves inside the world’s top 25 by valuation, before issuing a single public share.

The token data underwrites it. Coatue’s estimate of annualized API tokens generated by OpenAI, Anthropic, and Gemini (slide 27) sat near zero in early 2024, hit 16.4 trillion by late 2025, and is now tracking toward 35 trillion-plus on a trajectory that Coatue labels “hyper-exponential.”

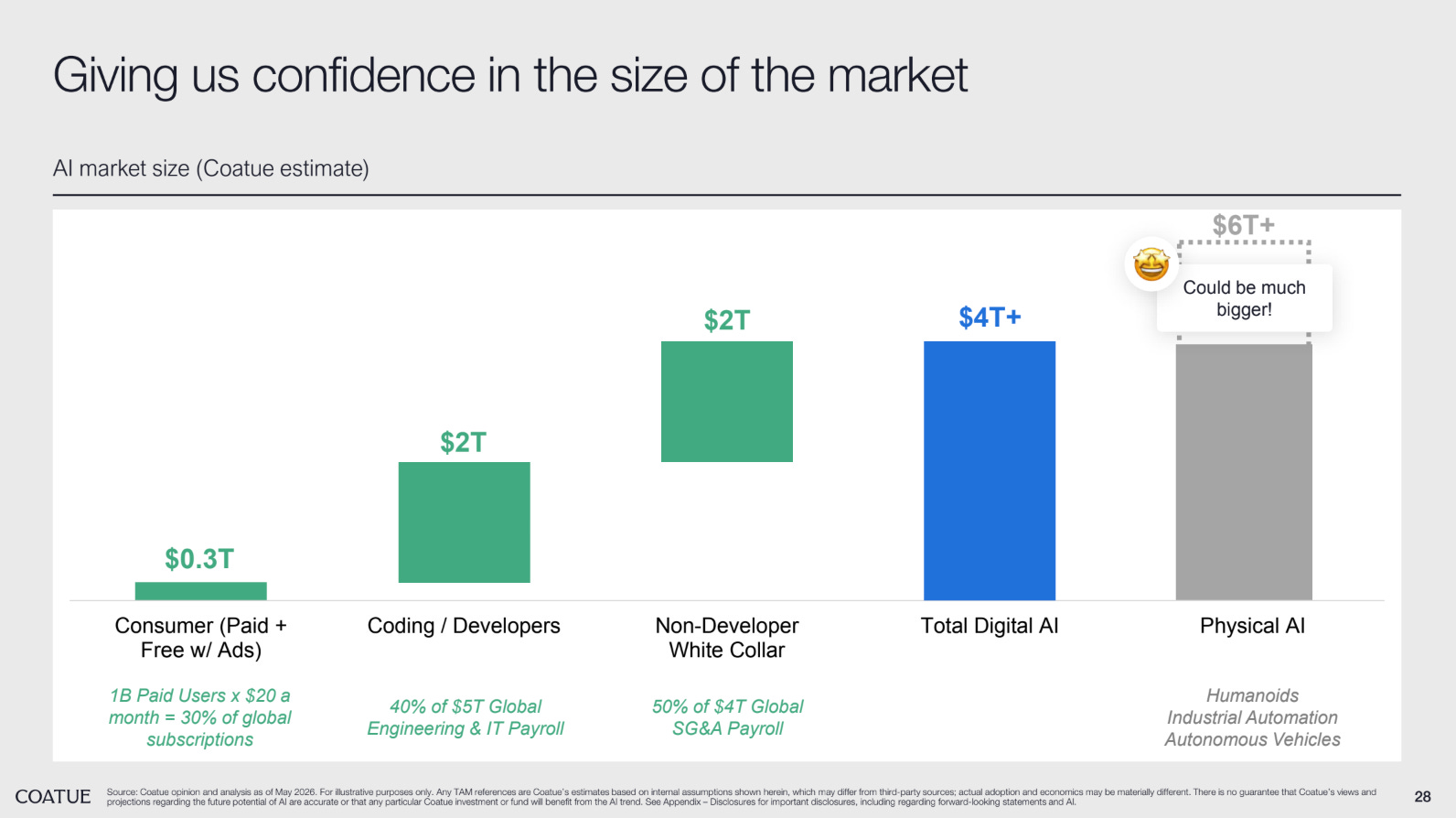

That growth gives Coatue confidence in a market sized at roughly $4 trillion-plus for digital AI alone, as detailed (slide 28):

$0.3T from consumer (a billion paid users at $20 per month equating to ~30% of global subscriptions)

$2T from coding and developers (40% of the $5T global engineering and IT payroll)

$2T from non-developer white-collar work (50% of the $4T global SG&A payroll)

Add physical AI (humanoids, industrial automation, autonomous vehicles), and the TAM climbs to $6T+. Coatue’s annotation: “Could be much bigger!”

AI Revenue Acceleration & the $12T Funding Engine

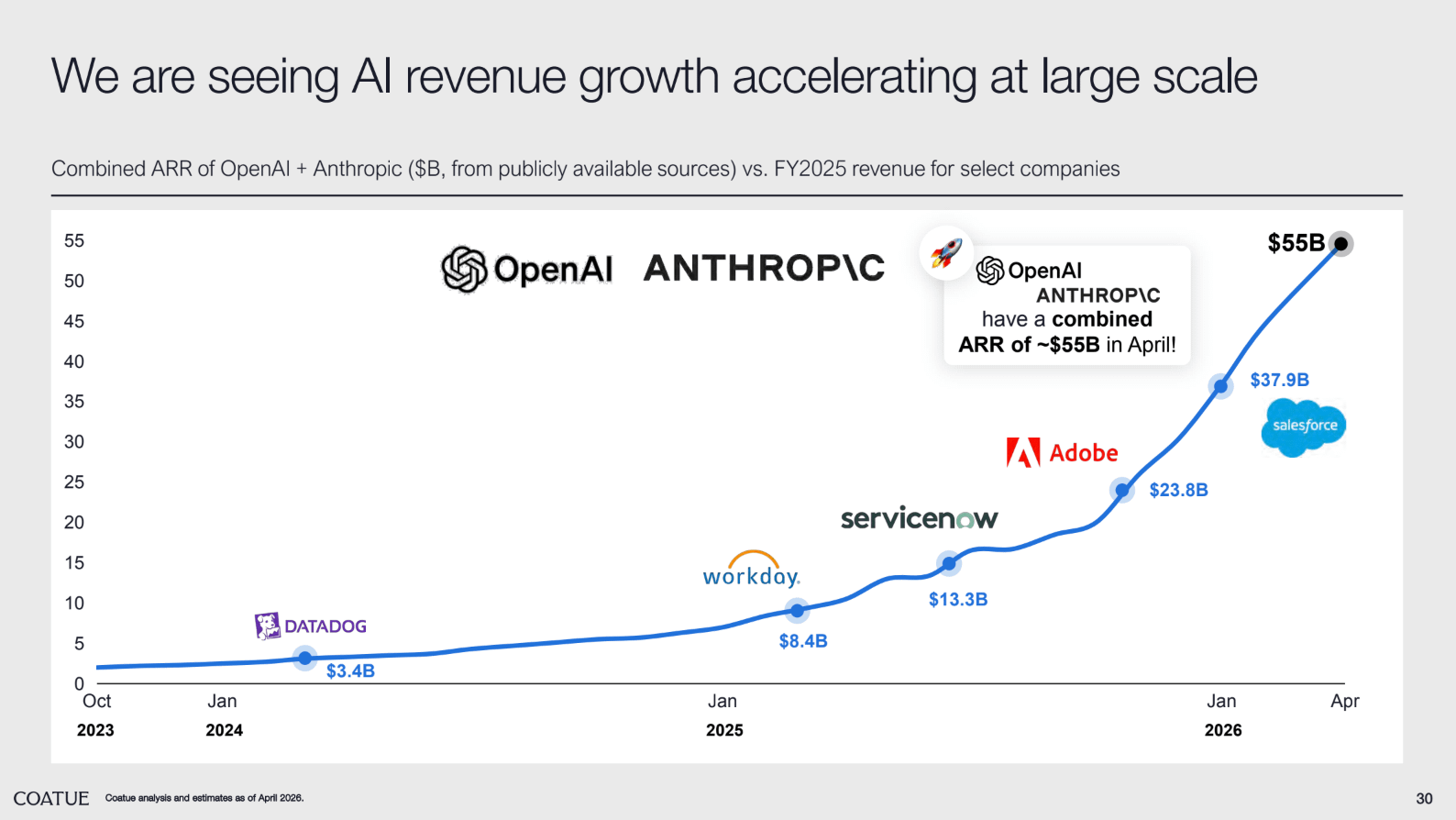

If the TAM defines the ceiling, two charts in the deck show how quickly the industry is climbing toward it. Slide 30 plots the combined ARR of OpenAI & Anthropic against FY2025 revenues of established software franchises, & the line is near vertical.

