Sourcery 🌳 Adobe≠Figma, Prague, a16z American Dynamism

(12/11-12/15) Armada, SumUp, Hyperplane, Comun, Twin Health, PursueCare, Inductive Bio, Essential AI, Contact Monkey

Happy Holidays!

We’re just getting back from a week in Prague for the 2023 Postgres Conference EU. And while we sadly missed many holiday parties in the States, we made it up by visiting every single Christmas market in the charming cobblestoned historic city (in the brief 30min period outside of the conference hall).

For those unfamiliar, Postgres (aka PostgreSQL) is one of the most popular & extensible databases used by pretty much every organization out there. More specifically, it is an open-source relational database management system (RDBMS) with over 36 years of active development. Turns out, you can kind of do everything with Postgres and some even prefer it as their one-stop shop for data management by utilizing its abilities to create user-defined data types, functions, and procedures.

For example, Postgres has ‘extensions’ which are add-on modules that enhance the functionality of the databases: PostGIS for geospatial data (AD), pgmq for message queues (chatbots?), or more popular as of late, pgvector for vector similarity search (AI/LLM), etc. ‘Foreign Data Wrappers’ (FDW) are also powerful options to interact with external data sources, offering a unified view of data: i.e. clerk_fdw—a tool that bridges the gap between Clerk, a leading user management solution & your own Postgres Database. Lastly, custom operators and index types can also be defined to optimize queries based on specific data characteristics.

With more data, more tools, and more chaotic environments (aka AI/LLM revolution), DBAs (database administrators) and developers are increasingly turning to maxing out their Postgres databases to reduce the sprawl. Curious to learn more? Check out one of my favorite blogs on “collapsing the modern data stack” with Postgres.

This week is the final week before many take-off & shut down for the holidays (& my favorite: time becomes an illusion). The deals section isn’t the most active, but it is pretty rich across Fintech, AI, and HardTech. Musings are super full as headlines stay strong, and AI & HardTech continue to lead interesting conversations & innovations. Lastly, at the very bottom, check out the 2023 public markets’ rollercoaster (maybe Riccardo, the bull at Newark station really is a sign?), plus a solid overview of Moonshots and winners in Space launch.

Musings

Macro

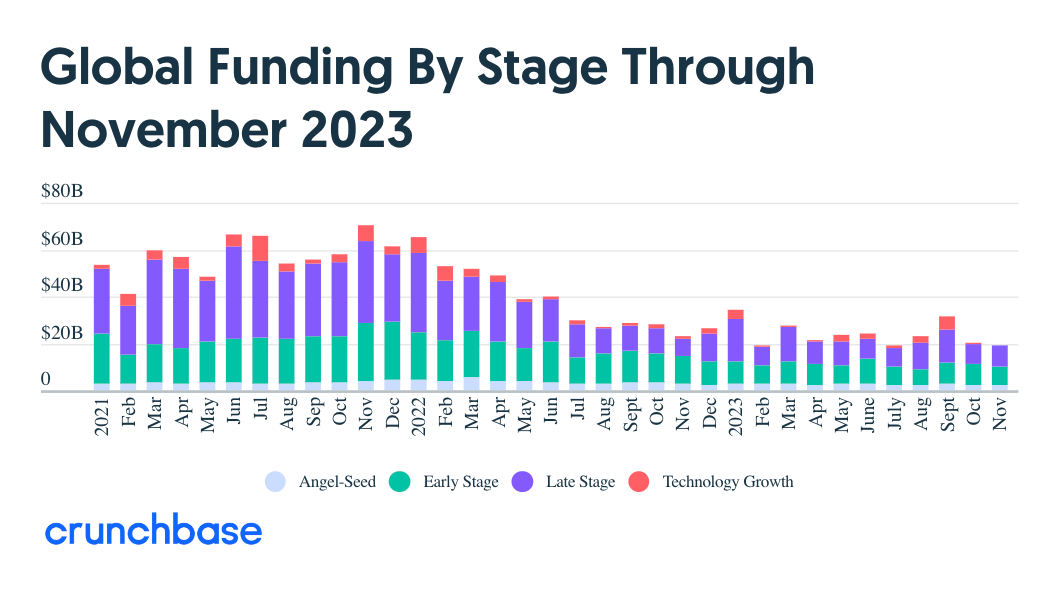

Global Venture Funding In November Slows At Early Stage, TechCrunch

Global venture funding reached $19.2 billion in November 2023, down marginally month over month, Crunchbase data shows. Funding fell around 16% from the $23 billion invested in November 2022, which was already down by two-thirds from November 2021.

