ICYMI: MIT AI Report

Elon, Crusoe, Stripe, Figure Markets, Ashlee Vance

Brought to you by Brex

Brex is the intelligent finance platform: cards, expenses, travel, bill pay, banking—wrapped into a high-performance stack. Built for scale. Trusted by teams that move fast.

Spend smarter. Move faster. Sourcery subscribers get: 75,000 points after spending $3,000 on Brex card(s). Plus, white-glove onboarding, $5,000 in AWS credits, $2,500 in OpenAI credits, and access to $180k+ in SaaS discounts. On top of $500 toward Brex travel, $300 in cashback, plus exclusive perks (like billboards..) visit → brex.com/sourcery

Hello from SF

I had the pleasure of visiting Ashlee Vance, the ruler of the Core Memory empire, and of course, the “Elon Musk of writing about Elon Musk.” Stay tuned for a fun collab.. If you haven’t listened yet, check out his recent interview with Bryan Johnson. Probably the best interview of Bryan to date.

Ok. Now, don’t hold your breath, this next section is a little long.

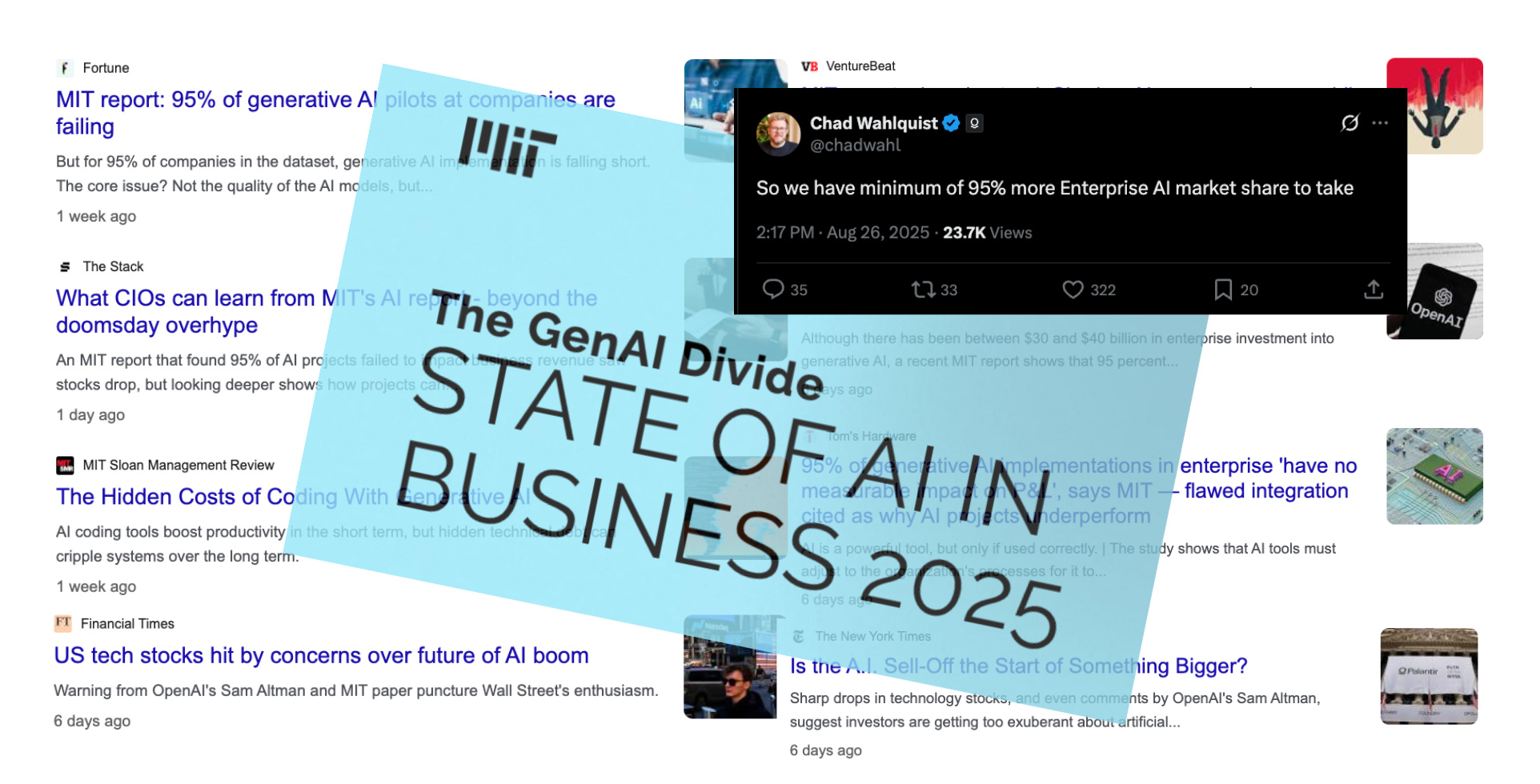

MIT AI Report

This shockinggg report, which ripped through wall st, silicon valley, & even, the All-In podcast, finds that despite $30–40B in enterprise investment, 95% of organizations see no real ROI from GenAI. Coining the “GenAI Divide”: a split where only ~5% of enterprises extract measurable value (millions in savings or revenue), while most remain stuck in pilots.

Stats:

Adoption vs. Transformation: Over 80% of organizations have piloted ChatGPT/Copilot, with ~40% deploying them. Yet these mainly improve individual productivity, not enterprise P&L.

Enterprise Tools Stall: 60% of firms evaluated enterprise-grade/custom systems, but just 5% reached production. The barrier is not model quality or regulation but lack of learning, memory, & workflow integration.

Industry Impact: Only Tech and Media show structural disruption. Sectors like healthcare, finance, energy, and manufacturing remain largely unchanged.

Shadow AI Economy: Employees are using consumer tools personally (90% of surveyed workers), far outpacing official enterprise adoption (40% of firms paid for enterprise licenses). This “shadow AI” delivers more practical ROI than corporate pilots.