The combined number sat at $3.4B in early 2024 (smaller than Datadog), reached $8.4B by January 2025 (Workday-scale), $13.3B mid-2025 (ServiceNow-scale), $23.8B by late 2025 (Adobe-scale), $37.9B by January 2026 (Salesforce-scale), and then.. OpenAI & Anthropic reached a combined ARR of ~$55B by April 2026.

Jaimin’s framing in conversation underscores the velocity. “They’re adding $10 billion plus or minus a month, almost $2.5 billion a week. Most of the companies in the SaaS universe don’t even have $2.5 billion of ARR annually, right? They’re adding that in a week.” The companies on the comparison line each took 15 to 25 years to reach their current scale. OpenAI and Anthropic compressed the same trajectory into roughly 24 months.

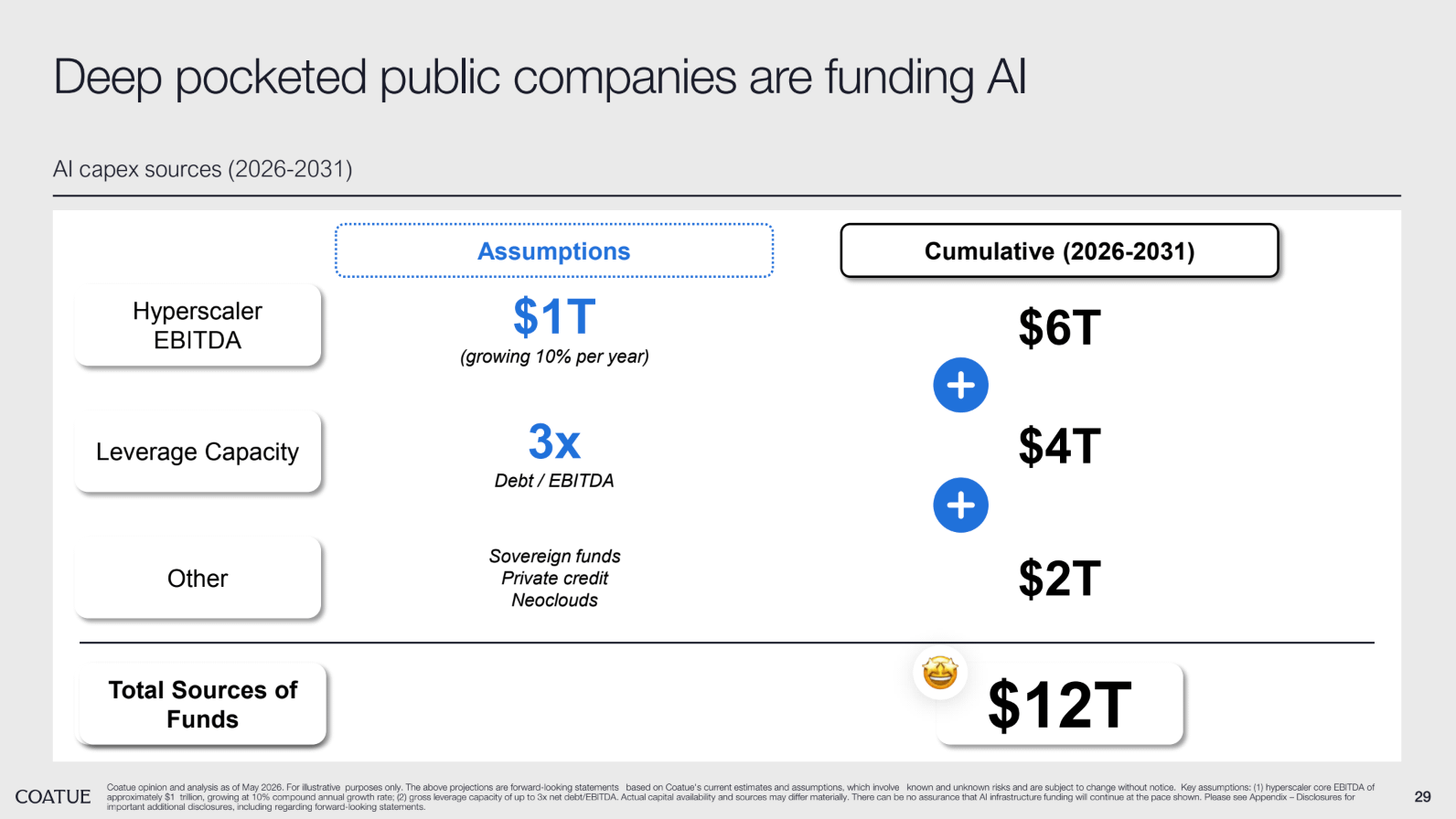

The question that naturally follows is how this gets paid for. Slide 29 lays out Coatue’s AI capex funding model for 2026 to 2031. Hyperscaler EBITDA contributes a base of ~$1T per year, growing at 10% annually, which compounds to $6T cumulative over the period. Layering on 3x debt-to-EBITDA leverage capacity adds another $4T. Sovereign funds, private credit, and Neoclouds contribute an additional $2T. The total: $12T of cumulative funding sources for AI infrastructure through 2031.

That number reframes the entire debate about whether AI capex is sustainable. The buyers of shortage are not stretching to fund this build-out; they are funding it from operating cash flow and modest leverage, with sovereign and private capital filling the remainder. As Jaimin put it: “They are not investing hundreds and hundreds of billions of dollars growing at these high rates into something that they think is just gonna kinda peak and trough.”

Tokens, Agents, & the Digital Population Boom

If gigawatts are the atomic unit of supply, tokens are the atomic unit of demand. “Basically, a token is the unit of thought by any AI model,” Jaimin explained. “It’s like a unit of intelligence.” Unlike human cognition, AI cognition can be priced, metered, and forecasted, and that property is reshaping how Coatue models every company in the AI stack.