Step-Ups & Duration: The Shape of Things to Come to the Series A in 2024, Tomasz Tunguz

The typical software startup raised their Series A 15 months after raising their seed at 2x their seed valuation. A year ago, that Series A would have been raised three months earlier at 3.5x the valuation.

8 Charts That Explain 2023, The Information

Chatbots reigned. IPOs & startups (outside of AI) struggled. Bitcoin soared, despite bankruptcies and guilty pleas. Creator economy winners.

The Death of the Creator Economy, Contrary Research

Narrative violation: The ‘All-In’ Hosts Make the Leap from Investors to Influencers, The Information

AI & Data

Gavin Uberti - Real-Time AI & The Future of AI Hardware, Invest Like the Best

Gavin Uberti is the Chief Executive Officer at Etched.ai. We cover the hardware building blocks of AI models, how model-specific chips differ from traditional GPUs, and the need to build dedicated physical infrastructure to support the transformer revolution.

Confluent’s Resilient Rise To Software Behemoth, Logan Bartlett Podcast

Jay Kreps (CEO, Confluent) only went to one year of high school because he thought school was an inefficient way of learning. Since then, he’s continued to carve his unique path. Jay shares Confluent’s resilient journey from LinkedIn spin-out to public company, including details from turning an open source project into a commercial success, competing with AWS in the cloud industry, and his learnings from diving into a CEO role.

Five Predictions for AI in 2024, Vivek Ramaswami & Sabrina Wu

How AI Will Transform Legacy Industries, The Bull Case for Vertical SaaS, and the Future of the Series A Market (Jules Schwerin), The Full Ratchet

Jules Schwerin is a Partner at RTP Global, an early-stage firm headquartered in New York that has backed the likes of DataDog, Delivery Hero, and DataRobot.

HardTech

David Ulevitch, GP at Andreessen Horowitz, America Builds Podcast

David Ulevitch is an entrepreneur and investor. As a General Partner at Andreessen Horowitz, he leads the firm’s American Dynamism practice, which focuses on investing in companies advancing American interests such as defense, aerospace, public safety, education, housing, supply chain, industrials, and manufacturing.

Why Every Company Will Be an Energy Company, Meera Clark

Looking ahead to 2024, we're excited about software's potential to reshape the $600Bn commercial energy industry as businesses shift from analog to algorithmic approaches.

The Future of Aviation, A deep dive into the mysteries and future of flight, Anna-Sofia Lesiv

Although challenges remain before supersonic travel returns, innovations in military aircraft may portend the end to the long stall in progress in commercial flight.

Other

The 3 "Macronutrients" You Need For Lifelong Happiness, Arthur Brooks, Ph.D., mbg

. . .

Last Week (12/11-12/15):

Relevant deals include the 60+ deals across stages below.

I've categorized the deals below into five categories, FinTech, Care, Enterprise & Consumer, HardTech, and Sustainability, and ordered from later-stage rounds to early-stage rounds. Highlighted deals include Armada, SumUp, Hyperplane, Comun, Twin Health, PursueCare, Inductive Bio, Essential AI, Contact Monkey, Durable, Allstar.gg, Distributional, Chalk, Delphina, Arcane, True Anomaly, Qogita, Tacto, Super, CurbWaste, Prevu; Docker/AtomicJar, ConcertAI/CancerLinQ

Final numbers on Bull Market? and Moonshots: Virgin Gallatic & Launch Winners at the bottom.

Deals

Fintech:

- SumUp, a London, U.K.-based financial services company, raised €285 million ($306.5 million) in funding. Sixth Street Growth led the round and was joined by Bain Capital Tech Opportunities, Fin Capital, and Liquidity Group.