Budget Misallocation: ~50–70% of AI budgets go to sales & marketing (outbound emails, lead scoring, personalization), while back-office functions (finance, procurement, ops) where ROI is actually higher, are underfunded.

What Works: Organizations that cross the divide rely on external vendor partnerships, bottom-up adoption by line managers, & tools that learn, retain context, and integrate deeply into workflows. Internal builds fail at 2x the rate of partnerships.

ROI Examples: Front-office gains (10% better retention, 40% faster lead qualification) are overshadowed by back-office wins: $2–10M saved annually by cutting BPOs, 30% reduction in agency spend, & major efficiency in finance/procurement.

The Counter: ‘AI Native’ Apps’ $18.5 Billion Annualized Revenues Rebut MIT’s Skeptical Study | The Information

ChatGPT Moment → Chaos Markets

After the launch of ChatGPT in late 2022, the tech industry entered fight-or-flight. SaaS was suddenly declared “dead,” layoffs swept through the sector, and by early 2023, companies were rushing to craft AI strategies. Few had a clear product-market fit, but they needed to prove to investors, employees, customers, & even themselves, that they wouldn’t miss out on what could be the most consequential shift in value creation since mobile or cloud.

This urgency led to AI “task forces,” board briefings, and high-profile pledges to integrate generative AI across business lines. But beneath the headlines, most enterprise efforts stalled. Many became pilots that never scaled, flashy partnerships to drive momentum, or surface-level integrations designed more for public market signaling than for true transformation.

FWIW I think this might’ve been one of the first times in history that the general public has had direct, low barrier access to the same advanced tools as corporations (ChatGPT, Copilot, Claude, Midjourney). Adoption has been widespread, progress has been visible, and it’s been nearly impossible to hide progress.. we see through your fake demos.