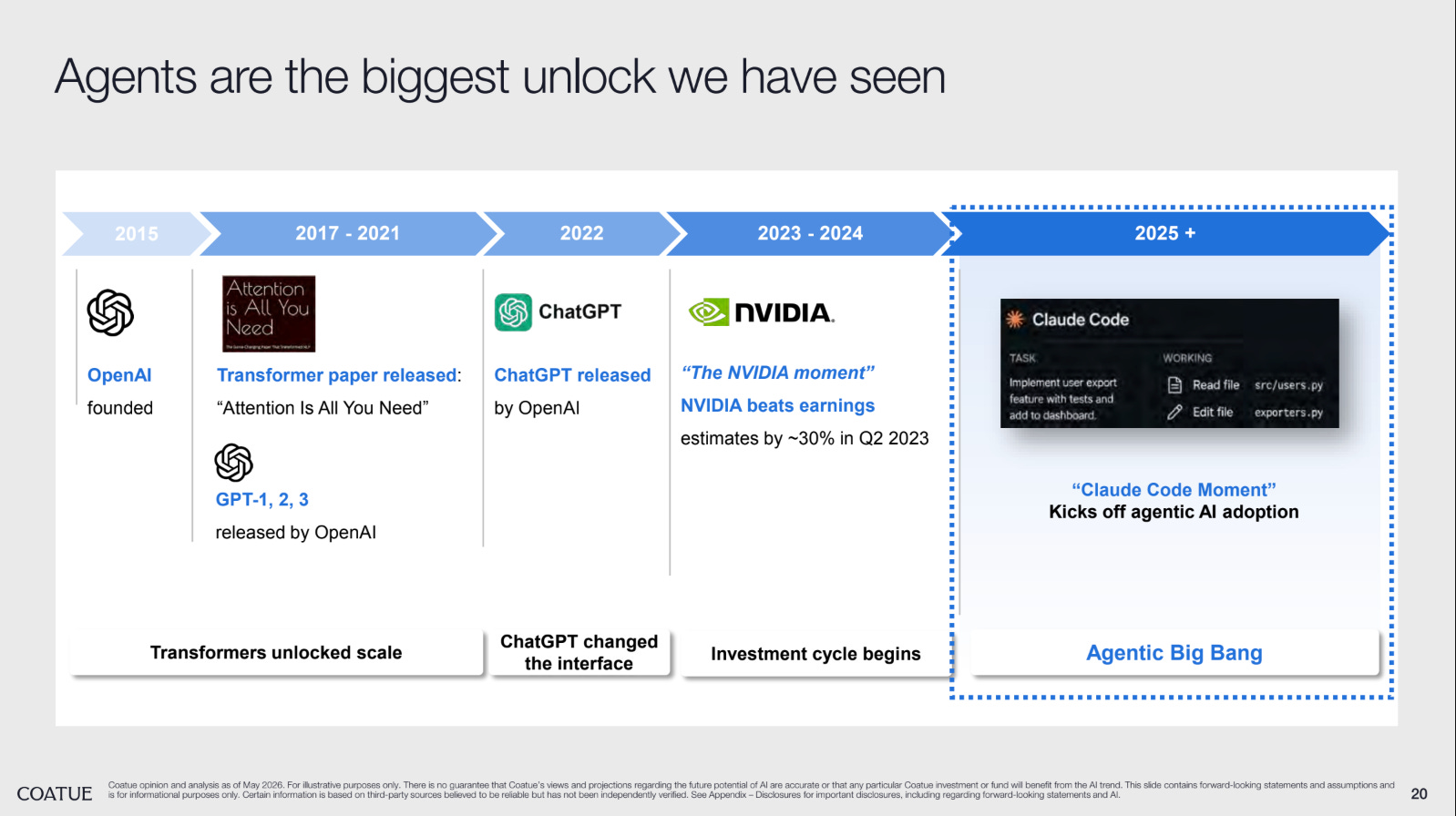

The unlock that turned tokens into an economy was agents. Coatue maps the catalyst timeline (slide 20): 2015 OpenAI founded, 2017 to 2021 transformer paper and GPT-1, 2, 3 (”Transformers unlocked scale”), 2022 ChatGPT (”changed the interface”), 2023 to 2024 the NVIDIA moment as it beat Q2 2023 estimates by ~30% (”Investment cycle begins”), and 2025+ what Coatue calls the “Claude Code Moment,” the “Agentic Big Bang.”

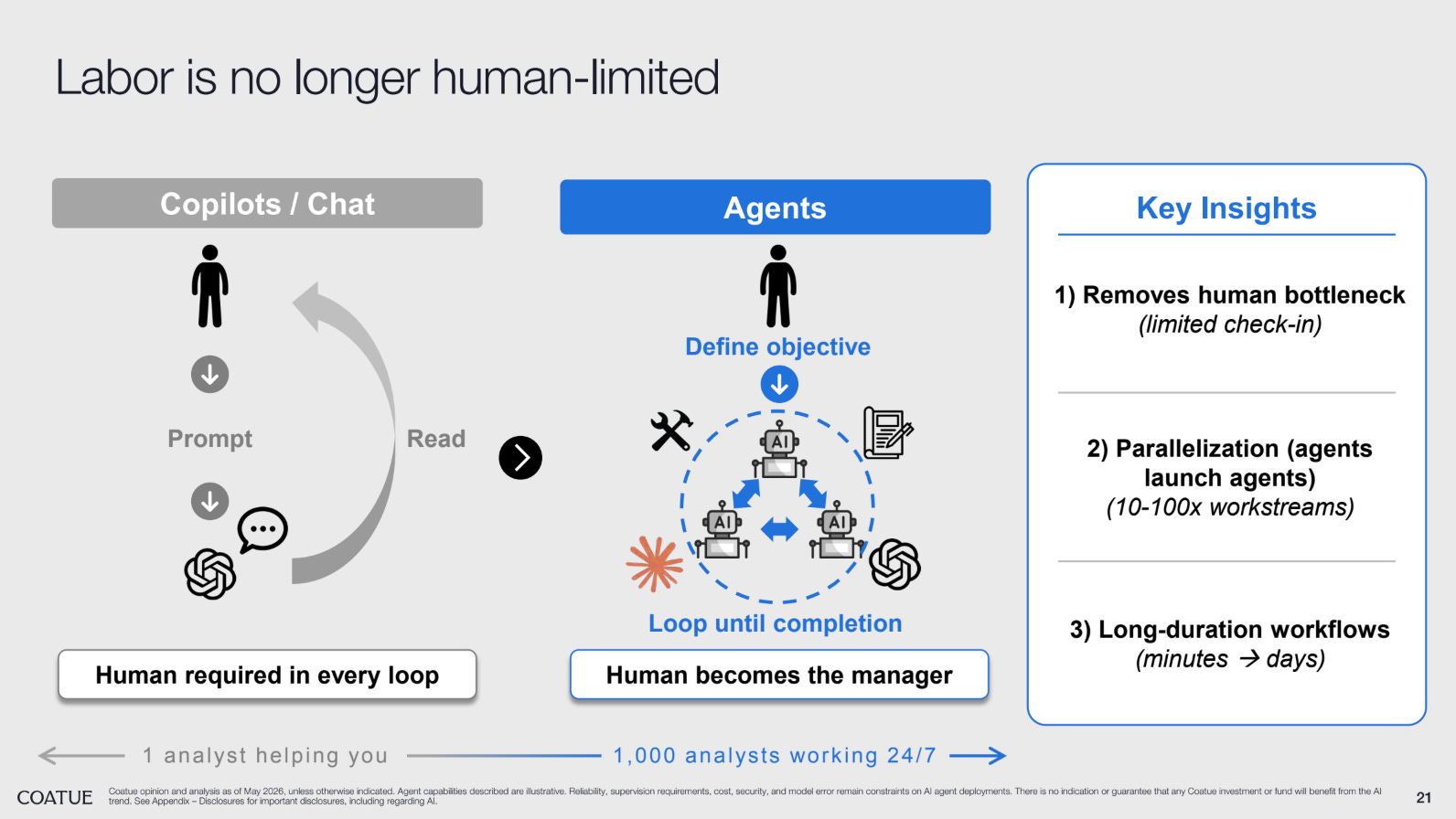

Slide 21 captures the shift: agents launching agents removes the human bottleneck, parallelizes work by 10 to 100x, and stretches workflows from minutes to days. The model moves from “1 analyst helping you” to “1,000 analysts working 24/7.”

Jaimin describes his own workflow: open a Claude session, assign a task, open another, assign another. “You’re able to launch agents, and then you’re able to launch multiple pools of agents that also launch multiple agents below. And so to me, it’s just the sheer power of exponential growth of the number of agents and the amount of work that’s being done.” Coatue captures the consumer endpoint (slide 25) in one phrase: “Your phone becomes your remote!” A WhatsApp interface fans out into a tree of dozens of agents, each spawning subagents, each acting on the user’s behalf in parallel.