- Dynamic Labs, a Palo Alto, Calif.-based developer of a web3 login tool, raised $13.5 million in Series A funding. a16z crypto led the round and was joined by Founders Fund, Castle Island Ventures, and others.

- Lolli, a New York City-based bitcoin and cashback rewards company, raised $8 million in Series B funding. BITKRAFT Ventures led the round and was joined by Sfermion, Prisma Ventures, Hypersphere Ventures, and others.

- Hyperplane, a Palo Alto, Calif.-based data intelligence platform for financial institutions, raised $6 million in seed funding. Lachy Groom led the round and was joined by SV Angel, Clocktower Technology Ventures, Liquid2 Ventures, and others.

- Comun, a New York City-based banking app designed for Latino families, raised $4.5 million in funding. Costanoa Ventures led the round and was joined by existing investors Animo Ventures, South Park Commons, and others.

- Stairs Financial, a remote-based mortgage marketplace, raised $3.5 million in seed funding. Zigg Capital led the round and was joined by Y Combinator, Antler, and others.

- Binkey, a Washington, D.C.-based fintech helping businesses accept FSA and HSA payments, raised $3.3m in seed funding, per Axios Pro. Wellington Management led, and was joined by Springtide Ventures, Plug and Play Ventures and Third Culture Capital. https://axios.link/48hYD6s

- SupportPay, a Charlotte, N.C.-based child support management and payment platform for co-parents, raised $3.1 million. HearstLabs led the round and was joined by Michigan Capital Network, Victorium Capital, Rendar Capital, and others.

. . .

Care:

- Twin Health, a Mountain View, Calif.-based metabolic care startup, raised $50m in Series C funding, as first reported by Axios Pro. Temasek led, and was joined by insiders Iconiq Growth, Sofina, Peak XV, and Helena. https://axios.link/3toQNJf

- PursueCare, a Middletown, Conn.-based virtual addiction treatment provider, raised $20m in Series B funding. T.rx Capital and Yamaha Motor Ventures co-led, and were joined by Seyen Capital and OCA Ventures. It also acquired digital therapeutic assets from bankrupt Pear Therapeutics. https://axios.link/3RET64d

- Medefy, a Tulsa, Oklahoma-based platform designed to help employees navigate their health benefits, raised $10 million in Series A funding. Mercury Fund led the round and was joined by Advantage Capital.

- Inductive Bio, a New York City-based company developing a machine learning platform to be used in drug discovery, raised $4.3 million in seed funding. a16z Bio + Health and Lux Capital led the round and were joined by Character, Bessemer Venture Partners, Alleycorp, and others.

- Certainly Health, a New York City-based healthcare marketplace for booking medical and cosmetic care with upfront prices, raised $2.3 million in funding from Pacific 8 Ventures, Y-Combinator, and others.

. . .

Enterprise & Consumer:

- Essential AI, a San Francisco-based company developing AI products designed to improve human productivity, raised $56.5 million in Series A funding. March Capital led the round and was joined by AMD, Franklin Venture Partners, Google, and others.

- ContactMonkey, a Toronto, Ontario-based internal email communications platform, raised $55 million in Series A funding from Updata Partners.

- Guardz, a Tel Aviv, Israel-based provider of cybersecurity for small businesses, raised $18 million in Series A funding. Glilot+ led the round and was joined by Hanaco Ventures, iAngels, and others.

- Origin AI, a Rockville, Maryland-based developer of technology designed to turn WiFi signals into precise presence sensing solutions for security, eldercare, and other uses, raised $15.9 million in a Series B extension. Verisure led the round and was joined by Okinawa Electric Power Company and others.

- Durable, a Vancouver, B.C.-based AI-powered website builder and small business platform, raised $14 million in Series A funding. Spark Capital led the round and was joined by existing investors Torch Capital, Altman Capital, Dash Fund, and others.

- Allstar.gg, a New York City-based platform that automatically creates shareable gaming videos from longform gameplay, raised $12 million in Series A funding. Drive Capital led the round and was joined by Mark Cuban, Studio VC, J-Ventures, and others.