Yes, the overall spending has been massive, & yes, this certainly comes with R&D-like experiments that can go nowhere. But the companies that acted quickly made the right call.. *cue* move fast, break things. We’re now seeing rapid progress on all fronts: startups scaling from $0 to $100M faster than ever, and even Palantir surpassing $1B in quarterly revenue. In a market moving this quickly, actively learning & market testing has been critical.. or else, you become Apple 😂.

And despite $1B job offers for AI researchers, one point is honestly not mentioned enough.. the need for teams to embrace & create new cultures around AI. Lean in, or move on. Coinbase CEO Brian Armstrong emphasizes this in his Cheeky Pint interview: engineers had one week to get up to speed with AI or be fired.

Look to the Bright Side?

Quick AI Lessons

Klarna's AI Automation Reversal

After laying off 700 employees in 2022 & partnering with OpenAI to automate their workforce, Klarna soon faced declining customer satisfaction as its AI-first experience didn’t meet expectations (though they did save $10M on marketing). By 2025, CEO Sebastian Siemiatkowski admitted that cost-cutting had come at the expense of quality & began rehiring humans, effectively reversing the fully-automated push, and allowing for more BNPL Chipotle burritos.

Similarly, IBM followed a similar arc, freezing hiring & cutting 8,000 roles in 2023 before recently announcing a roll-out of new hires. Not so fast, Watson.

Fully Integrated, AI-Native Strategy

“We recognized from the beginning that AI would be transformational to our business, so we built it directly into the foundation of our products and operations. Never layered it on top.

The biggest mistake we see today is companies treating AI as a quick fix or add-on. To truly compete and build durable infrastructure, AI has to be thoughtfully deployed, full-stack, and fully integrated. That is how you win.” Brex COO, Camilla Matias

Read More: How we're building AI-native operations at Brex

Questions

Are surveys even real?

How fast will Palantir capture the 95% upside?

Does this give enterprises pricing power / negotiation leverage?

Musings

Podcasts

VC

Is Venture Broken? What 2,000+ Priced Early-Stage Rounds Tell Us about the State of Seed & Series A | Beezer Clarkson, Sapphire

Top Interviews

How 8VC Builds Billion-Dollar Companies | Palantir, Addepar, Saronic

Raising a Trust Fund With Marc Andreessen & Paris Hilton | Sophia Amoruso

Vulcan Elements: How The Rarest Company On Earth Raised $75M from Altimeter

→ Follow Sourcery on: X, YouTube, Spotify, Apple, Linkedin

Last Week (8/18-8/22):

Relevant deals include the 70+ deals across stages below. I've categorized the deals below into seven categories, Fintech, Care, Enterprise / Consumer, HardTech, Sustainability, Acquisition/PE, and Fund Announcements, and ordered from later-stage rounds to early-stage rounds.

VC Deals

Fintech:

- Midas, an Istanbul, Turkey-based investment app, raised $80 million in Series B funding. QED Investors led the round and was joined by International Finance Corporation and QuantumLight.

- IVIX, a New York City-based AI-powered platform designed to help governments around the world combat financial crime at scale using LLMs, advanced graph analytics and publicly available data, raised $60 million in Series B funding. O.G. Venture Partners led the round and was joined by Insight Partners, Citi Ventures, Team8, Disruptive AI, Cardumen Capital, and Cerca.

- Medallion, an SF-based back-office management automation company, raised $43m. Acrew Capital led, joined by Washington Harbour Partners, Sequoia Capital, GV, Spark Capital, and NFDG.

- Paradigm, a San Francisco, Calif.-based developer of an agentic AI-powered spreadsheet, raised $5 million in seed funding from General Catalyst.

- Legion, a New York City-based crypto fundraising platform, raised $5 million in seed funding. VanEck and Brevan Howard Digital led the round and were joined by Kraken, Coinbase Ventures, GSR, Crypto.com Capital, cyber•Fund, Bitscale Capital, Blockchain Builders Fund, and Systemic.

Care:

- Twin Health, metabolic health startup, raises $53 million Series E at $950 million valuation

- Wellth, an LA-based digital health platform, raised $36m in Series C funding. Mercato Partners led, joined by FCA Venture Partners, Comcast Ventures, SignalFire, NY Life, and CD-Venture.