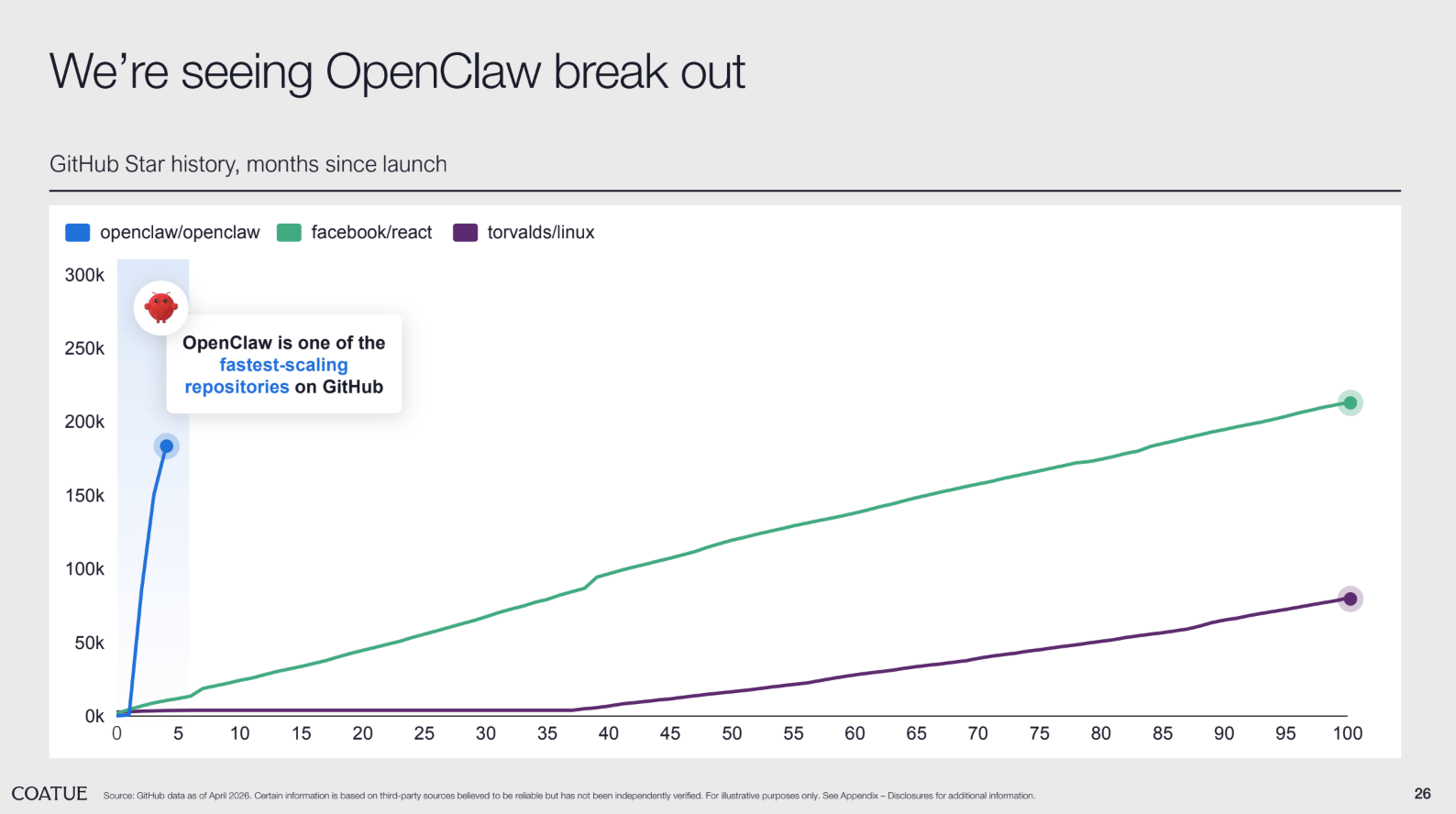

The breakout is already visible in developer tooling. Coatue’s GitHub Star History chart (slide 26) shows OpenClaw accumulating roughly 190,000 stars in its first ~4 months, a trajectory it labels “one of the fastest-scaling repositories on GitHub,” running near-vertical against React (which took ~100 months to reach ~215,000) and Linux (~80,000 over the same window). Project that forward and the implications for infrastructure could go even furhter: “In a year or two, we’re gonna have a claw that’s running hundreds of agents at all time.”