- Distributional, an enterprise platform for AI testing, raised $11m in seed funding. Andreessen Horowitz led, and was joined by Operator Stack, Point72 Ventures, SV Angel, and Two Sigma. https://axios.link/3RKoqii

- Chalk, a San Francisco-based data platform for machine learning, raised $10 million in seed funding. General Catalyst led the round and was joined by Unusual Ventures, Xfund, and angel investors.

- Delphina, a San Francisco-based AI copilot for data science, raised $7.5 million in seed funding. Costanoa Ventures and Radical Ventures led the round and were joined by angel investors.

- Featureform, a San Francisco, Calif.-based MLOps feature store for building AI and ML systems, raised $5.5 million in seed funding. GreatPoint Ventures and Zetta Venture Partners led the round and were joined by Tuesday Capital and Alumni Ventures.

- Datalogz, a New York City-based business intelligence platform designed to reduce business intelligence and analytics sprawl, raised $5 million in funding. GreatPoint Ventures led the round and was joined by Graphene Ventures, Squadra Ventures, Berkeley Skydeck, and others.

- Arcane, a London, U.K.-based AI copilot for digital marketers, raised $5 million in seed funding. Accel led the round and was joined by others.

- Magma, an Austin, Texas-based collaborative art creation and project management platform, raised $5 million in seed funding. GFR Fund led the round and was joined by 4founders, Supernode Global, and others.

- Seam, a Brooklyn, N.Y.-based platform designed to allow users to code, design, and curate their own social spaces, raised $2.5 million in seed funding. 1kx led the round and was joined by Seed Club Ventures, Sfermion, F7 Ventures, Social Graph Ventures, and angel investors.

. . .

HardTech:

- True Anomaly, a Centennial, Colo.-based developer of space security, sustainability, and accessibility technology, raised $100 million in Series B funding. Riot Ventures led the round and was joined by Eclipse, ACME Capital, Menlo Ventures, and others.

- Qogita, a London, U.K. and Amsterdam, Netherlands-based procurement platform for wholesale products, raised €80 million ($87.7 million) in Series B funding. Dawn Capital led the round and was joined by Accel and others.

- Armada, a San Francisco-based company designed to enable companies to use generative AI and predictive models from anywhere on the planet, raised $55 million in funding. Founders Fund, Lux Capital, Shield Capital, and 8090 Industries led the round and were joined by Felicis, Contrary, and others. Shoutout to Xander Oltmann of Commodity Capital for getting in at the Seed (“yuge deal”)!

- Tacto, a Munich, Germany-based operating system for supply chains, raised €50 million ($54 million) in funding. Sequoia Capital and Index Ventures led the round and were joined by Visionaries Club, Cherry Ventures, and UVC Partners.

- Zuper, a Seattle, Wash.-based solutions provider to field operations businesses, raised $32 million in Series B funding. FUSE led the round and was joined by Prime Ventures and others.

- CurbWaste, a New York City-based provider of software for waste services management, raised $10 million in Series A funding round. Flourish Ventures led the round and were joined by TTV Capital, Mucker Capital, and B Capital.

- Prevu, a New York-based online real estate platform, raised $6m in Series A funding from Citi, Alpaca Ventures, Winklevoss Capital, RiverPark Ventures, Metropolis Ventures, Simplex Ventures, Liebenthal Ventures, Alpaca VC, TYH Ventures, and Blue Ivy Ventures. https://axios.link/3GLjmDX

Acquisitions & PE:

- Docker, the software container platform most recently valued by VCs at $2.1b, acquired AtomicJar, a Newark, N.J.-based open source testing startup that earlier this year raised $25m in Series A funding from Insight Partners, Boldstart Ventures, Tribe Capital, and Chalfen Ventures. https://axios.link/3wDOrEr

- ConcertAI, a Cambridge, Mass.-based med research tool valued by VCs at nearly $2b, acquired CancerLinQ, a provider of oncology data and quality of care solutions, from the American Society of Clinical Oncology. www.concertai.com

- Hibu, backed by H.I.G. Capital, acquired the software division of Signpost, a New York City-based provider of live receptionist services. Financial terms were not disclosed.

- Ncontracts, a portfolio company of Gryphon Investors, acquired Quantivate, a Bothell, Wash.-based provider of governance, risk, and compliance solutions for banks and credit unions. Financial terms were not disclosed.