- Method AI, a Boston, Mass.-based developer of image-guided surgical navigation technology, raised $20 million in Series A funding. A private family officer led the round and was joined by Cleveland Clinic and JobsOhio Growth Capital Fund.

- Develop Health, a Menlo Park, Calif.-based benefits‑verification and prior‑authorization platform, raised $14.3 million in Series A funding. Wing Venture Capital led the round and was joined by Afore Capital, J Ventures, and South Park Commons.

- Convoke, a South San Francisco-based AI-powered operating system for drug development, raised $8.6 million in seed funding. Kleiner Perkins and Dimension Capital led the round and were joined by ACME, Comma Capital, Liquid2, Not Boring Capital, Audacious, Lux Capital, and angel investors.

- Cascala Health, a Boston, Mass.-based AI-powered clinical intelligence platform, raised $8.6 million in seed funding. Flare Capital Partners and Eniac Ventures led the round and were joined by others.

Enterprise/Consumer:

- Ontic, an Austin, Texas-based protective intelligence platform, raised $230m in Series C funding. KKR led, joined by JMI Equity, Silverton Partners, Ridge Ventures, and Ten Eleven Ventures.

- Seemplicity, a Tel Acic, Israel-based risk management & remediation platform, raised $50 million in Series B funding. Sienna Venture Capital led the round and was joined by Essentia Venture Capital and existing investors Glilot Capital Partners, NTTVC, and S Capital.

- TinyFish, a Palo Alto, Calif.-based web infrastructure company, raised $47 million in funding. INCONIQ led the round and was joined by USVP, Mango Capital, MongoDB Ventures, ASG, and Sandberg Bernthal Venture Partners.

- Kasa, a San Francisco-based operator of hotel and apartment hotel rentals, raised $40 million in funding. Silver Lake Waterman led the round.

- Zed, a Boulder, Colo.-based developer of an open-source code editor, raised $32 million in Series B funding. Sequoia Capital led the round.

- Pylon, a San Francisco-based AI-powered support platform for B2B companies, raised $31 million in Series B funding. Andreessen Horowitz and Bain Capital Ventures led the round.

- Loft Dynamics, a Santa Monica, Calif.-based developer of virtual reality flight training technology, raised $24 million in Series B funding. The Friedkin Group led the round and was joined by Alaska Airlines, Sky Dayton, Craft Ventures, and UP.Partners.

- Tote.ai, a San Francisco-based AI-powered point-of-sale system for fuel and convenience stores, raised $22.6 million in funding. Cota Capital led the round and was joined by Storm Ventures and Cervin Ventures.

- Bluefish AI, a New York City-based AI platform for brand marketing, raised $20 million in Series A funding. NEA led the round and was joined by Salesforce Ventures, Crane Venture Partners, Swift Ventures, and Bloomberg Beta.

- Phoebe, a London, U.K.-based developer of agentic AI software designed to diagnose issues in live data and prevent them, raised $17 million in seed funding. Google Ventures and Cherry Ventures led the round.

- Firecrawl, a San Francisco-based AI crawler, raised $14.5 million in Series A funding. Nexus Venture Partners led the round and was joined by Y Combinator and others.

- Definite, a Wilmington, Del.-based full-stack AI-native data platform, raised $10 million in seed funding. Costanoa led the round and was joined by Acrew Capital and angel investors.

- Convoke, a Cambridge, Mass.-based developer of an AI-powered operating system, raised $8.6 million in seed capital. Kleiner Perkins and Dimension Capital led the round and were joined by ACME, Comma Capital, Liquid2, Not Boring Capital, Audacious, and others.

- TensorZero, a New York City-based startup building open-source infrastructure for LLMs, raised $7.3 million in seed funding. FirstMark led the round and was joined by Bessemer, Bedrock, DRW, Coalition, and angel investors.

- Zipline AI, a San Mateo, Calif.-based AI infrastructure company, raised $7 million in seed funding. Wing VC led the round and was joined by Stripe, Box Group, and Exceptional Capital.