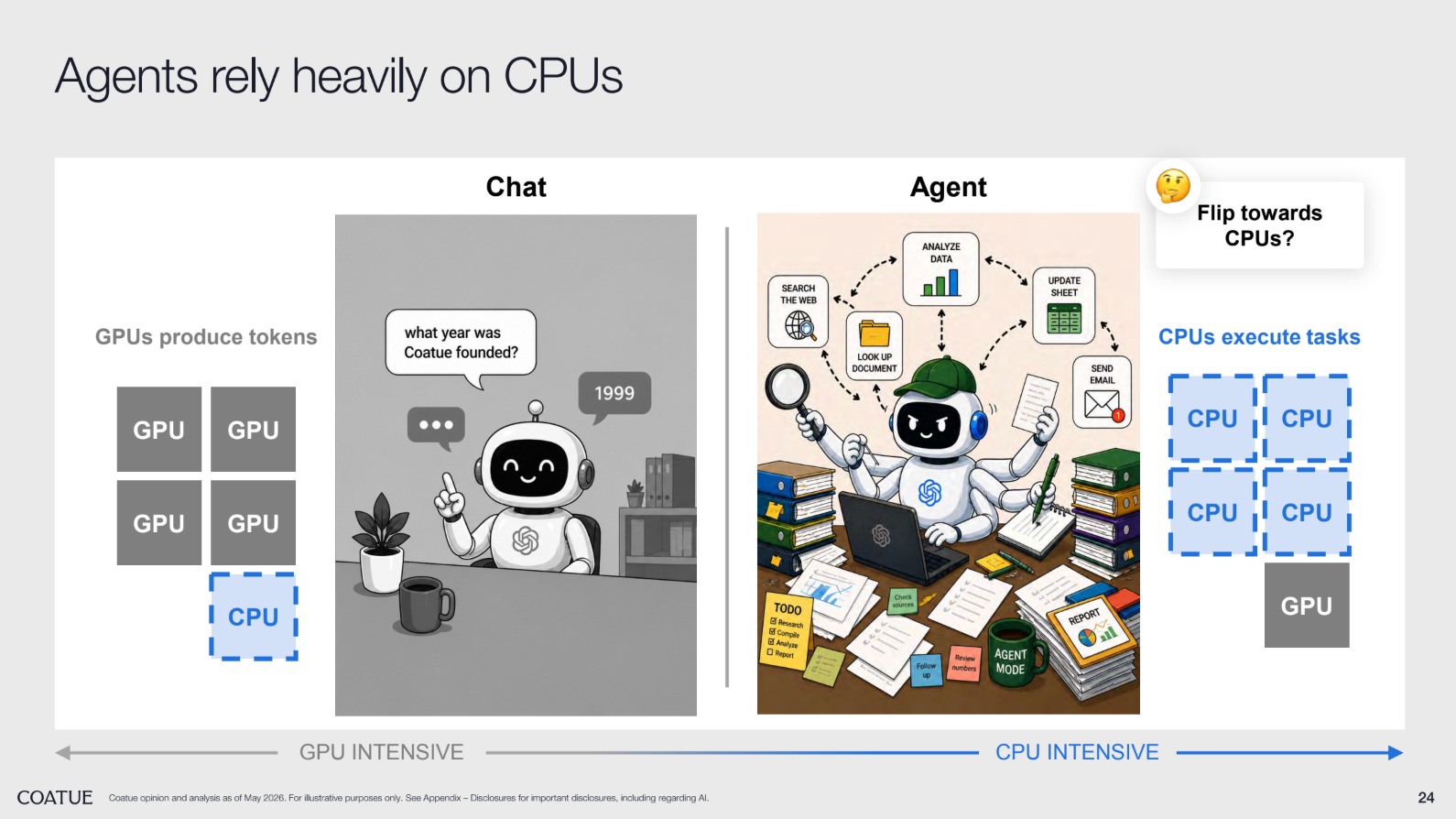

The Great CPU-GPU Flip

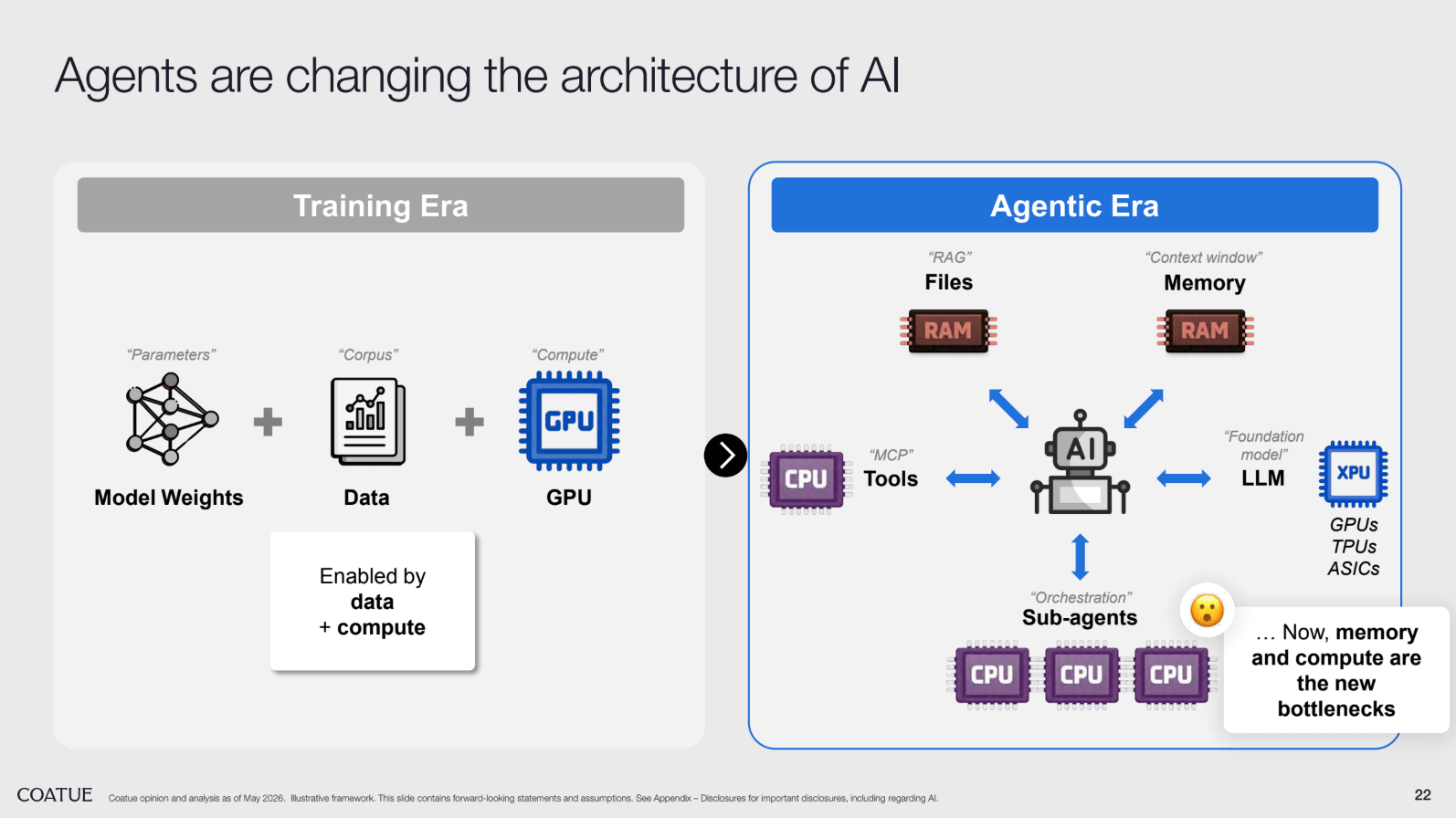

In the Training Era, the recipe for AI was simple: model weights plus data plus GPU. In the Agentic Era, the architecture has fragmented. Coatue’s diagram (slide 22) shows the agent at the center, surrounded by RAG-based file access, context-window memory, MCP tools, orchestration via sub-agents, the underlying LLM foundation model, and a mix of accelerators (GPUs, TPUs, and ASICs). With a clear message: “Now, memory and compute are the new bottlenecks.”

For most of the last four years, the compute ratio was lopsided: one CPU for every eight GPUs, sometimes one for sixteen. CPUs handled the final orchestration step; GPUs did everything else. Agents are quietly inverting that. “Now the ratio is actually moving from to one CPU to four GPUs, and so it’s improved kind of by 2X already, and we think it actually has a chance to flip the opposite direction, which is one GPU to four CPUs.” Some on Coatue’s team think it could go to one GPU per eight CPUs, embedding a 16x expansion of the CPU market opportunity inside the same workloads driving GPU demand.

The reason is architectural, illustrated (slide 24). Chat workloads are GPU-intensive: a single question, a single token-generating response. Agent workloads are CPU-intensive: search the web, look up a document, analyze data, update a sheet, send an email, long chains of serial subtasks, each calling tools, each requiring orchestration. Coatue’s visual flips the compute footprint accordingly: where a chat workload uses four GPUs and one supporting CPU, an agent workload uses four CPUs and one GPU.

That shift has implications for who wins. “On the CPU side, it’s Intel, AMD, and Arm,” Jaimin said. He’s particularly constructive on Intel, a company that spent years as semiconductors’ forgotten child but now has new leadership and clean math. “Some of the best thesis are the simple thesis, and you don’t wanna overthink it.”