- Nintex, backed by TPG Capital, agreed to acquire Skuid, a Chattanooga, Tenn.-based low-code platform for developing apps. Financial terms were not disclosed.

- Hubbell Incorporated acquired Systems Control, an Iron Mountain, Mich.-based manufacturer of substation control and relay panels for the electric transmission and distribution industry, from Comvest Partners. Financial terms were not disclosed.

- Nokia agreed to acquire Fenix Group, a Chantilly, Va.-based provider of tactical communications products for military applications, from Enlightenment Capital. Financial terms were not disclosed.

- Bain Capital acquired Guidehouse, a McLean, Va.-based provider of consulting and managed services, from Veritas Capital for $5.3 billion.

- Thoma Bravo acquired a majority stake in BlueMatrix, a Durham, N.C.-based content creation and distribution platform for investment research providers. Financial terms were not disclosed.

Funds:

- Oaktree Capital Management, a Los Angeles, Calif.-based asset management firm, raised approximately $3 billion for its third fund focused on companies facing temporary challenges.

- Apax Partners, a New York City-based private equity, raised $900 million for a fund focused on companies tackling environmental or social issues.

- BoxGroup, a New York City and San Francisco-based venture capital fund, raised $425 million across two funds.

- Playground Global, a Palo Alto, Calif.-based venture capital firm, raised $410 million for its second fund focused on deep tech companies.

- Harpoon Ventures, a San Diego, Calif.-based Harpoon Ventures, $125 million for its third fund for startups in AI, deep tech, cybersecurity, enterprise infrastructure, and other industries.