- Agenda Hero, a San Francisco-based developer of an AI-powered calendar program, raised $5.6 million in funding. Upfront Ventures led the round and was joined by Precursor Ventures and existing investor K9 Ventures

- Innerworks, a London, U.K.-based cybersecurity company, raised $4 million in seed funding. AlbionVC led the round and was joined by Digital Currency Group, Founders Capital, Firestreak Ventures, NVTBL Ventures, and Metaversal Ventures.

- July AI, a San Francisco-based company platform that provides new graduates and professionals with AI training, raised $1.04 million in pre-seed funding from Basis Set, Liquid 2 Ventures, Night Capital, SV Angel, and others.

HardTech:

- Quantinuum, a quantum computing group backed by Honeywell (Nasdaq: HON), is in talks to raise new funding at a $10b valuation

- FieldAI, an Irvine, California-based developer of "brains" for robots, raised $393 million in Series A and Series A-1 funding, at a $2 billion post-money valuation.

- Nuro, a Mountain View, Calif.-based self-driving technology company, raised $203 million in Series E funding from Uber, Baillie Gifford, Icehouse Ventures, Kindred Ventures, NVIDIA, and Pledge Ventures.

- Overhaul, an Austin, Texas-based supply chain risk and intelligence company, raised $105 million in Series C funding. Springcoast Partners led the round and was joined by Edison Partners.

- Aalo Atomics, an Austin, Texas-based builder of nuclear plants, raised $100 million in Series B funding. Valor Equity Partners led the round and was joined by Fine Structure Ventures, Hitachi Ventures, NRG Energy, Vamos Ventures, Tishman Speyer, Kindred Ventures, and others.

- Stark, a German weaponized drone maker, raised $62m at a $500m valuation. Sequoia Capital led, joined by 8VC, Thiel Capital, NATO Innovation Fund, In-Q-Tel, Project A, and Döpfner Capital.

- Keychain, a New York City-based developer of an AI-powered manufacturing platform for the consumer packaged goods industry, raised $30 million in Series B funding. Wellington Management and BoxGroup led the round and were joined by existing investors.

- SpinLaunch, a Long Beach, Calif.-based developer of a low-orbit broadband constellation, raised $30m. ATW Partners led, joined by Kongsberg Defence and Aerospace

- Garage, a New York City-based online emergency vehicle and surplus equipment marketplace, raised $13.5 million in Series A funding. Infinity Ventures led the round and was joined by Y Combinator, Initialized Capital, Benchstrength, Wayfinder Ventures, and FJ Labs.

Acquisitions & PE:

- MCR Group has agreed to help take Soho House (NYSE: SHCO) private for $2.7 billion, or $9 per share.

- Crusoe, a Denver-based modular data center company that's raising new funds at a $10b valuation, paid $150m in cash and stock to acquire Atero, an Israeli provider of GPU management and memory optimization for AI workloads.

- Thoma Bravo has agreed to buy Dayforce (NYSE: DAY), a Minneapolis-based HR software provider, for $12.3 billion.

IPOs:

- Figure, a consumer lending platform led by Mike Cagney (ex-SoFi), filed for an IPO that Renaissance Capital estimates could raise $400m. It reports $29m of net income on $191m in revenue for the first half of 2025, and plans to list on the Nasdaq (FIGR). Figure has raised around $425m, most recently in 2021 at a $3.2b valuation, from backers like DST Global, Ribbit Capital, DCM, and Norgan Creek Digital.

Love merch? Check out our shop: sourcerymerch.com

The material presented on Molly O’Shea’s website are my opinions only and are provided for informational purposes and should not be construed as investment advice. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular security, strategy, or investment product. Any analysis or discussion of investments, sectors or the market generally are based on current information, including from public sources, that I consider reliable, but I do not represent that any research or the information provided is accurate or complete, and it should not be relied on as such. My views and opinions expressed in any website content are current at the time of publication and are subject to change. Past performance is not indicative of future results.