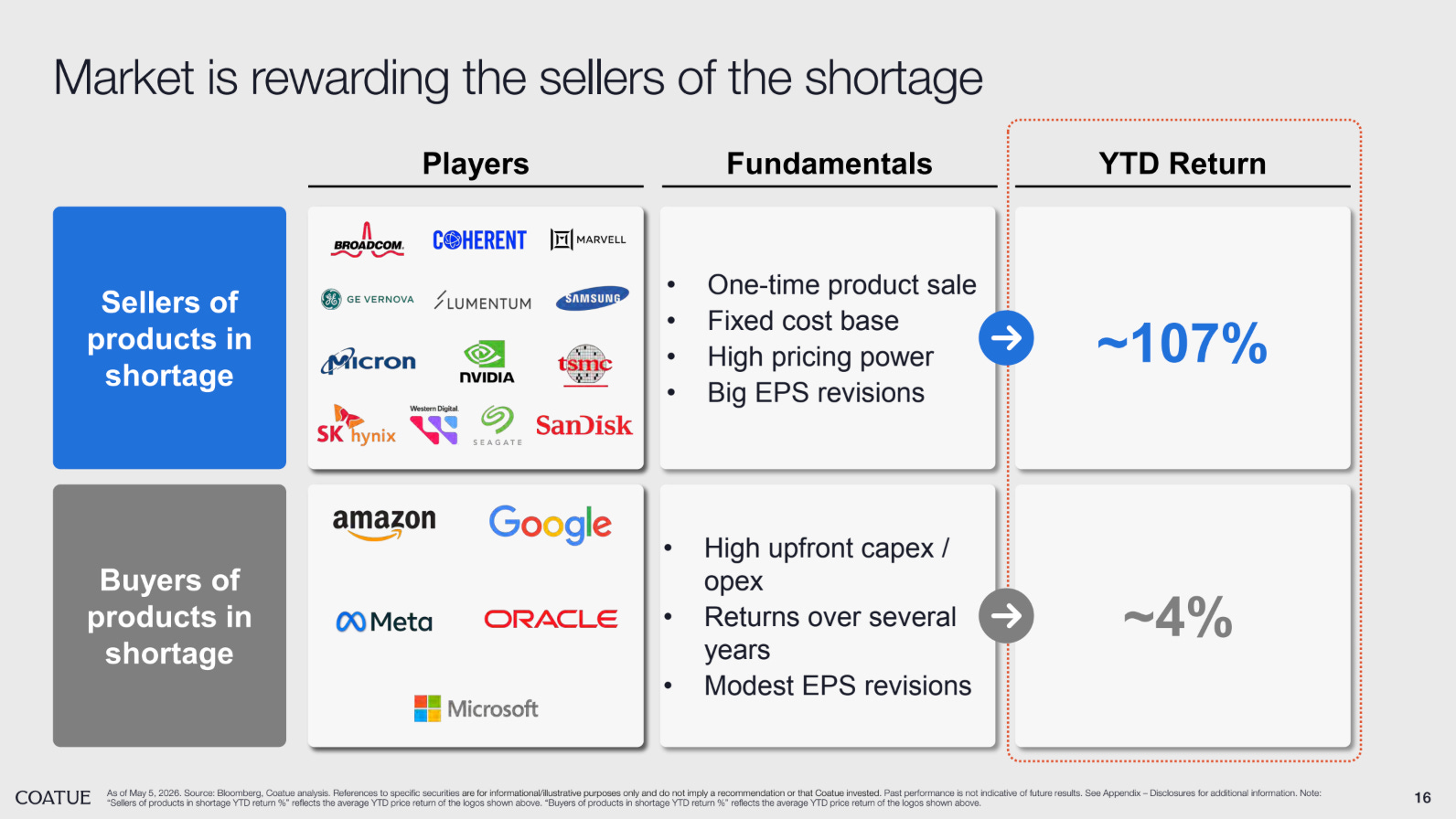

Sellers vs. Buyers of Shortage

The single most useful framework in Coatue’s deck is the distinction between sellers of shortage and buyers of shortage. The deck’s most evocative visual is a literal tug-of-war: two strongmen pulling on a rope labeled TOKENS, the SELLER side branded with Micron, SK Hynix, SanDisk, Lumentum, GE Vernova, and Intel; the BUYER side with Amazon, Meta, Microsoft, and Google.

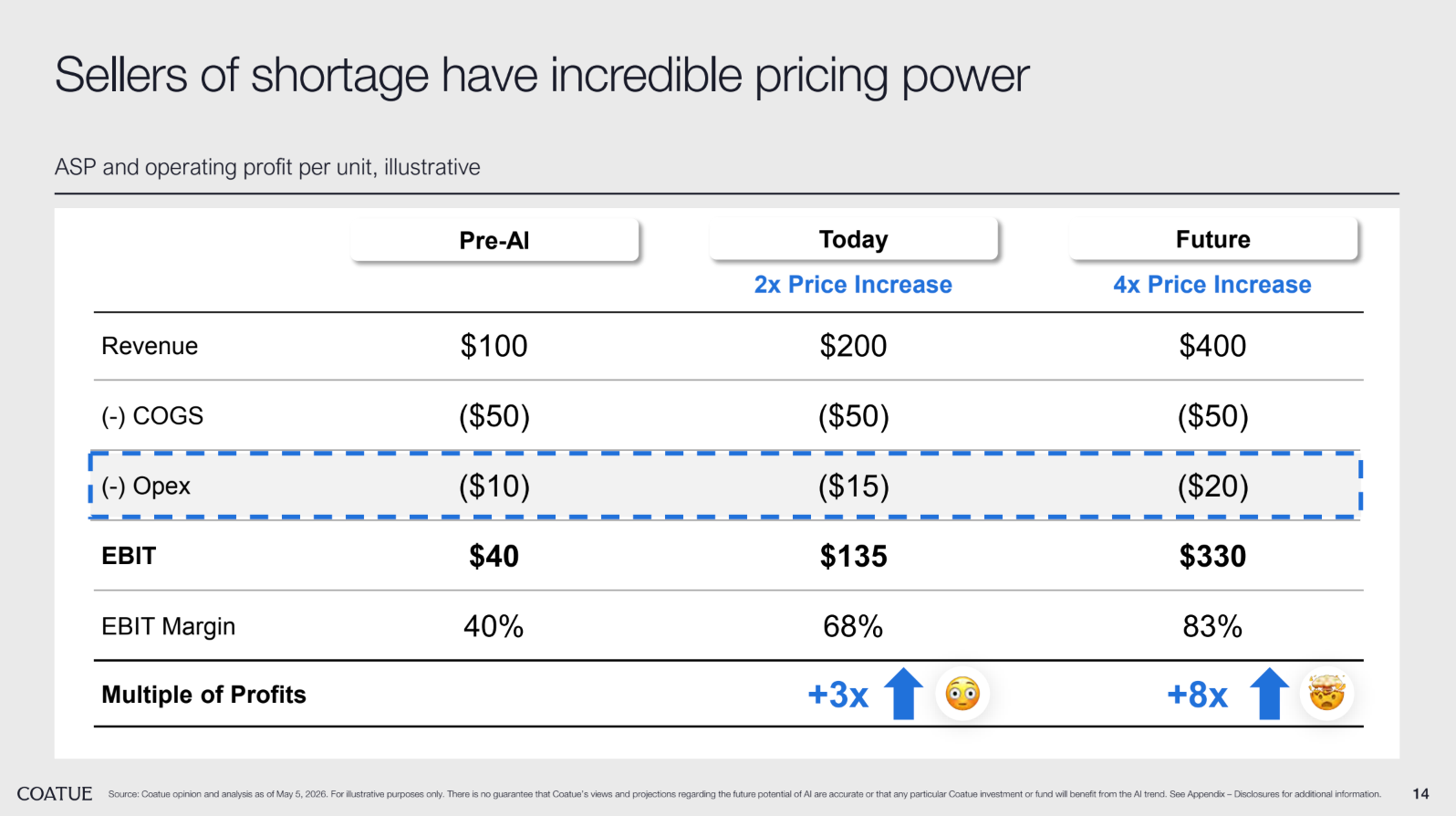

The economics behind the framework are extreme. Coatue’s illustrative unit economics (slide 14): a Pre-AI seller of shortage earns $40 of EBIT on $100 of revenue at a 40% margin. With a 2x price increase and only modest opex creep, today the same unit generates $135 of EBIT at a 68% margin, a 3x jump in profits. With a 4x price increase, the future case delivers $330 of EBIT at an 83% margin, an 8x jump.

“When price is the main lever of your revenue growth and you have fixed costs, your operating profit actually go up multiples of what your price increases or your revenue’s growing at.”

Real-world data (slide 15) confirms it: Micron’s operating margin has gone from a 16% five-year average to 69% today (+4x), and Seagate’s from 17% to 38% (+2x).

The market is rewarding the sellers and punishing the buyers.

According to slide 16, year to date, sellers of shortage (Broadcom, Coherent, Marvell, GE Vernova, Lumentum, Samsung, Micron, NVIDIA, TSMC, SK Hynix, Western Digital, Seagate, SanDisk) have returned ~107% on average.

Buyers (Amazon, Google, Meta, Oracle, Microsoft) have returned just ~4%. The cash-flow plumbing tells the same story.