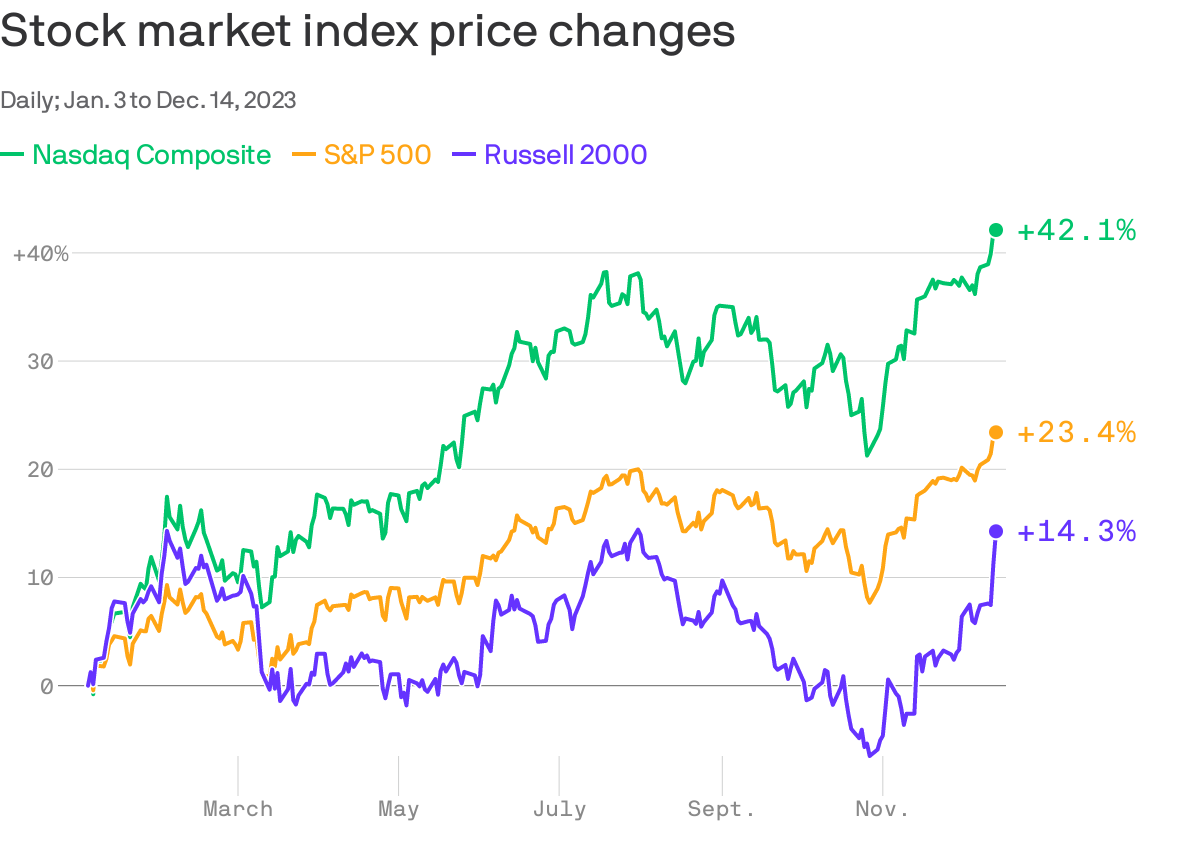

Final Numbers: 🐂🐂🐂 Market?