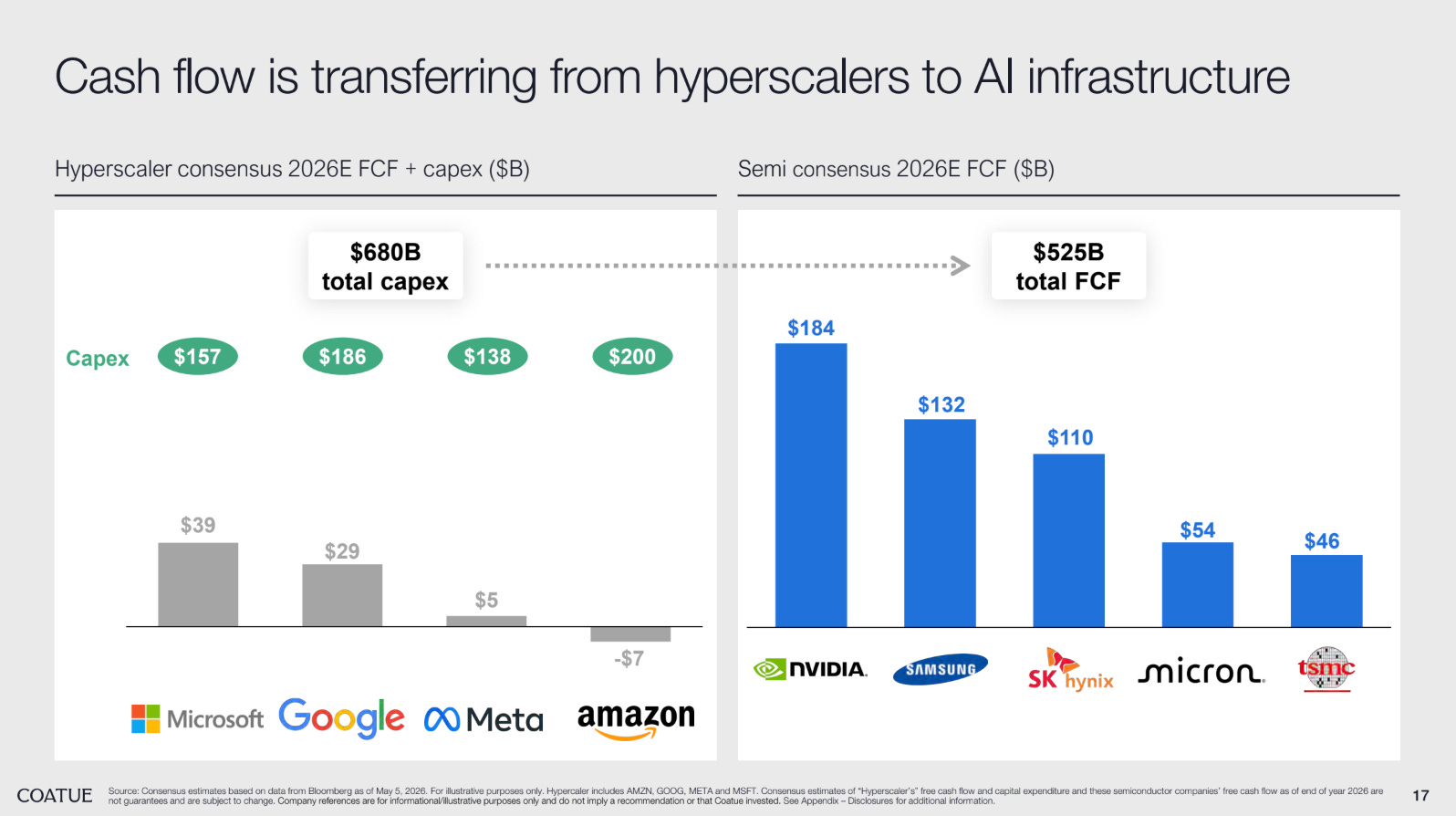

Meanwhile, the four hyperscalers will spend a combined $680B in capex on 2026E consensus (Microsoft $157B, Google $186B, Meta $138B, Amazon $200B) against just $66B of total free cash flow ($39B, $29B, $5B, –$7B).

On the semi side? The cohort generates $525B of FCF combined: NVIDIA $184B, Samsung $132B, SK Hynix $110B, Micron $54B, TSMC $46B. Cash flow, in Coatue’s words, is “transferring from hyperscalers to AI infrastructure.”

The multiple compression on buyers is the second-order effect, shown on slide 18. Since January 2025, Meta’s forward P/E has dropped from 23x to 17x (–6x), Amazon’s from 31x to 26x (–5x), and Microsoft’s from 30x to 22x (–8x). “If memory pricing goes up 100% and Microsoft has to spend two units instead of one, they’re not actually getting two units of benefit.” Two names sit in a unique middle position: “I actually think Amazon and Google are in an un-unusual camp, and those are the two companies that we really like because they are also a bit of a hybrid in that Google has TPUs that they sell, and Amazon has talked about selling Trainium.” By owning silicon as well as deploying it, they capture some of the shortage premium themselves.

Risks, Volatility, & What Comes Next

For all the bullishness, Jaimin is a risk manager first. The biggest risk he watches is another DeepSeek moment, a breakthrough that materially reduces the power, compute, or memory required to produce the same intelligence. In the short run, such a moment compresses the sellers of shortage. In the long run, it likely accelerates adoption and expands the pie.

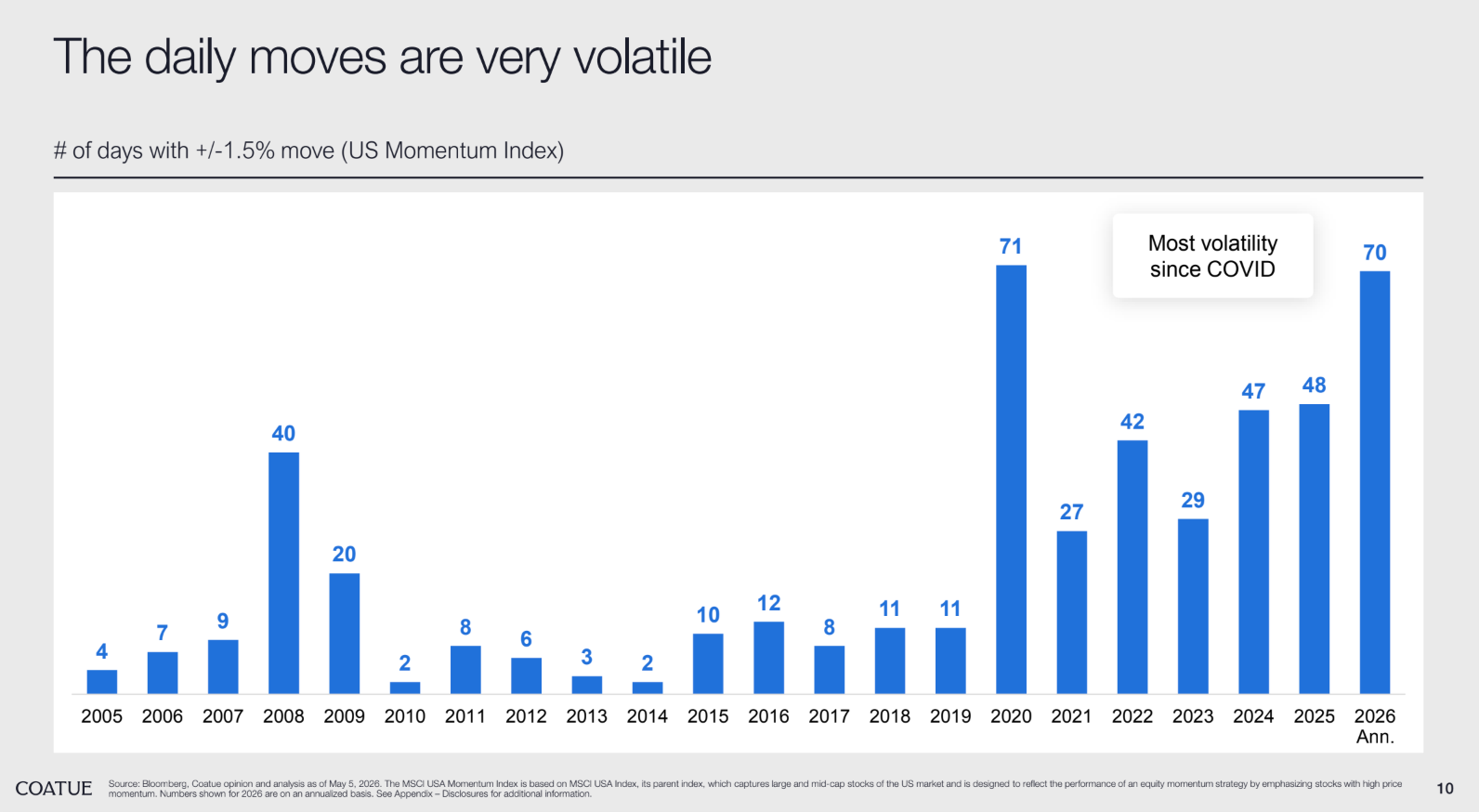

The other defining feature of this cycle is volatility, and Coatue’s data quantifies it. Slide 10 shows the MSCI USA Momentum Index has logged 70 days year to date (annualized) with moves of +/– 1.5% or more, the most since COVID. That compares to 71 in 2020, 47 to 48 in 2024 to 2025, 42 in 2022, and just 2 to 12 in most years between 2010 and 2019. Coatue’s annotation: “Most volatility since COVID.” Jaimin describes the qualitative experience: “The volatility we’re facing now is, wow, I’m still really bullish. AI is still doing great things, but wow, some days, some of our stocks are just down 5% or 10% on for no reason.” The discipline in those moments is to re-ground in fundamentals, and to use hedges, puts, and shorts where appropriate.

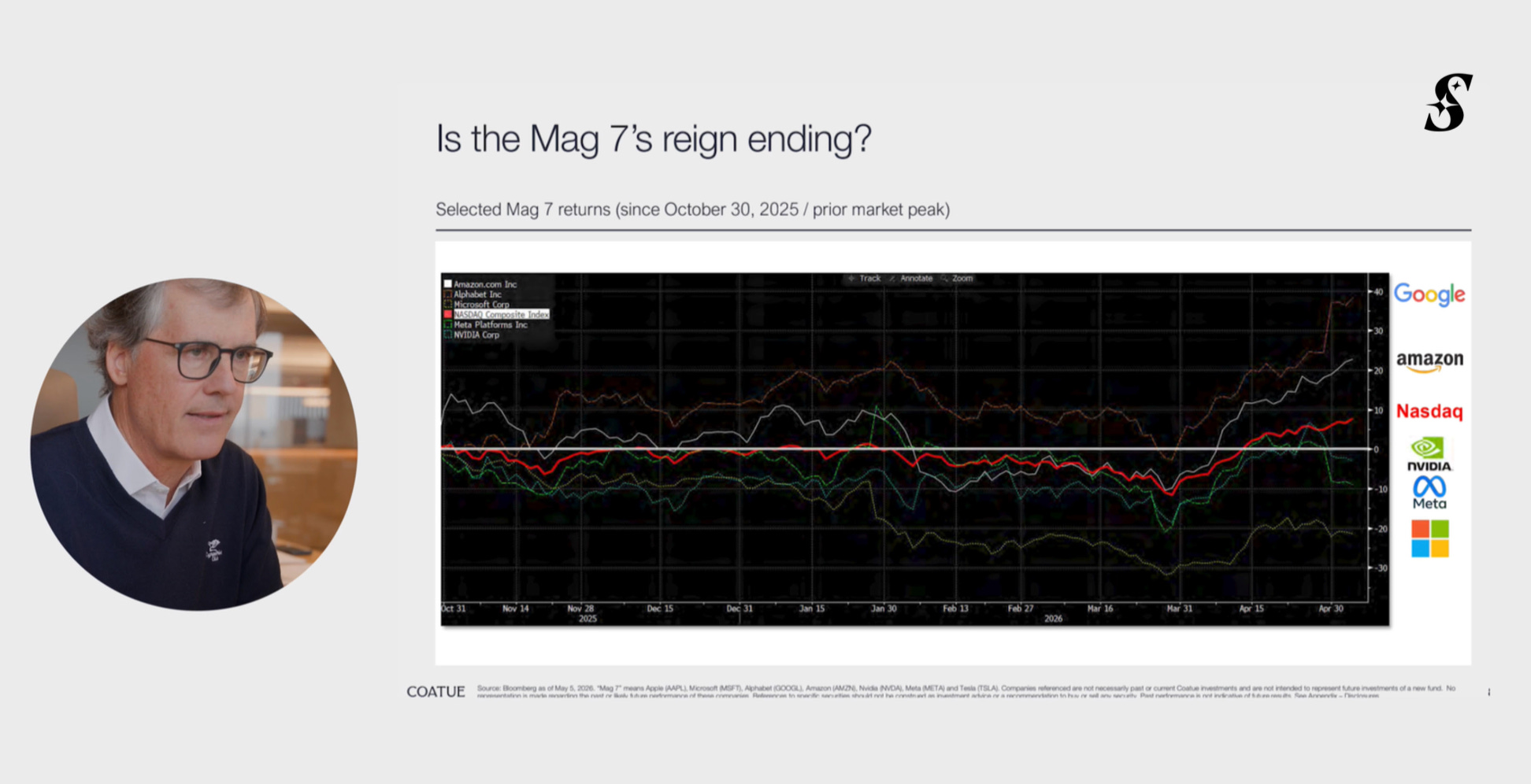

Even the Mag 7 is being reordered. Coatue’s chart (slide 8) of selected Mag 7 returns since the October 30, 2025 prior market peak shows extreme dispersion: Google has broken out to roughly +40%, Amazon is up around +20%, the NASDAQ Composite is up modestly, and the rest of the Mag 7 sits flat to down, with one name down more than 20%. As Philippe Laffont said on the call, “even within the Mag 7, the reordering of the pecking order is happening quickly.”

The underlying fundamentals remain strong. S&P 500 earnings growth is tracking at ~15% accelerating to 18% through 2026. The market is up roughly 7 to 8% year to date against 16% earnings growth, meaning multiples are actually compressing as prices rise. “At the end of the day, like, fundamentals do matter more so than sentiment, and I think the fundamentals are really strong.”

Asked what he’s most looking forward to, Jaimin returned to the firm itself. He joined Coatue in 2007 when it managed $700 million with twelve people; today it manages ~$80 billion with 200 people.

“I feel like we’re, as an organization, are at our second inflection. Maybe, probably not second, like fifth inflection. But we’re at another inflection where I think we’re really on this journey to, to really just break out.”

In a market where the rate of change is the only thing that matters, that mindset, what is changing, and how do I catch it?, may be Coatue’s most durable edge.

→ Listen on X, Spotify, YouTube, Apple

The material presented on Molly O’Shea’s website are my opinions only and are provided for informational purposes and should not be construed as investment advice. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular security, strategy, or investment product. Any analysis or discussion of investments, sectors or the market generally are based on current information, including from public sources, that I consider reliable, but I do not represent that any research or the information provided is accurate or complete, and it should not be relied on as such. My views and opinions expressed in any website content are current at the time of publication and are subject to change. Past performance is not indicative of future results.

Paid Endorsement. Brokerage services by Open to the Public Investing Inc, member FINRA & SIPC. Advisory services by Public Advisors LLC, SEC-registered adviser. Crypto trading provided by Zero Hash LLC, licensed by the NYSDFS. Generated Assets is an interactive analysis tool by Public Advisors. Output is for informational purposes only and is not an investment recommendation or advice. See disclosures at public.com/disclosures/ga. Matched funds must remain in your account for at least 5 years. Match rate and other terms are subject to change at any time.