Data: Yahoo Finance; Chart: Axios Visuals

Moonshots

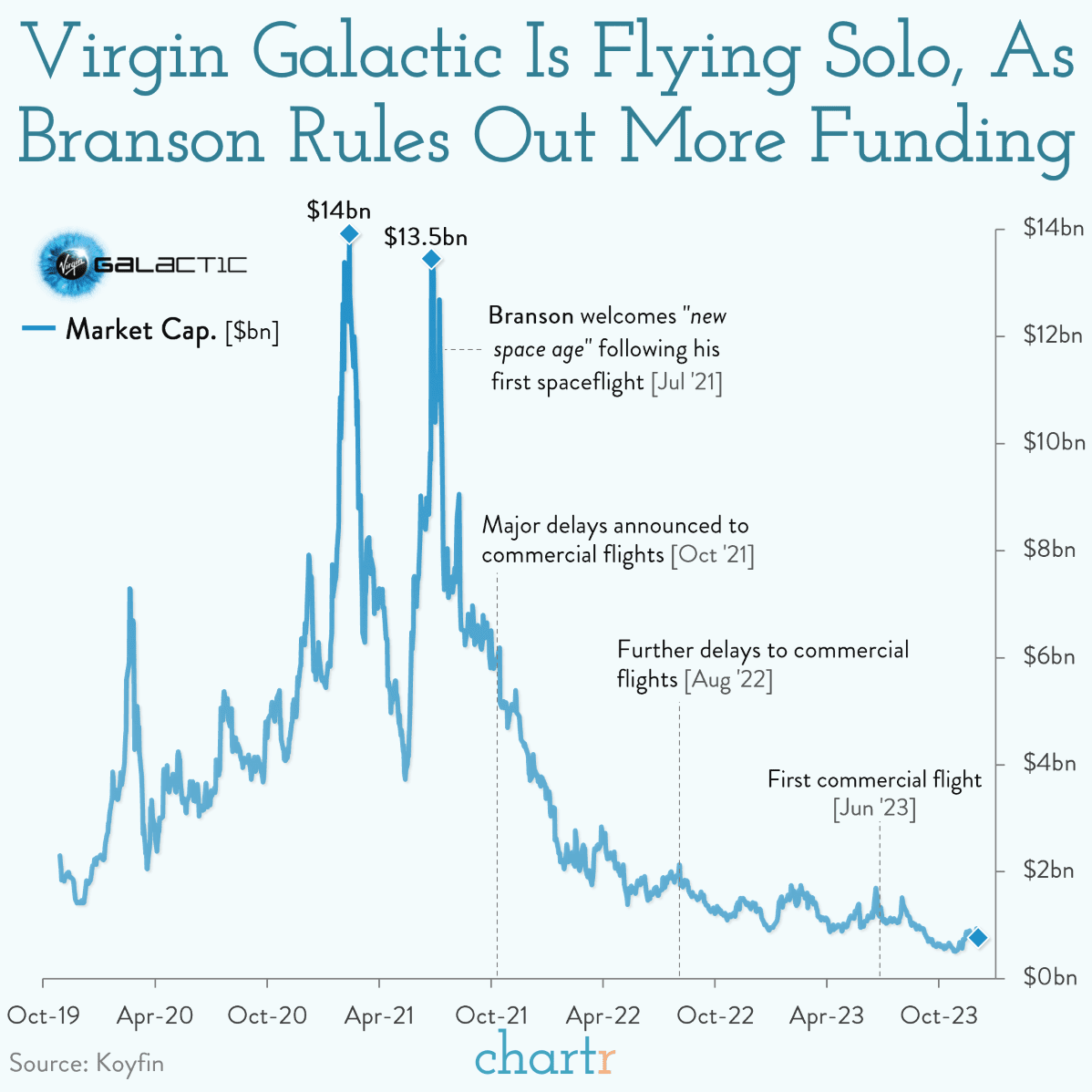

After NASA’s founding in 1958, the elusive idea of “the future” looked to many like robot cleaners, flying cars, and taking in the vistas of outer space on your commute. Just 11 years later, one giant leap towards that vision was taken — when man first visited the moon — but, for many decades after the lunar expeditions, progress in space was more small steps than giant leaps.

Recently, however, space travel has been blasting back into the headlines, as private enterprise has taken up the mantle of exploration, with trips to space, zero-gravity experiences, and even a space hotel just some of the projects underway. At the forefront of space tourism are billionaires Bezos, Musk and Branson, with ‘cosmic one-upmanship’ peaking in 2021 amidst competing launches, massive PR pushes, and celebrity-packed flight crews.

Cosmic capitalism

These endeavors promise a bright future for humans in space, with commercial and scientific interests briefly aligning, upending the government-funded model that defined the previous century. But, much like the US government discovered in the 1960s… space travel requires almost infinitely deep pockets — and some billionaires have had enough of pouring their capital into a black hole.

Feeling the weight

Indeed, only a month after laying off 18% of its workforce, Sir Richard Branson announced last week that Virgin Group will no longer be investing in Virgin Galactic. That was a big blow to the company which had finally flown its first commercial customers in June; a launch that took 3 tourists, including a mother-daughter duo, to the edge of space, where they experienced a few minutes of weightlessness.

Branson’s pullback sent Virgin Galactic shares tumbling on Monday, and although they've since recovered some of that fall, the stock remains down 44% in the last 6 months, and a whopping 96% from its peak in 2021. Even at $450k per ticket, Virgin Galactic has a very long mission to making any kind of profit.

To put it simply, Branson’s rivals in the billionaire space race — Bezos’s Blue Origin and Musk’s SpaceX — simply have a lot more cash, with Musk’s personal $200bn+ hoard often gaining or losing Branson’s entire net worth (~$3bn) in a single day, depending on what Tesla’s stock is doing.

Space tourism... and beyond

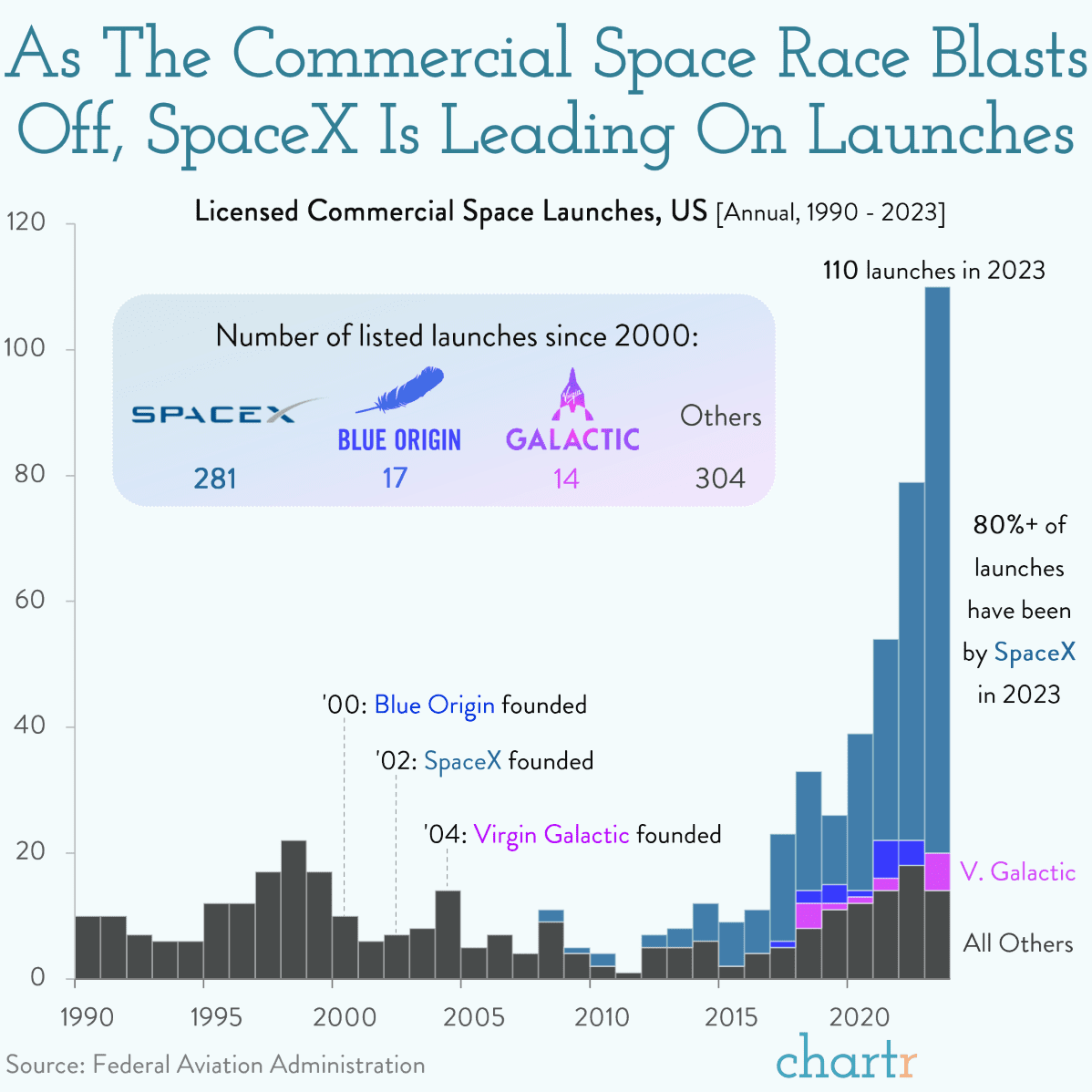

Indeed, SpaceX, which has a wide-ranging set of commercial interests beyond taking tourists to the edge of space, continues to move forward — with a tender offer reported last week that could value it at $175bn. Plans for thousands of internet satellites, commercial travel to the moon, a base on the lunar surface and even loftier goals to turn the human race into an interplanetary species by colonizing other planets, are all ambitions of the California-based company.

SpaceX has catalyzed much of the excitement about space tourism. The company’s two-stage Falcon 9 rocket is able to launch a kilogram into low-Earth orbit for just ~$1,500, a 10-20x decrease in cost in roughly as many years. That's due to its (partial) reusability — a breakthrough that’s helped SpaceX dominate commercial launchpads in the US. Indeed, FAA data reveals that SpaceX has completed 281 licensed launches since 2000 — 9x as many as Blue Origin and Virgin Galactic have managed between them.

Up

Of course, even if you re-use some of the rocket, burning hundreds of tonnes of CO2 in the pursuit of tourism for rich people is always going to be controversial. But, not all space tourism ventures see themselves blasting into the final frontier. A French startup, Zephalto, is looking to make its first ascent in late 2024, carrying 6 passengers in a pressurized cabin with comfy couches attached to a giant eco-friendly balloon, offering passengers Michelin-starred catering while they look at the Earth’s curves. Needless to say, Zephalto’s vision remains more of a concept for tourists, than a reality, for now.

These ventures all beg perhaps the most important question of all: does anyone want to go to space anyway?

. . .

The material presented on Molly O’Shea’s website are my opinions only and are provided for informational purposes and should not be construed as investment advice. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular security, strategy, or investment product. Any analysis or discussion of investments, sectors or the market generally are based on current information, including from public sources, that I consider reliable, but I do not represent that any research or the information provided is accurate or complete, and it should not be relied on as such. My views and opinions expressed in any website content are current at the time of publication and are subject to change. Past performance is not indicative of future results.

Merry Christmas Molly, thanks for all the info nuggets this year